A funny thing happens when an empire grows old.

The financial system that once seemed permanent is slowly behaving like an aging casino somewhere off the Atlantic City boardwalk. The chandeliers still sparkle. The carpets still look expensive from a distance. Cocktail waitresses still weave through the blackjack tables, balancing watered-down martinis beneath soft lighting.

But somewhere behind the walls, the plumbing groans, the wiring overheats and accountants begin holding conversations in quieter voices.

That mood increasingly hangs over the American debt market now.

For decades, investors treated U.S. Treasury bonds as the safest financial asset on earth because the assumptions supporting Pax Americana felt almost eternal. Globalization suppressed inflation. Foreign governments recycled trade surpluses back into Treasury markets.

The Federal Reserve pushed borrowing costs lower whenever markets stumbled badly enough. Washington borrowed, Wall Street speculated and consumers kept spending because everyone assumed the machinery underneath the system would continue functioning indefinitely.

Now the machinery itself is beginning to strain.

Long-term Treasury yields continue hovering near levels that would have seemed unthinkable during the easy-money years, even after the Federal Reserve cut short-term rates six times between September 2024 and December 2025.

Under the old rules, that should have eased pressure across the entire financial system. Instead, the bond market continues acting like an exhausted banker staring across the table at a debtor who suddenly wants another enormous line of credit while already carrying multiple maxed-out cards in his wallet.

David Kelly, Chief Global Strategist at JPMorgan Asset Management, warned this week that even the best-case scenario for America’s debt burden still likely involves economic deterioration, inflation pressure and recession risks unless artificial intelligence delivers productivity gains large enough to offset the strain.

Fortune columnist Nick Lichtenberg noted that Kelly also warned that a Federal Reserve perceived as subordinate to White House borrowing needs could shatter investor confidence in Treasury markets altogether, as markets would begin viewing the central bank less as an inflation fighter and more as a financing arm for government debt.

That is not an ordinary warning coming from one of Wall Street’s more sober strategists.

But it does help explain why the Trump Administration increasingly appears less interested in preserving the old financial order than redesigning it for the next industrial era.

🏛️ The Art of the Sovereign Restructuring

That brings us to what we have been calling Chapter 47, the 47th President’s options when it comes to restructuring the $39 trillion in national debt. At 122.5% of the United States’ total gross domestic product (GDP), the territory is already in what most traditional economists would call the “danger zone.”

If Congress is, as they have consistently proven to be, incapable of reining in spending by any small measure, then the executive branch will be forced to deal with a severe and debilitating sovereign debt crisis… at the epicenter of the Western financial system.

A sovereign bankruptcy is not anything like what happens to individuals or failing corporations.

The United States cannot simply march into federal court and walk away from its obligations, as an overleveraged casino company does under Chapter 11 protection. Sovereign governments operate differently.

The 47th president of the United States spent decades in the private sector learning how debt restructurings work in practice, and the lesson he appears to have internalized is that sufficiently large systems rarely collapse cleanly. They reorganize themselves around whatever new source of growth promises survival on the other side.

That mindset suddenly matters enormously because the administration increasingly behaves as though artificial intelligence, energy infrastructure and industrial reshoring represent the economic equivalent of wartime mobilization.

Viewed through that lens, Chapter 47 begins to look less like financial desperation and more like a national industrial reset wrapped in emergency executive authority.

The legal architecture already exists.

The International Emergency Economic Powers Act gives the president broad authority during declared national emergencies tied to economic threats, foreign instability or national-security risks. Those powers already support sanctions regimes, banking restrictions, trade controls and asset freezes across a large portion of the global economy.

Under the framework emerging around The Great Race, the administration could plausibly argue that AI competition with China, semiconductor dependence, cyberwarfare vulnerabilities and Treasury-market instability collectively constitute a national-security emergency requiring coordinated industrial and financial action.

That declaration alone would unlock extraordinary flexibility.

Then there is the Treasury’s Exchange Stabilization Fund, one of the least understood but most powerful pools of financial authority inside Washington. Created in 1934 during the aftermath of Franklin Roosevelt’s gold-confiscation era, the ESF gives Treasury wide latitude to intervene in currency markets, sovereign-debt operations and financial stabilization programs with relatively limited congressional oversight.

During Chapter 47, mechanisms like the ESF could support Treasury markets, stabilize digital-dollar systems and help anchor the broader transition toward what Treasury Secretary Scott Bessent increasingly appears to envision as Dollar 2.0.

One of Kevin Warsh’s stated goals as incoming Federal Reserve Chairman is to restore credibility to the central bank and to unload assets that have been accumulating since the 2008 financial crisis. Warsh believes the bank has lost its way and is spending too much of its time and energy manipulating markets, the economy and the culture. He will likely butt heads with governors on the board who argue the Fed needs to maintain its activist policies. (Source: BNP Paribas, Fortune 500)

One of Kevin Warsh’s stated goals as incoming Federal Reserve Chairman is to restore credibility to the central bank and to unload assets that have been accumulating since the 2008 financial crisis. Warsh believes the bank has lost its way and is spending too much of its time and energy manipulating markets, the economy and the culture. He will likely butt heads with governors on the board who argue the Fed needs to maintain its activist policies. (Source: BNP Paribas, Fortune 500)

The Federal Reserve’s emergency lending powers under Section 13(3) create an entirely separate layer. Those authorities returned during the 2008 financial crisis and again during the pandemic, when the Fed quietly became the refinancing arm for large parts of the economy.

If Chapter 47 ever moved from theory toward reality, the Fed would almost certainly become deeply involved in supporting Treasury liquidity, industrial financing and credit markets tied directly to the AI buildout now underway.

🧠 Mythos and the New National Security State

What makes this moment different from previous financial crises is that Washington no longer sees artificial intelligence merely as a technology sector.

The administration increasingly appears to view AI as strategic infrastructure on the scale of railroads, nuclear systems or the interstate highway network.

That realization may explain the increasingly tense relationship between the White House and Anthropic over control of its restricted Mythos model.

According to reporting from the New York Times, Wall Street Journal and multiple cybersecurity publications this month, Mythos demonstrated unusually sophisticated capabilities involving network vulnerabilities and cyber exploitation, triggering alarm across intelligence and national-security circles.

Regulators spent years threatening to rein in AI. Now they’re terrified of missing the boom entirely. After years of focusing on AI risks, policymakers are now racing to ensure the U.S. doesn’t fall behind in the global AI arms race. (Source: Wall Street Journal)

White House officials reportedly opposed broader commercial access to the model while simultaneously debating how tightly frontier AI systems should remain tied to government oversight.

The details matter less than the pattern.

Washington increasingly appears to view frontier AI systems the way earlier generations viewed cryptography, satellite technology or nuclear research during the Cold War. Once a technology becomes deeply connected to cyberwarfare, financial infrastructure, intelligence gathering and sovereign competitiveness, the relationship between government and private industry changes rapidly.

The arrangement emerging now resembles a hybrid system in which strategically important firms receive regulatory protection, infrastructure support, guaranteed energy access and enormous federal contracts, while the government gradually gains operational influence over technologies considered too important to remain entirely independent during a period of geopolitical competition.

Ten years ago, that kind of arrangement might have sounded implausible inside the American system. Today, it increasingly resembles the opening framework of industrial policy for the AI age.

And once investors begin looking at the world through that lens, many of the administration’s seemingly disconnected moves start fitting together more naturally.

Saudi energy negotiations, semiconductor restrictions, uranium supply chains, stablecoin legislation, electrical-grid expansion and Treasury-market stabilization all begin to resemble other sections of the same larger industrial strategy.

Artificial intelligence no longer behaves like a software boom floating harmlessly above the economy. It increasingly resembles a giant industrial organism that requires electricity, chips, cooling systems, energy security, sovereign financing and geopolitical coordination, all functioning simultaneously.

⚡ Wall Street Winces Under the Pressure

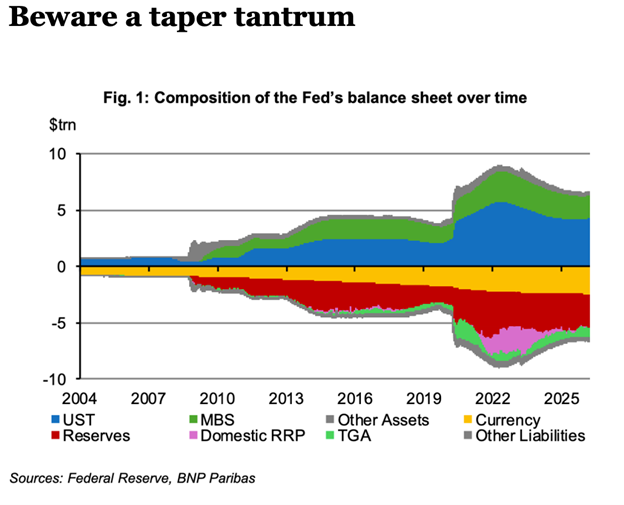

Yesterday, BNP Paribas analysts studying Kevin Warsh’s signals on shrinking the Federal Reserve’s balance sheet later this decade warned that even gradual tightening could trigger another version of the 2013 taper tantrum if markets perceive the communication as overly aggressive.

Their analysts pointed specifically to the way credit spreads widened sharply after Ben Bernanke’s 2013 comments around reducing bond purchases, reminding investors how sensitive markets remain to any suggestion that the age of endless monetary support may finally be ending.

That anxiety increasingly hangs over the entire Treasury market because lenders now understand something policymakers spent years pretending could be postponed indefinitely.

The AI era requires enormous investment in electrical grids, semiconductor fabrication, industrial infrastructure, energy production and military modernization, precisely at a moment when the United States already carries debt burdens accumulated over 40 years of globalization and artificially cheap borrowing.

That is why the bond market feels so uneasy… why the Trump administration, currently running the third-highest annual deficit in history, needs to get spending under control… and why individual investors like you need to prepare for an era of structural inflation, rather than the disinflation of the past 40 years.

It’s also why sophisticated investors increasingly migrate toward the physical economy itself.

Warren Buffett continues to concentrate enormous capital in energy and industrial systems while sitting atop record cash reserves. Ray Dalio warns openly about debt cycles, geopolitical fragmentation and currency instability while maintaining significant exposure to commodities and gold. Stanley Druckenmiller keeps discussing energy shortages, industrial rebuilding and commodity underinvestment as though the world is preparing for something much larger than another ordinary business cycle.

All three men appear to recognize the same underlying transition.

The world built during the long decades of globalization rewarded financial engineering, falling interest rates and software scalability. The next era may reward whoever controls energy systems, industrial infrastructure, strategic resources and the financing mechanisms that support them.

That is the wager sitting underneath our proposition “Chapter 47.”

The administration appears to believe America can survive a difficult debt transition if it simultaneously dominates the next industrial age.

💵 Trump’s Funny Money

And perhaps the strangest part of the entire story is how perfectly Trump himself fits the symbolism of the moment.

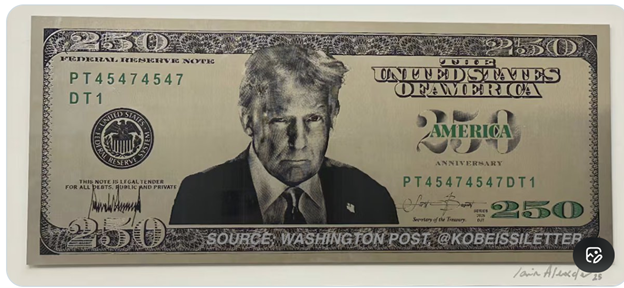

The Washington Post reported this week that the Trump administration and Treasury Department are designing a new $250 bill featuring President Trump himself. If launched, Trump would become the first living person to appear on U.S. currency since 1866.

Yesterday, we listed six failed efforts Trump has made in the private economy to slap his name on things, from whiskey and vodka to a national football league, beauty pageant and a “university”. Perhaps, 47 will be more successful with this commemorative slip of paper printed by the U.S. Treasury. (Source: Washington Post, Kobeissi Letter)

Yesterday, we listed six failed efforts Trump has made in the private economy to slap his name on things, from whiskey and vodka to a national football league, beauty pageant and a “university”. Perhaps, 47 will be more successful with this commemorative slip of paper printed by the U.S. Treasury. (Source: Washington Post, Kobeissi Letter)

Honestly, nobody should be surprised.

Trump spent his entire career placing his name on skyscrapers, casinos, airplanes and golf courses. The idea that he might eventually want his signature attached to America’s next monetary system feels oddly consistent with the larger transition now unfolding around us.

Empires eventually redesign their money, just as aging casinos eventually renovate their gaming floors. The old structure becomes too expensive to maintain as the owners desperately search for the next attraction capable of keeping the crowds inside the building.

The question now is whether Chapter 47 becomes the beginning of an American industrial renaissance or merely the latest attempt to refinance an empire already living beyond its means.

~ Addison

P.S. Somewhere inside the Treasury Department tonight, there is probably a designer adjusting the placement of President Trump’s portrait on a prototype $250 bill while bond traders in Tokyo stare nervously at 30-year Treasury yields and wonder whether America is preparing for the next great industrial boom — or simply putting a more recognizable face on the funny money.

Meanwhile, this morning’s data shows persistent inflation may become a feature of the economy in the years ahead as we move from an era of structural disinflation to structural inflation.

The most notable signal is rising long-term rates in the face of Fed efforts to cut the short-term. The signal we propose will trigger a rotation of up to $17 trillion into an unloved and overlooked segment of the S&P 500.

Investors need to prepare.

Grey Swan Live! returns this afternoon with a closer look at our latest research: The Great Race.

A global scramble is now underway for:

- Energy.

- Semiconductors.

- Industrial capacity.

- Strategic minerals.

- AI dominance.

- And monetary control.

Most people still see tariffs, gold, stablecoins, Saudi Arabia, AI, and the bond market as separate stories.

They aren’t.

They are all symptoms of the same transition: The world moving from an era of structural disinflation … to structural inflation.

And that changes everything about investing.

The physical economy is reasserting itself after decades where finance and software dominated nearly everything.

That may become the defining investment shift of the next decade.

👉 Join us Thursday at 2 p.m. ET for Grey Swan Live!

Because the race is already underway.

Most investors just haven’t realized it yet.