Oil at $120 – no wait, $86 – grabbed headlines this week.

AI, mostly because it’s new, is getting blamed for a weak jobs report in February.

Both are impactful…and transient.

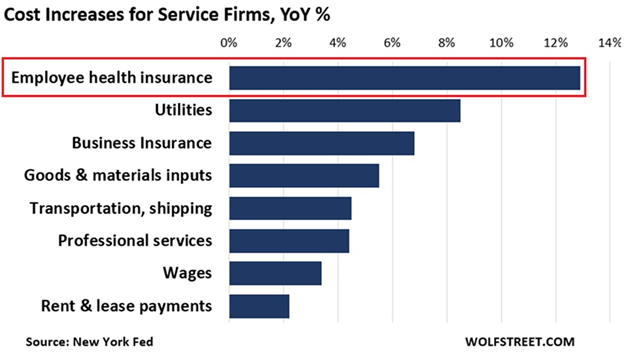

The biggest driver for both rising prices and slowing employment – and a compression in corporate profits — is health insurance:

Health care, among other corporate costs, has been soaring faster than the rate of inflation. (Source: Wolf Street)

Health care, among other corporate costs, has been soaring faster than the rate of inflation. (Source: Wolf Street)

Rising costs associated with employees, particularly health insurance, are the biggest reason the jobs numbers are weak.

Several macro trends are unfolding in the stock market at once:

- Retail investors are still buying tech and AI stocks at historic rates, while the pros sell and diversify like the late dotcom bubble in 2000-01…

- Private credit markets are seizing at a pace similar to subprime mortgages in late 2007…

- Commodities and energy prices reacting to rising demand and government money printing like the 1970s….

The late 2020s are shaping up to be in an economic era all on their own: sell stocks, buy energy.

~ Addison

P.S. With the war on and lines backing up at TSA check points across the nation, it seems like an odd week to be traveling. Then again…

It’s also a good week to visit old friends in Panama! This week, Grey Swan Live! will be recorded on scene in Panama City.

We’re traveling to join The Gathering, a group of investors in an international real estate; project led by friend and associate Ronan McMahon and his team at Real Estate Trend Alert.

Along with Alfredo Alemán we’ll be examining Panama’s 20-year outlook in a world where chokepoints and liquidity matter more than headlines. As well as some choice properties in Panama’s most cosmopolitan city.

The Ipanema and Beachwalk briefings will provide us with context on jurisdiction, infrastructure, and the long-term prospects for allocating some of our capital to vacation rentals across Latin America and in select places in Europe.

We’re looking forward to it. The Gathering was a unique experience in Playa del Carmen, Mexico last year. We expect nothing less of Panama City this year. Learn more here…