After five days in Panama, we thought we’d return to market chaos.

After all, the United States has been conducting what the Pentagon politely calls an “operation” against Iranian military infrastructure. The Strait of Hormuz — the narrow passage through which roughly a fifth of the world’s oil flows — has become a chessboard of tankers, mines and nervous insurance underwriters.

Markets had every reason to be panicky.

Instead, the past week delivered something subtler. Here are the five dominant trends shaping the market while we were away:

- Oil surged toward $100 a barrel, driven by supply fears and reported mine deployments in the Strait of Hormuz. Energy stocks outperformed most of the market.

- Technology shares pulled back, particularly among the “Magnificent Seven,” as enthusiasm for artificial intelligence (AI) ran into valuation fatigue and intensifying competition.

- Major indexes slid to new 2026 lows, with the Dow, S&P 500, and Nasdaq all falling as investors trimmed risk exposure amid geopolitical uncertainty and persistent inflation pressures.

- Money rotated into defensive sectors, including utilities, consumer staples and industrial companies that tend to hold up better when investors become cautious.

- Financial shares weakened, as growing anxiety over the $2 trillion private credit market began to ripple through Wall Street balance sheets.

None of these developments happened in isolation. Each connects to the same larger theme: capital is becoming more cautious in a world that suddenly looks less predictable.

Go figure.

💣 Oil Near $100 and the Echo of 2007

Energy traders spent the week watching crude oil prices creep higher as tensions around the Strait of Hormuz intensified. Brent crude briefly closed above $100 a barrel, the first time since 2022.

History has a way of whispering when energy prices spike alongside financial stress.

Bank of America strategist Michael Hartnett recently pointed out that oil followed a similar path during the early stages of the 2008 financial crisis. Prices rose from roughly $70 to $140 per barrel even as cracks began forming in mortgage markets months before Lehman Brothers collapsed.

We’re seeing a similar pattern today….

Oil is climbing again. And somewhere else in the financial system, something appears to be tightening.

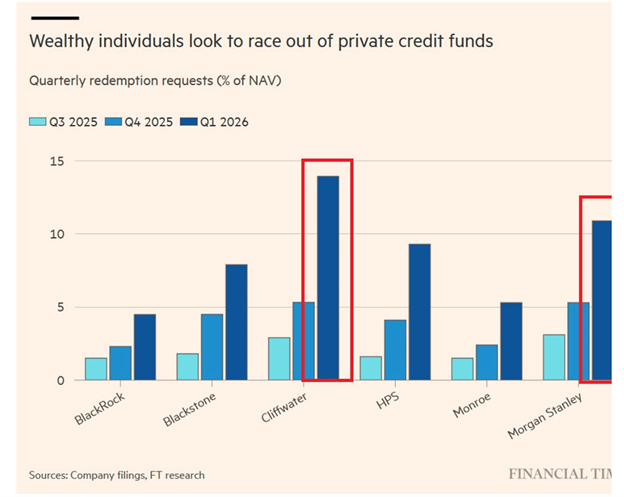

🏦 Private Credit Starts to Squeak

That tightening is coming from private credit, the $2 trillion lending ecosystem that grew rapidly after the 2008 financial crisis as banks retreated from riskier lending.

According to reporting in the Financial Times, wealthy investors have already requested more than $10 billion in withdrawals from several of the largest private credit funds during the first quarter of 2026. (Source: Financial Times)

Redemption requests for private credit funds have tripled since third-quarter 2025.

Some funds are feeling the pressure more than others. Cliffwater reported redemption requests equal to about 14% of net asset value, meaning investors attempted to withdraw roughly 14cents of every dollar invested.

Morgan Stanley funds saw about 11% requested withdrawals, while HPS Investment Partners reported roughly 9.5%.

Managers have agreed to honor only around 70% of those redemption requests, forcing investors to wait for the rest of their money.

Meanwhile, publicly traded private credit firms — including Blackstone, KKR, Blue Owl, Ares and Apollo — have lost more than $100 billion in combined market value this year, with many shares down roughly 25% year to date.

Wall Street veterans hear a familiar sound in those numbers.

In August 2007, BNP Paribas froze withdrawals from three mortgage funds tied to subprime securities. That decision didn’t cause the financial crisis, but it was one of the first visible signs that liquidity inside the system had begun to stiffen.

Private credit may or may not follow that same path. For now, investors are asking a simple question.

Can the stress stay contained?

🧠 AI Euphoria Starting To Meet Gravity

While credit markets are beginning to creak, the technology sector is experiencing its own reality check.

The so-called “Magnificent Seven” tech giants have been trading unevenly as investors reconsider the price tags attached to AI.

A year ago, almost any company that mentioned AI on a conference call could expect a pop in its share price. Now, even retail investors have gotten the memo and are starting to ask harder questions:

- How quickly will these systems generate real profits?

- How fierce will competition become?

- How many billions must companies spend on data centers before the revenue arrives?

High-growth software companies have taken the brunt of the skepticism. Some have dropped sharply as capital rotates toward sectors with steadier cash flows.

It’s a pattern as old as the market itself. First comes the technology. Then comes the excitement. Then comes the math.

🔁 The Great Rotation Picks Up Speed

While technology stocks have stumbled, professional investors have quietly shifted capital elsewhere.

Utilities, consumer staples and industrial companies have all attracted new interest as portfolio managers search for stability amid an uncertain geopolitical environment.

Energy shares have been the clearest beneficiaries. When oil rises, balance sheets across the oil patch tend to improve quickly.

The shift is subtle but important. Among the pros, the money rarely leaves the market entirely. More often, it simply changes neighborhoods.

That is, until there’s a crisis and everyone sells and everything gets sold.

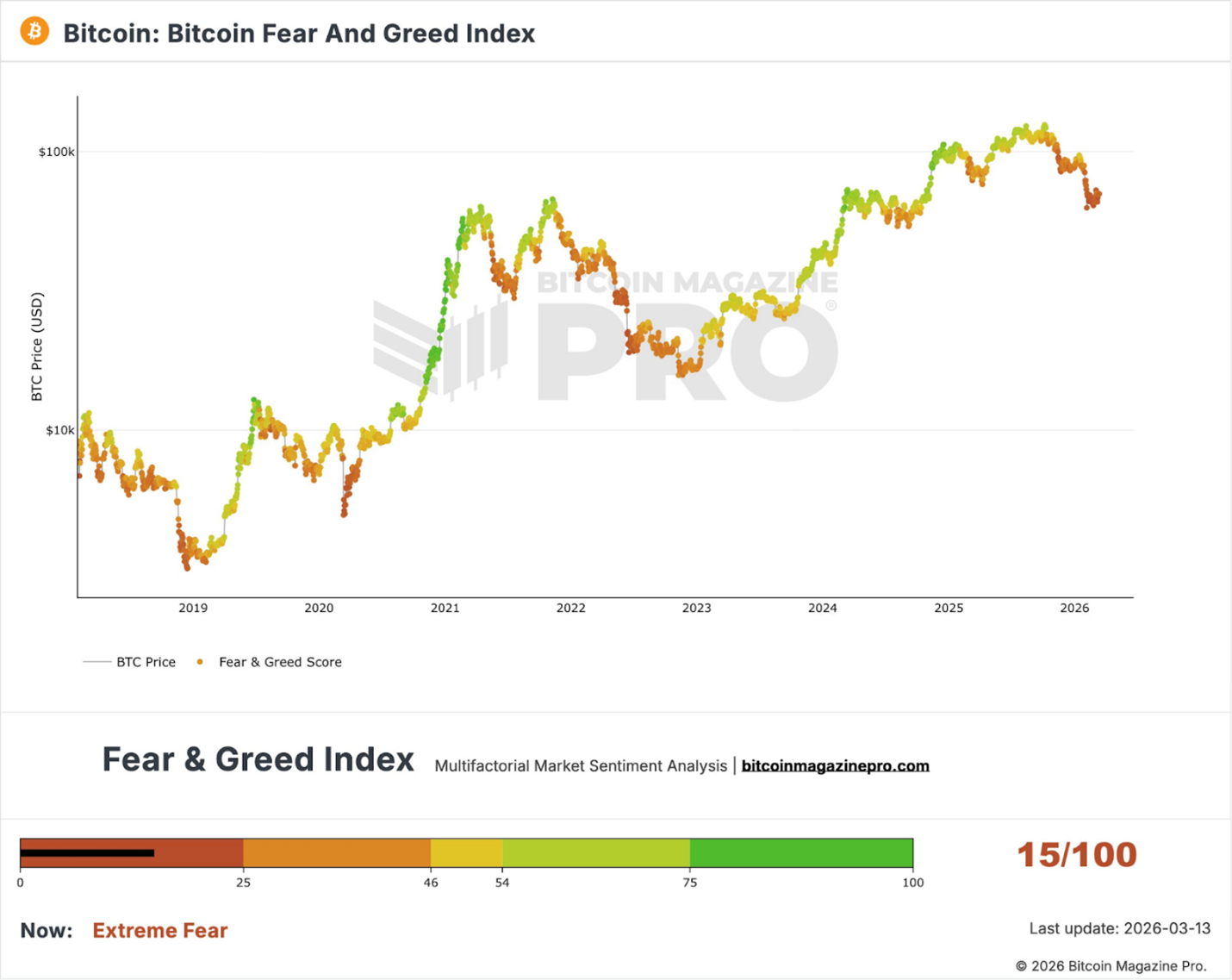

🪙 Bitcoin Stirs While Gold Sleeps

One of the stranger developments during the past few weeks has been the behavior of traditional safe-haven assets.

Gold has remained mostly flat despite rising geopolitical tension. For the immediate term, the precious metal appears to be digesting the massive rally it experienced over the past few years.

Meanwhile, bitcoin is showing signs of life; a trend Andrew and I observed in the Grey Swan Trading Fraternity live event last Wednesday.

After falling roughly 50% between October and February, the world’s most popular cryptocurrency has rebounded to around $74,000 and may be eyeing a move toward $80,000.

One possible explanation is mechanical. Bitcoin tends to move faster in both directions than gold. A 50% drawdown can unfold in months rather than years.

Supply dynamics also play a role. Bitcoin’s maximum supply is fixed, and exchange balances have been shrinking while money flows into bitcoin ETFs.

When supply tightens and demand begins to return, prices tend to notice — even if markets are still in fearful conditions.

Although bitcoin has started to move well off its panic lows from February, and inked a one-month high today, it’s still at levels of extreme fear. (Source: Bitcoin Magazine)

Andrew Packer noticed, too. He plied his adept skills and the Grey Swan Indicator and issued an options trade this morning in the Grey Swan Trading Fraternity that will do well if this move in bitcoin has real legs.

If you’re interested in making money by trading the macro trends we observe in Swan Dive, you’ll want to join the Grey Swan Trading Fraternity, too. On average, Andrew has been issuing 1-2 trades a week.

📉 The Incredible Vanishing Rate Cuts

Interest-rate expectations have shifted dramatically during the past several weeks.

After new data from the Bureau of Economic Analysis (BEA) showed weaker-than-expected growth, traders began aligning their outlook with the Federal Reserve’s more cautious projections.

Private sales to domestic purchasers — a closely watched measure of underlying demand — rose only 1.9% in the latest report, a full percentage point below the previous quarter.

As that data arrived, expectations for aggressive rate cuts quickly faded.

December 2026 Fed Funds futures now imply rates around 3.44%, nearly 40 basis points higher than at the end of February.

Market pricing suggests traders now believe they might see one rate cut this year… or perhaps none at all.

In other words, the era of easy money may remain a little further away than investors had hoped… or President Donald Trump has promised.

💵 The Dollar’s Long Story

All of these developments — oil shocks, private credit stress, interest-rate expectations — exist within a longer monetary narrative.

In a recent conversation with Demetri Kofinas, economic historian Barry Eichengreen traced the lineage of global currencies from ancient Lydia to modern stablecoins.

Each dominant currency in history has emerged from a combination of political stability, financial infrastructure and trade networks.

Athens developed early monetary systems that helped power Mediterranean commerce. The Dutch Republic refined modern banking and finance. Britain built a global financial system that anchored the pound sterling during the 19th century.

The United States inherited that mantle during the 20th century through a combination of the Federal Reserve system, two world wars and the Bretton Woods agreement.

Even after Bretton Woods collapsed in 1971, the dollar retained its position through the global network of trade and finance built around it.

The question Eichengreen raises today is not whether the dollar disappears tomorrow. The real question is whether the world eventually transitions toward a system without a single dominant reserve currency at all.

Such a system would look less orderly than the one investors had grown accustomed to over the past 70 years.

⚓ Panama and the Long Memory of Empire

On March 11, 1802, Congress founded the United States Military Academy at West Point to train officers in the theory and practice of military science.

The academy sits on a commanding bend of the Hudson River, where a Revolutionary-era fort once guarded the valley against British invasion.

In 1780, General Benedict Arnold attempted to surrender the fort to the British in exchange for 6,000 pounds, but the plot was uncovered before the deal could be completed.

West Point would later train generations of officers whose assignments stretched far beyond the Hudson Valley.

Among those missions was helping construct and defend the Panama Canal, one of the most important engineering projects of the 20th century.

Following a failed French attempt, the U.S. Army Corps of Engineers completed the canal between 1904 and 1914 under the leadership of Colonel George Washington Goethals. The canal quickly became a strategic artery for global trade and naval power.

The United States treated the canal as a vital national security asset for decades. During World War II, thousands of troops and anti-aircraft defenses protected the waterway from sabotage.

The Canal Zone, a 10-mile-wide strip of territory surrounding the canal, remained under American control throughout the Cold War.

The military presence eventually wound down following the Torrijos-Carter Treaties, culminating in the full transfer of the canal to Panama on December 31, 1999.

We visited the Canal Museum in Panama City on Saturday and spent about an hour longer there than our (already-packed) itinerary allowed for.

The exhibits tell the story of how engineering, trade and geopolitics intersect in narrow passages of water, or as the military refers to them, “chokepoints.”

With the world’s attention fixed once again on the Strait of Hormuz, the lessons available in the Canal Museum felt especially prescient on Saturday. The canal moves ships slowly across the Isthmus. Capital decides where it anchors.

— Addison

P.S. This week in Grey Swan Live!, we have another two-fer. The recording from Panama City during The Gathering with Ronan McMahon will be posted soon.

In the interview, Ronan and I explore the Ipanema and Caracol briefings in the context of infrastructure, canal exposure, jurisdiction and long-term capital allocation.

You’ll also get a great overview of why we include the deals from Real Estate Trend Alert (RETA) in our resources available to Grey Swan Investment Fraternity.

Not only do they offer international diversification for your portfolio, but Ronan also insists that most RETA members are even more enthusiastic about the lifestyle choices they offer.

Then, Thursday, March 16, 2026, Grey Swan Live! will return to its regular time slot at 2 p.m. ET/11 a.m. PST.

This Thursday, we’ll be joined by our natural-resources specialist, Shad Marquitz, for a prescient look at volatility and opportunity in oil, energy, rare earths and precious metals following the Iran bombing excursion.