Good news broke with the rise of the sun this morning: the Strait of Hormuz is officially open again — assuming “you believe what you read in the papers.”

Which, as we were catching up with Doug Casey today, he assured us he does not.

The markets did, for a time at least. Oil traded down $10 to $84 a barrel after spending the week in the mid-90s.

Gold pushed upwards past $4,800. Mr. Casey called the gold surge “a little bit counterintuitive.” But U.S. C-130 transport planes continue moving troops and munitions into the Middle East, rather than out.

“Chances are this is just a pause in hostilities,” Casey summarized. “Everybody’s taking the opportunity to reload.”

We got a brief flash of an oil trader on a desk in lower Manhattan just after the open, watching crude drop $6 in the first hour.

Tankers that had been idling or rerouting over the past six weeks were now transiting Hormuz again, albeit under tighter coordination.

Port access for Iranian cargo remained restricted under U.S. naval enforcement. Our trader, then, reduced a short-term hedge built earlier in the week and shifted exposure back toward equities. Oil dropped a few bucks more… the S&P 500 and Nasdaq added to yesterday’s record close.

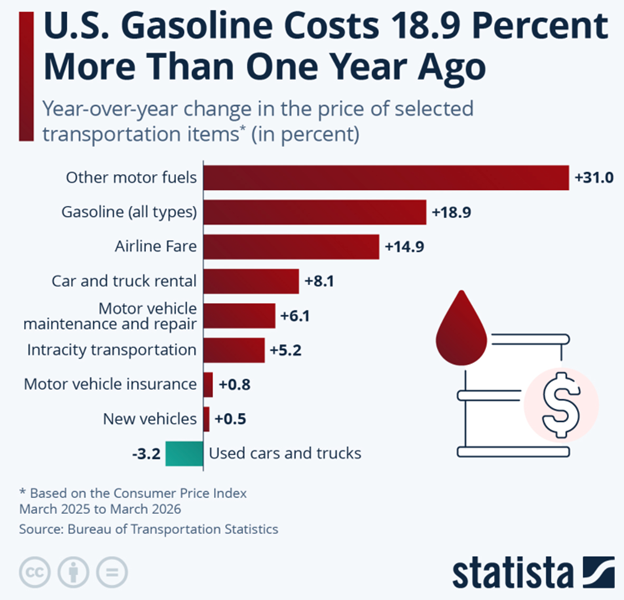

⛽ Gasoline Prices Rise in March

The Bureau of Labor Statistics reported that gasoline prices rose 18.9% from March 2025.

From February to March alone, prices increased 21.2%, the largest monthly increase on record.

The move followed the six-week disruption to Middle Eastern supply routes, when flows through Hormuz slowed and global inventories tightened.

If nothing else, the “data journalists” at Statista.com produce nice charts following headline-grabbing data sets in a timely manner. (Source: Statista.com)

If nothing else, the “data journalists” at Statista.com produce nice charts following headline-grabbing data sets in a timely manner. (Source: Statista.com)

In another scene, at a gas station off I-95, a delivery driver stood with the nozzle in hand, recalculating his route. Two extra deliveries covered the difference. Across the country, similar adjustments are taking place — longer routes consolidated, fewer idle miles, more attention paid to timing.

The University of Michigan’s Consumer Sentiment Index fell to 47.6, below levels recorded during both the Great Recession and the pandemic. Open-ended responses cited higher fuel costs and the Iran conflict directly.

At PNC, CEO Bill Demchak reviewed internal data across deposit accounts and credit usage. Gasoline remains roughly 3% of total consumer spending. Beyond that, employment levels are steady. Income flows have not broken. Households are absorbing higher fuel costs through small behavioral changes rather than broad cutbacks.

Nobody, today anyway, has been particularly bothered by the prospect that AI is going to wipe out jobs for the middle class.

🛢️ Semafor World Economy Calls It A Wrap

The final slate of speakers and panel contributors graced the stage at Semafor’s World Economy event in Washington, D.C.

David Schwimmer, a former Goldman Sachs executive who is now CEO of London Stock Exchange Group, described the current posture as “rational complacency,” noting that markets have recovered to record highs despite an ongoing conflict affecting global energy supply.

Jim Esposito, after 29 years at Goldman, now sits in the president’s chair at Citadel, and described the buy-the-dip crowd as exhibiting a blatant “breakdown in discipline.”

Amos Hochstein, Managing Partner at TWG Global, pointed to the spread between spot crude prices and futures curves, which continue to imply a shorter supply or price disruption than headline hysteria or physical oil delivery suggests.

Despite today’s price drop to $84, longer-dated crude contracts remain anchored closer to $70 than $80, indicating traders expect the price to normalize even as infrastructure and supply chains digest the new “post-ceasefire” normal.

🪖 U.S. Navy Enforces Iranian Port Blockade

Here’s the part that gives Doug Casey pause:

U.S. Central Command deployed more than 10,000 sailors, Marines, and airmen, along with over a dozen warships and dozens of aircraft, to enforce a blockade on Iranian ports this week. In other words, the U.S. Navy is still actively engaged.

Admiral Brad Cooper reported that 14 vessels turned around within the first 72 hours to comply with the blockade of Iranian ports.

On the deck of destroyers in the Gulf, crews are monitoring two flows: tankers transiting designated lanes through Hormuz and vessels approaching restricted Iranian ports. Commercial shipping continues under supervision. Iranian export capacity remains constrained at the port level.

It’s a dirty job. Someone’s gotta do it. At least until Nato boats arrive to help out.

To wit, U.S. Secretary of War Pete Hegseth said U.S. forces remain “maximally postured” to resume operations if negotiations fail.

Tick. Tock.

🏛️ The “Golden Age” Policy Trifecta

In Washington, Treasury Secretary Scott Bessent’s team continued to pressure the Senate Banking Committee to get a final draft of the Clarity Act on the Senate floor for a vote.

Federal debt financing continues to depend on stable yields and consistent auction participation.

In Bessent’s view, Dollar 2.0 digital assets will, if the Senators do their jobs correctly, provide a global 24/7 market for stablecoins backed by Treasurys, thereby making it easier to finance the U.S. National Debt ($39 trillion!).

President Trump is confident his nominee to replace Jerome Powell as Chair of the Federal Reserve, Kevin Warsh, will also be hauled into the Senate for confirmation hearings next week.

Stablecoins, Warsh’s plan for lower interest rates and cheaper energy as a result of military action in Venezuela and Iran would constitute the trifecta of policy achievements for the U.S. economy, and a win for Republicans in the House of Representatives during November’s midterm elections, if they can pull it off.

During this afternoon’s trading, Treasury yields held within a narrow range. Equities moved higher alongside falling crude prices. Traders tied both moves to the same development—resumption of shipping through Hormuz combined with continued restrictions on Iranian exports.

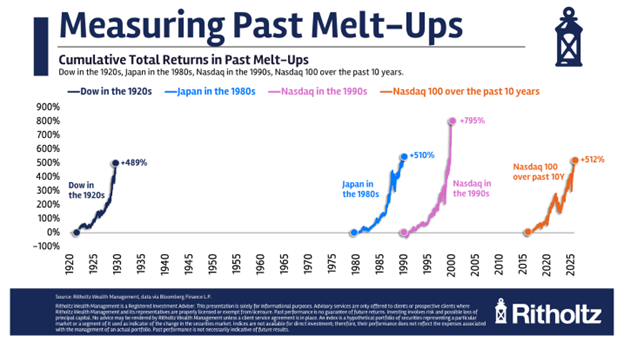

📊The Post-War 1950s Bull Market Ran Against Sentiment

Ben Carlson, a research analyst with Ritholtz Wealth Management, caught our eye with an analysis of the bull market in U.S. stocks that followed the end of World War II.

It’s the “Greatest Bull Market that No One Talks About,” according to Carlson, because even in the midst of it, the hangover from 1929’s epic collapse remained seared in investors’ minds.

In 1953, Robert Bleiberg wrote in Barron’s that brokerage firms struggled even as stock prices rose because trading volume remained low.

The S&P 500 returned approximately 19.5% annually across the decade, while popular participation from everyday investors lagged the advance.

Carlson compiled the annual returns on the U.S. market from the 1950s:

- 1950 +30.8%

- 1951 +23.7%

- 1952 +18.2%

- 1953 -1.2%

- 1954 +52.6%

- 1955 +32.6%

- 1956 +7.4%

- 1957 -10.5%

- 1958 +43.7%

- 1959 +12.1%

Seven of the 10 years produced double-digit gains. Half exceeded 20%. Over the past 2 years, gains have been above 40%. The largest annual decline was approximately 10%. And yet no one remembers…

📈 Melt-Up Conditions Mirror Prior Cycles

Carlson compared those figures to the current market.

The Nasdaq 100 has returned roughly 20% annually over the past decade and approximately 22% annually from the March 2009 lows.

Those returns align with prior cycles such as the Roaring 20s and Japan in the 1980s, both of which ended with sharp reversals.

Following the dot-com peak, the Nasdaq declined more than 50% between 2000 and 2008. From 2000 through 2013, total returns averaged 1% per year.

Today, the ten largest companies account for more than 50% of the index. Earnings growth supports the indexes. Concentration at the top of the indexes drives headlines about the booming market amid the Iran conflict.

Carlson’s conclusion is straightforward: sustained returns at this pace do not continue indefinitely. Lower forward returns are more likely than uninterrupted growth. Diversification becomes relevant when concentration dominates performance.

For more research on the Shadow Stocks that we expect to perform well during this extraordinary market that no one is talking about, either, see: Shadow Stocks: Hidden Gems In Today’s Volatile Markets, here.

📜 The War For Iran’s Resources Has Gads of Precedent

“Iran cannot have a nuclear weapon,” President Trump has repeated ad nauseam since February 28. 2026. While we measure the success of the war in terms of the oil price, there is a long precedent of using nukes as the motive for military action; ever since the U.S. used them first in Hiroshima and Nagasaki, Japan, in 1945.

On this day, April 17, in 1945, the History Channel tells us, U.S. Lieutenant Colonel Boris T. Pash commandeered over half a ton of uranium at Strassfurt, Germany, in an effort to prevent the Soviets from developing an A-bomb.

Pash was head of the Alsos Group, organized to search for German scientists in the postwar environment in order to prevent the Soviets, previously Allies but now a potential threat, from capturing any scientists and putting them to work at their own atomic research plants.

Uranium piles were also rich “catches,” as they were necessary to the development of atomic weapons for use by the U.S. military.

~Addison

P.S. Yesterday on Grey Swan Live!, we showcased our latest research on Shadow Stocks – volatile stocks that move rapidly up and down beneath the surface of the calm indexes.

Earnings season is a ripe time for cherry-picking stocks. Along with the research, we are launching an upgrade to your Grey Swan forecast emails that will include up to five stock or trade recommendations a week.

To kick it off, we’re going to give you three stocks free of charge. Gratis. On the house. The research is excellent, and the upgraded Grey Swan Pro will be worth your time to consider. Take a look here.