Yesterday, we explored how the Great Race is unfolding in foreign capitals and bond markets overseas… and increasingly inside the American system itself.

Twenty states have already enacted Article V of the Constitution to push restraints on deficits and debt, spending and term limits at the Federal level. The advocates only need to sign up 14 more states to try to save the Republic from itself.

Gold, too, is quietly re-emerging as the oldest form of money. Eleven states have taken their cues from the Constitution and enacted positive state-level laws making gold and silver transactional money.

Beneath all three stories sits the same larger reality: the 40-year age of cheap money and frictionless globalization is giving way to a more competitive world organized around monetary credibility, industrial capacity and control over strategic resources.

The investors positioning themselves ahead of that transition increasingly resemble old-world industrialists more than modern financial engineers, which may explain why Buffett, Dalio and Druckenmiller continue migrating toward energy, commodities and the physical economy.

Today, we arrive at a possibility so politically radioactive that most respectable economists would rather swallow a stapler than discuss it publicly.

What if President Donald Trump ultimately attempts a sovereign restructuring of the American balance sheet?

🏛️Let’s call it Chapter 47

Not because the United States would literally declare bankruptcy under Chapter 11 or 13. Sovereign governments operate under entirely different legal rules. But because Trump’s entire career suggests he thinks about debt differently than almost any modern politician who has occupied the Oval Office.

Trump’s political opponents like to goad him for “going bankrupt” six times in his career.

They’re, of course, missing the point.

Much like Buffet says about paying his personal taxes: “If you don’t want me to use the bankruptcy laws to my advantage,” Trump might say, “change the law.”

Every president in the post-World War II Pax Americana era has treated debt as an accounting problem. “Reagan proved,” according to then Congressman Dick Cheney, “that deficits don’t matter.”

Cheney meant voters would not punish elected officials for running deficits or mounting debts on the liability side of the Federal government’s books.

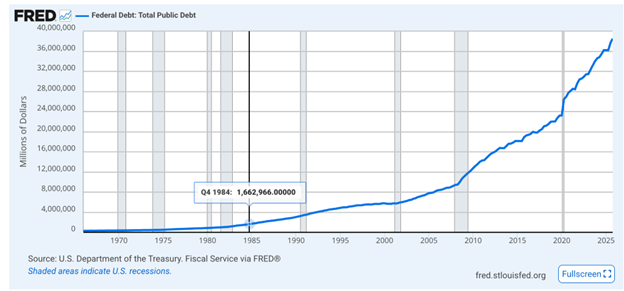

Reagan proved that voters would not punish elected officials for running deficits, so long as their mission was, in their view, worthy enough. Reagan ran aggressive deficits to “outspend the Soviet Union into oblivion” during the Cold War. Once that die was cast, no successor president has paid much attention. (Source: Federal Reserve)

The 47th President of the United States treats debt as leverage. That distinction may become enormously important during the next phase of The Great Race.

🎰 The Casino Lessons of Atlantic City

For years, Trump’s corporate bankruptcies became shorthand for ridicule among financial commentators who preferred reducing complex restructurings into late-night punchlines.

But anyone who survived the New York real-estate world of the 1980s understood something different.

Debt restructurings are negotiations.

Trump’s Atlantic City casino empire borrowed aggressively during the debt mania of the late 1980s, particularly around the Taj Mahal project, which opened carrying financing burdens heavy enough to sink a battleship.

When revenues collapsed beneath the interest costs, Trump used Chapter 11 proceedings not as a surrender, but as a mechanism to force creditors back to the table.

The banks faced an ugly reality.

Liquidating the properties would destroy enormous amounts of value while publicly humiliating lenders already overexposed to the collapsing commercial real estate market. Keeping Trump alive politically and financially offered better odds of recovering capital over time than detonating the enterprise outright.

So the lenders blinked, balked… cajoled.

Debt maturities stretched outward. Bondholders absorbed losses. Ownership stakes changed hands. Creditors accepted concessions because preserving the broader system mattered more than enforcing punishment in the present moment.

Here’s an amusing list of Trump’s effort to put his name on everything:

- Trump University: A for-profit real estate education company launched in 2005 that shut down following numerous fraud lawsuits and a $25 million settlement.

- Trump Airlines: Launched in 1989 after purchasing Eastern Air Shuttle, it defaulted on loans and was surrendered to creditors by 1992.

- Trump Steaks: Introduced in 2007, this premium meat brand was discontinued shortly after launch due to extremely low sales.

- Trump Vodka: A premium spirits brand launched in 2006 that failed to capture significant market share and ceased sales by 2011.

- Trump Mortgage: A mortgage brokerage firm founded in 2006 that closed within a year due to the declining housing market and poor management.

- GoTrump.com: An online travel booking site launched in 2006 that failed to gain traction and shut down within a year

Trump learned something from those experiences that most politicians never fully internalize:

If the debtor is large enough, interconnected enough and strategically important enough, the negotiation changes completely.

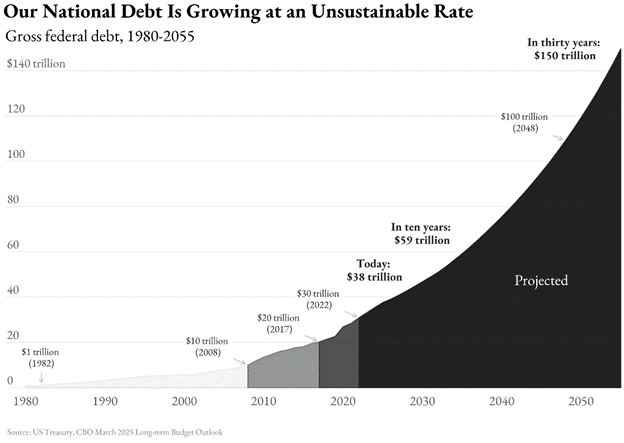

Now place that mentality in the Oval Office as the United States carries debt levels accumulated over 40 years of globalization, financialization and permanently falling interest rates.

What was once a long-term concern is now showing up in real time. The national debt is increasingly shaping the economic backdrop, with higher interest costs crowding out growth and tightening financial conditions. (Source: US Treasury)

With the 47th president, the national debt conversation becomes much more interesting.

📈 The Bond Market Begins Asking Dangerous Questions

For decades, the machinery of Pax Americana functioned beautifully because the world trusted three assumptions simultaneously:

America would remain dominant, globalization would keep inflation contained, and Treasury bonds would remain the safest asset on earth.

That arrangement allowed Washington to borrow extraordinary sums at relatively low interest rates while foreign governments recycled trade surpluses back into U.S. debt markets almost automatically.

The system reinforced itself. As long as rates were low enough, traders high and low were happy to consider “treasury debt” as risk-free.

Cheap imported goods suppressed inflation. Lower inflation supported lower interest rates. Lower rates inflated financial assets and encouraged even more borrowing.

Then came the pandemic, supply-chain fragmentation, energy shocks, and the AI infrastructure race now unfolding between the United States and China.

Since May 13, 2026 – for the past three weeks – the 30-year Treasury Yield has stubbornly remained above 5%.

The trend higher began in September 2024.

After six Federal Reserve rate cuts between then and December 2025, lenders increasingly appear worried that the next industrial era will require enormous spending on electrical grids, semiconductor fabrication plants, military systems, energy infrastructure and domestic manufacturing, all at once.

Artificial intelligence may eventually produce extraordinary wealth. But building the physical infrastructure supporting that future requires staggering amounts of capital today.

And the bond market increasingly seems unsure whether the old debt structure can comfortably survive the transition.

That is where Chapter 47 enters the conversation.

⚙️ What Chapter 47 Might Actually Look Like

Now, let’s be honest.

The United States cannot simply “walk away” from its Treasury obligations without triggering a global financial meltdown.

But sovereign restructurings rarely happen through dramatic formal default anyway.

They occur through monetary policy adjustments, asset repricing, inflation management, maturity extensions and changes to the rules governing the debt itself.

One path might involve some form of national asset restructuring, in which federal lands, energy reserves, mineral rights and infrastructure projects are partially tied to Treasury financing vehicles.

Foreign creditors and sovereign wealth funds are increasingly nervous that fiat debt alone could, in theory, expose them to productive American assets directly connected to energy production, rare-earth development, or industrial infrastructure.

Another possibility involves aggressive Federal Reserve intervention through yield-curve control and the monetization of long-term debt. That was the effort the post-2008 financial crisis Bernanke Fed championed. Followed by the “DEI and climate emergencies” declared by the Yellen Fed.

Then… the “too late” Powell pandemic era and historic inflationary Fed.

Under the new Chair, Kevin Warsh, the Fed could effectively cap borrowing costs by purchasing enormous amounts of Treasury debt whenever markets push yields above politically tolerable levels.

Trump has stressed independence for Warsh, positioning him as a technocratic operator rather than a political extension of the White House, even as the appointment reflects a broader effort to reshape monetary policy direction. (Source: Getty Images)

Of course, that risks weakening confidence in the dollar itself, which explains why the Trump Administration increasingly appears interested in building what Scott Bessent has informally described as a next-generation dollar architecture — what we have been calling Dollar 2.0 — around stablecoins, digital settlement systems and Treasury-backed liquidity mechanisms capable of creating fresh global demand for dollar assets.

And then there is the oldest restructuring mechanism in history:

Inflate the debt away slowly while rebuilding the productive economy faster than the liabilities compound.

That strategy only works if the industrial boom actually arrives. And if voters don’t throw a hissy fit at the gas station or in the grocery aisle.

This may explain why the administration behaves as though AI, energy dominance and industrial reshoring represent existential national priorities rather than ordinary economic policy.

Whatever path Trump decides, it will have to be a remarkable shift away from the existing path if he expects sovereign wealth funds, bond vigilantes of Wall Street’s biggest banks, to know that the regime change is for real.

And it’s going to have to happen before the midterms on November 3.

🌎 Why Trump Might Believe Chapter 47 Could Work

Trump would never call it a default.

He would call it a reset.

That distinction matters because Chapter 47 would not look like America collapsing beneath unpaid bills. It would look like America reorganizing the financial system around a new industrial era, the same way distressed companies reorganize around a new business model after the old one stops working.

Trump understands something most politicians avoid admitting publicly:

When debt grows too large, the question eventually stops being:

“How do we pay it back?”

And becomes:

“How do we keep the system functioning while we build the next source of growth?”

That is pure restructuring logic.

In Trump’s world, bankruptcy was never primarily about liquidation. It was about freezing pressure long enough to preserve strategic assets and reposition the enterprise for survival.

Translated into sovereign terms, Chapter 47 could begin with a declaration that America is entering a national industrial mobilization period tied directly to:

- AI,

- energy dominance,

- semiconductor independence,

- military modernization

- and domestic manufacturing capacity.

The administration could argue that the old Pax Americana system — built on globalization, cheap imports and endlessly expanding debt — no longer fits the realities of the 21stcentury.

So instead of “inflate or die,” the message becomes something much more ambitious:

America is restructuring itself around the industries that will dominate the next hundred years.

That is a very different psychological framing.

Under Chapter 47, the government would likely attempt to:

- stabilize Treasury markets through Dollar 2.0 systems,

- redirect capital toward industrial expansion,

- anchor portions of the financial system to hard assets and productive capacity,

- and gradually dilute legacy debt through growth, controlled inflation and industrial output.

The public argument would not be:

“We cannot afford our debts.”

It would be:

“The old system financed consumption. The new system must finance production.”

That is a far more politically survivable narrative because Americans historically tolerate enormous restructuring during periods framed as national rebuilding:

- The New Deal,

- World War II Mobilization,

- The Interstate Highway era,

- The (old) Space Race,

- The Cold War

Trump’s probably the only president who could present Chapter 47 at all. And in the same way, he presents most negotiations not as retreats but as leverage.

Not:

“America is weak.”

But:

“America is reorganizing to win The Great Race.”

And honestly, that may be the only version of debt restructuring global investors – or the American public – would ever accept.

This is the critical point most commentators miss. Trump does not view artificial intelligence merely as a technology boom.

Increasingly, 47 appears to view it the way Franklin Roosevelt viewed wartime industrial mobilization or the way postwar planners viewed the interstate highway system: as the organizing economic engine of an entirely new era.

That helps explain the strange mosaic of policies now unfolding simultaneously across the administration:

Saudi energy super deals, Greenland mineral negotiations, semiconductor restrictions, uranium interest, stablecoin legislation, electrical-grid expansion and aggressive efforts to secure domestic manufacturing capacity.

Viewed separately, the details feel disconnected. Viewed together, they resemble preparations for a massive industrial reset.

Jensen Huang, CEO of Nvidia, recently described the AI economy as a “five-layer cake,” beginning with energy generation, chips and data centers, long before consumers ever touch the software itself. Most investors still focus on the frosting while the administration increasingly behaves as though it intends to dominate the layers underneath.

🧠 How Everyday Investors Could Benefit

Now here is the less wonky part you may actually care about. What happens to individual investors if some version of Chapter 47 succeeds?

The answer depends entirely on where their money sits during the transition.

The last 40years rewarded financial assets tied to globalization, falling rates and cheap borrowing. That environment favored long-duration growth stocks, passive indexing, financial engineering and debt-fueled asset inflation.

Chapter 47 would likely reward something very different.

If the United States successfully restructures its debt burden while rebuilding industrial capacity around AI infrastructure and energy dominance, businesses tied to the physical economy could enter a long-term secular bull market.

Electrical infrastructure, uranium, natural gas, pipelines, industrial metals, engineering firms, defense systems, semiconductor manufacturing and strategic commodities could become the backbone industries of the next American expansion.

The winners may resemble the investors who positioned themselves ahead of the post-war manufacturing boom in the late 1940s rather than the software investors who dominated the age of globalization.

That may be why Warren Buffett continues to concentrate enormous amounts of capital in energy and industrial systems, while Ray Dalio openly warns about debt cycles and monetary disorder. Stanley Druckenmiller keeps talking about commodity scarcity, energy underinvestment and industrial rebuilding because all three men appear to recognize the same underlying reality:

The physical economy is becoming strategically important again. And whenever the physical economy reasserts itself after long financial bubbles, fortunes tend to migrate alongside it.

There is a pivotal moment arriving in the history of the Republic, too; an extraordinary opportunity to get out from under the mountain of debt that only grows and Washington’s business-as-usual grift machine merely ignores.

Chapter 47, bring it! Make it bold.

~ Addison

P.S. History rarely announces regime change politely. Usually, the transition begins when the old financial system becomes too expensive to maintain, while the new industrial system still requires enormous investment to build.

The setup in the stock market gives us an opportunity to stress the distinction between “investing” and “trading.” The Grey Swan Model Portfolio is primarily composed of stocks that are enjoying bull-market gains and paying high dividends, a perfect mix for long-term investors.

Over at the Grey Swan Trading Fraternity, our own Andrew Packer just issued an alert to close a trade in a space-related stock that’s been soaring in recent weeks. Total gains as of Friday’s close were over 130% – with a final return of over 200% following this morning’s market surge.

The SpaceX IPO, valued at nearly $2 trillion, will be a lot for the market to digest – and could lead to a vacuum sucking up capital from other stocks. This may be yet another case of the old adage of buying the rumor – in this case, all the details of the SpaceX IPO – and selling the news when it does happen.

As always, if you have any questions for us, send them to Feedback@GreySwanFraternity.com.