“If a global recession occurs because of the Iran conflict,” writes reader and frequent correspondent, Steven K., “then all bets are off.”

With his email, Steven kicks off a boatload of concern for individual investors regarding the Project 2026 midterm game plan underway by the Trump administration.

A telling sign our reader suggests we look for: Trump will likely cancel or postpone his May 14-15 trip to China because he has failed to get control of Iranian oil.

From his earlier reader mails, we’d say Mr. K is not particularly prone to Trump Derangement Syndrome (TDS), the go-to accusation often leveled at the President’s critics, most notably by White House Press Secretary Karoline Leavitt.

Steven, in fact, makes a few worthy observations:

Reducing taxes will be beneficial, but what if the problem is real wages? If Republican campaigns are preparing a confrontational approach, they’ll need to answer questions about why spend a trillion dollars on a war – right now.

They’ll also need to answer the benefits versus the risks of AI to [formerly supportive] voters. How will we recover if AI is a flop? Most vehicles purchased since COVID are worth less than their loan amounts. The FED simply lowering interest rates (free money) won’t fix our underlying economic problems. It should be interesting;

Like many, Steven is the leader of a household working through fuel bills, loan balances and wages that aren’t keeping up.

The election is set for November 3, 2026.

We summarized the historical challenge Project 2026 is meant to address yesterday:

Since 1946, the president’s party has lost House seats in 18 of the last 20 midterms, averaging 28 seats. Approval ratings below 50% have tended to coincide with larger losses. The historical record is fixed, while household balance sheets – fuel prices, borrowing costs, and wages – are a daily concern. Most popular economic surveys show that potential voters don’t see the economy improving anytime soon. (See: K-Shaped Conundrum)

That said, Project 2026 is more than winning the midterms; for Donald Trump, who we’ve frequently characterized as “the hero” in his own story, it’s about giving the U.S. economy the resources, interest rates, trade advantages and military victories it needs to compete with China in the rapidly developing AI economy.

His supporters scoff when those goals are questioned. Yet, questioned they are, frequently.

🧭 Roach’s Critique of the Trump Midterm Strategy

Stephen Roach, on Morgan Stanley’s Asia desk for some 30 years and now senior fellow at Yale University’s Jackson Institute for Global Affairs, probably does suffer from a fairly strong case of TDS.

But he’s at least more articulate about it than Hakeem Jeffries or Chuck Schumer. But then, Roach already has his bona fides and doesn’t have to win any voters from the confused ranks of the Democratic Party.

Roach offered this critique of the 2nd Trump Administration this morning:

Amid a series of massive, illegal policy blunders, US President Donald Trump has set his sights on a triumphant mid-May summit with Chinese President Xi Jinping. But it will probably go poorly because Trump is incapable of understanding Chinese strategy, a trait that goes back to Sun Tzu in the 6th century (BC).

Rumor has it that, last year, US President Donald Trump delayed his so-called Liberation Day tariff announcement by a day, to April 2, because he didn’t want his unconstitutional trade ‘emergency’ to come across as an April Fools’ Day hoax. This year, Trump defied the calendar with an address to the nation on April 1 touting yet another unconstitutional act—a war with Iran conducted without congressional approval.

Both moves have much in common. Not only do they flout the law, but they also attempt to drive a stake into the heart of the world order. Last year’s tariff shock was aimed at the rules-based global trading system established by the United States. This year’s military shock is aimed at the Middle East, long the world’s most volatile region.

Trump committed these reckless acts without any regard for their likely consequences. No surprise, both have backfired. Despite sky-high ‘reciprocal’ tariffs against America’s purportedly abusive trading partners, the US trade deficit hit a new record in 2025. And despite all the bluster about obliterating Iran’s military power, Iranian missiles and drones continue to wreak havoc in the Middle East, while the country’s strategic chokehold on the Strait of Hormuz has led to the world’s largest-ever oil shock.

Ahead of the still planned Presidential trip to Beijing, the Sinophile Roach added:

Trump, as always, will spin a tale of lies and distortion, underscoring the contrast between The Art of the Deal and The Art of War. Sun Tzu’s perspective would insist that, ‘The one with many strategic factors in his favor wins.’

For two consecutive years, Trump has made massive, illegal policy blunders. I am already worrying about 2027. By that point, if current polling is any indication, Trump’s MAGA faction will have lost control of at least one house of Congress, and American-style autocracy will hopefully be in decline. But an unpopular, angry, and vindictive president will be licking his wounds, intent on retaliating ahead of the 2028 election cycle.

This is not a risk to take lightly. It will be up to a new congressional leadership to right the course for the US.

Sun Tzu gets the final word on that possibility: ‘Leadership is a matter of intelligence, trustworthiness, humaneness, courage, and sternness.’

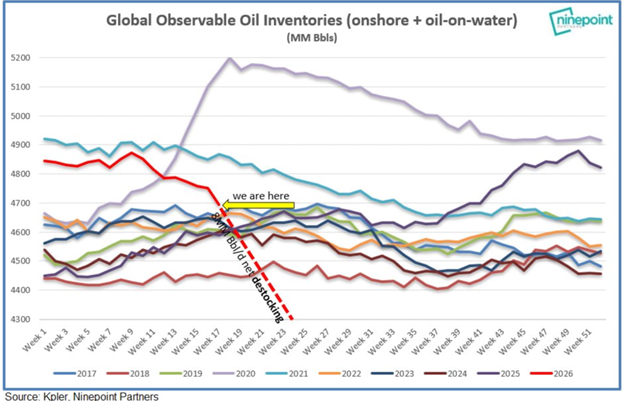

🛢️ Oil Flows Are, In Fact, Down (And the missing barrels are coming out of storage)

The International Energy Agency (IEA) reported that global oil inventories fell by 85 million barrels in March. Outside the Gulf, stocks dropped by another 205 million barrels as shipments through the Strait of Hormuz slowed.

Oil export losses from the Iran excursion now exceed 13 million barrels per day. At the peak, daily disruption moved above 12 million barrels. That is larger than the supply losses during the 1973 oil embargo and the 1978 to 1979 Iranian Revolution. (Source: Kpler, Ninepoint Partners)

Oil export losses from the Iran excursion now exceed 13 million barrels per day. At the peak, daily disruption moved above 12 million barrels. That is larger than the supply losses during the 1973 oil embargo and the 1978 to 1979 Iranian Revolution. (Source: Kpler, Ninepoint Partners)

In an effort coordinated by the IEA, member governments are releasing strategic reserves to keep fuel prices reasonable. Those barrels will replace the missing oil supply… for a while. As reserves fall, firms and end users will be forced to adjust. Airlines are already reducing routes. Trucking companies add or increase diesel surcharges. Fertilizer, if you can get your hands on some, costs more. Crop yields fall, food costs go up fast, “voters” feel the pinch months later.

Fuel is only one of the inputs the U.S. needs to keep production, transport, and military logistics running while competing with China. When supply tightens or tariffs impede supply lines, every one of those important economic activities becomes more expensive.

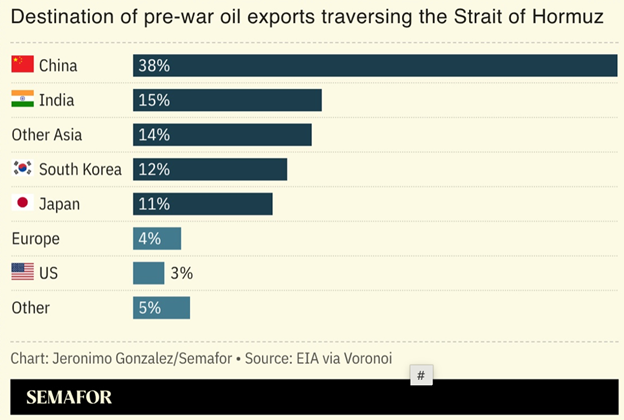

🚢 Trade Had Shifted Away From China (Before the ‘Energy Shock’)

Largely due to the shock and awe of the Trump tariff strategy, U.S. imports of goods from China fell by a third, from $438 billion in 2024 to $308 billion in 2025.

U.S. exports going the other way, to China, dropped by a similar fraction, from $143 billion to $106 billion.

Asian economies account for the highest share of trade disruptions through the Strait of Hormuz since the war began on February 28. (Source Semafor)

Outside the U.S., global trade still grew to about $35 trillion. Goods moved through Mexico, Vietnam, India, Taiwan, Thailand and Indonesia instead.

But each rerouted shipment added distance, handling, and cost. More ports, more inspections and more insurance. Companies carried additional inventory to avoid delays. That tied up cash and increased fuel costs per shipment.

Trade routes are but one lever in this historic shift in global competition. Changing the routes doesn’t stop trade, but it does change cost, speed and reliability.

🏛️ Bond Markets, Ultimately, Set Interest Rates

One leg of Project 2026 includes installing Kevin Warsh as chairman of the Federal Reserve, cutting the Fed funds rate and lowering borrowing costs across the economy. If you haven’t taken a moment to review our research and forecast the Warsh era at the Federal Reserve, please do so here: Trump’s 16-Day Profit Window.

Here we bump up against another historical anomaly. The Fed and Treasury can favor lower rates on the short end of the curve, but they may be powerless to control yield at the far end.

A post on X this morning by “Thierry from Arvy” raises the longer-term question:

“What if the biggest bubble of our lifetime isn’t crypto… or AI stocks… or real estate… but bonds?”

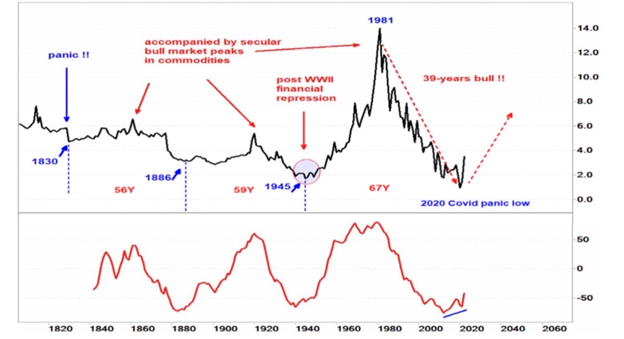

Even if it’s not politically expedient, interest rates have historically run on 50-60 year cycles since the founding of the republic 250 years ago. The post World War II spike then sell-off may have reached a cyclical bottom. Long-term interest rates have little room to go anywhere but up from here. (Source: Thierry fom arvy on X)

Even if it’s not politically expedient, interest rates have historically run on 50-60 year cycles since the founding of the republic 250 years ago. The post World War II spike then sell-off may have reached a cyclical bottom. Long-term interest rates have little room to go anywhere but up from here. (Source: Thierry fom arvy on X)

U.S. Treasury yields peaked near 14% in 1981 and declined to near zero by 2020. That decline lasted nearly four decades.

If yields rise over the next cycle, borrowing costs will increase across mortgages, corporate loans and government financing. Higher rates also increase the cost of building factories, data centers and military equipment.

Again, take a look at Trump’s 16-Day Profit Window.

📉 Stock Prices Do All The Heavy Lifting

Legendary investor Paul Tudor Jones rarely speaks in public these days. But in a recent interview making its rounds, Jones explained how much of the economy depends on equity values:

“We’re 252% of stock market cap to GDP.

In 1929 we were 65%. In 1987 we got to ~85–90%. In 2000, 170%.

If you get a 35% correction… you can see the budget deficit blowing up… you can see the bond market getting smoked…

The problem is that if you buy the S&P at this current valuation of PE 22, the 10-year forward return is negative…”

Capital gains contribute about 10% of U.S. tax revenue. When equity prices fall, that revenue declines. At the same time, household wealth drops and institutional portfolios lose value.

Equity prices are tied directly to funding. When they fall, the ability to finance spending — civilian or military — becomes more difficult.

🌏 Asia Keeps Production Running While Prices Move Higher

“If you know the enemy and know yourself,” Sun Tzu also says, “you need not fear the result of a hundred battles.”

The quote, also found in The Art of War, emphasizes that understanding both sides’ strengths and weaknesses is essential to victory, while ignorance leads to peril.

The rest of the quote portends an outcome a tad more dire: “If you know yourself but not the enemy, for every victory gained you will also suffer a defeat. If you know neither the enemy nor yourself, you will succumb in every battle.”

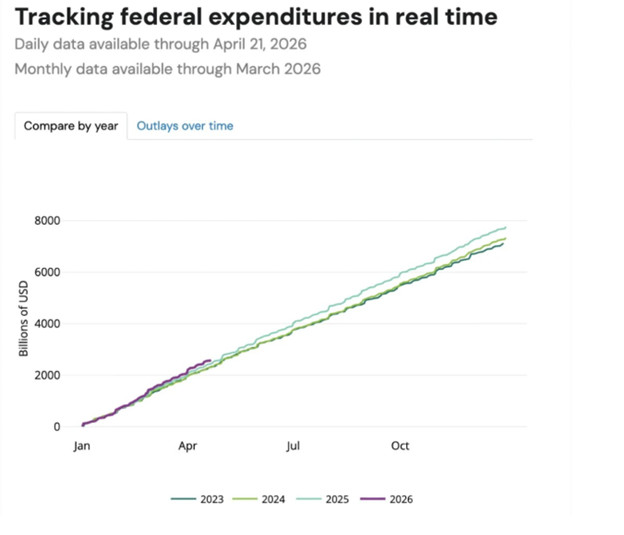

Federal expenditures month over month are increasing faster than in each of the previous three years. The government is already spending at crisis levels and has been since the pandemic lows of 2020. (Source: Federal Reserve)

While Trump and his administration are preoccupied with electoral politics, and financing the U.S. national debt, Asian economies continue to operate despite disruptions in oil supply.

Before the war, they imported roughly 90% of the crude passing through Hormuz.

Now they are relying on “efficiency improvements, electrification,” and technology to reduce fuel consumption per unit of output.

Like oil getting released from the strategic reserves in the West, China and its neighbors have limited the immediate impact of the Iran excursion.

Chinese leadership has directed investment toward water systems, power generation and computing infrastructure. The country entered the disruption with larger oil reserves and a faster buildout of renewable energy.

At the same time, export markets are slowing. A prolonged disruption in Hormuz will require the People’s Bank of China to employ additional fiscal or monetary support to maintain production levels.

The stakes are high. And getting higher. If Steven K.’s observation comes true and Trump cancels rather than postpones his trip to China, “all bets are off.”

To use a misattributed Chinese curse: “may you live in interesting times.”

~ Addison

P.S. Despite being so common in English as to be known as the “Chinese curse”, the saying is apocryphal, and no actual Chinese source has ever been produced. The saying says more about English speakers themselves than about mystic Chinese wisdom.

If you missed Grey Swan Live! last week with Zoltan Istvan, we got a whirlwind view of the future, Zoltan-style, which we dubbed “Robots, UBI, and Wine”…

In one stirring anecdote, Mr. Istvan described a recent letter he wrote to his wife. After three decades of buying, trading and developing real estate using the credit markets, they are planning for a “black swan” deflationary environment by deleveraging their real estate, something he’s never done with his own money…

I tried to persuade him to use the term “grey swan” instead, since it’s a trend he can see comin’. We’ll see if he comes around.

One curious story, while he’s planting more vines in his vineyard in Napa, he knows several other grape growers who are ripping their vines out of the ground, because it’s cheaper to let the land lie fallow than pay to deal with California’s onerous regulatory environment. Another sign of things to come?

Perhaps. Check out Zoltan’s interesting and very unique perspective on AI, the acceleration of change, and the future of value in the markets… stocks, bonds, real estate and tech. All very thought-provoking and worth a listen.

Plus, this week on Grey Swan Live!, we’ll team up with Jeff Opdyke to talk about what he believes could be one of the most important opportunities for retirement investors in the next decade. Learn more here…