In another misspent chapter of my youth, I lived as a ski bum in Telluride and then in Gunnison, just down the road from Crested Butte. The locals had a way of sorting themselves from the lift-line tourists. “Free the heel, free the mind.”

Telemark skiers fixed only the toe of the boot, leaving the heel free to rise and fall through each turn. The motion demanded a lunge, a kind of controlled imbalance that matched the terrain instead of fighting it.

You could cover more ground that way, reading the slope rather than imposing a rigid line on it. “Alpine” skiers, those with the conventional fixed heel, looked at telemark skiers and thought they were crazy. In our view, the tourists lacked imagination and a sense of adventure.

Monetary policy faces the same decision. Fix the heel, and you get stability that will snap under pressure. Free it, and the economy can absorb the unknown terrain and adapt.

Kevin Warsh, President Donald Trump’s nominee to replace Federal Reserve Chair Jerome Powell, has a proposal for a modern accord between the Fed and Treasury that would free the Fed from the responsibility of rigidly managing the economy through interest-rate manipulation and financial dominance.

In our view, the economic establishment should pay attention… and grow a pair.

🏦 The Market Already Drew the Line

In late March, interest-rate expectations reset at a speed traders usually associate with crisis periods.

Analysis from The Kobeissi Letter places the first expected rate cut in December 2027. A month earlier, desks debated three to four cuts in 2026. Futures markets now assign roughly a 51% probability to a rate hike by March 2027.

One-year inflation expectations moved above 5.0%, the highest level since the current tightening cycle began.

The move tracked oil, which has been driven higher by Gulf disruption and rerouted supply chains. Treasury yields adjusted higher in response, with the forward curve flattening through at least September 2027.

Treasury auctions cleared at higher yields as $100-plus oil fed directly into inflation breakevens and forced buyers to demand more compensation. Duration risk repriced. Mortgage rates moved toward 7%. Corporate borrowing costs widened.

The market has already set the marginal price of money. The Fed now chooses whether to follow that signal or override it.

⚡ The Energy Shock the Fed Cannot Fix

The current fear of inflation is driven by energy logistics rather than domestic demand.

The kerfluffle in the Gulf over the Strait of Hormuz is forcing tankers laden with all sorts of necessities for modern civilization (including helium critical for chip manufacturing) to reroute around the Cape of Good Hope, adding thousands of nautical miles and up to two weeks of transit time.

Insurance premiums have skyrocketed for fear that the ships will be swarmed by attack drones. Refiners are bidding for cargo based on delivery certainty as much as price.

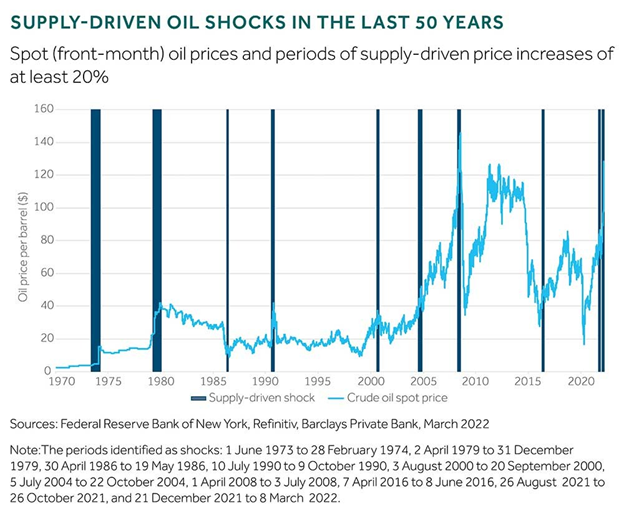

In a media blitz following S&P Global’s annual energy conference, co-chair Daniel Yergin described the current disruption as the largest dislocation in oil markets in modern history, surpassing the shocks of 1973 and 1979 in immediate impact on flows.

The conference agenda at CERAWeek shifted within hours from AI and electrification to supply security and affordability.

The Fed does not produce oil. It does not secure shipping lanes. It does not shorten transit routes or rebuild damaged infrastructure.

It sets the price of money. And right now, it is poised to make an egregious error simply by following the Fed’s “data-driven” rate policy decision-making process.

When that price rises in response to an energy shock, the cost moves through the system in a straight line — higher borrowing costs for households, higher hurdle rates for businesses and higher financing costs for government issuance.

On top of that, the Fed under Powell wants to keep rates steady. Some on the board of governors have argued they should follow other G7 central banks and raise rates. Yesterday, Powell said no.

No bueno.

🏭 Goodspeed’s Mechanism: How Expansions Get Killed

In his new book, Recession: The Real Reasons Economies Shrink and What to Do About It, ExxonMobil chief strategist Tyler Goodspeed argues the Fed is likely to exacerbate the impact of the Iran “energy shock”.

The work compiles roughly 350 to 400 years of economic history across the United States and the United Kingdom, building annual recession chronologies back to 1700 and quarterly data from 1854.

Across that dataset, expansions do not expire on their own. They get interrupted. War, energy price spikes and supply shocks appear repeatedly as the initiating events.

Energy shocks show up in nearly every U.S. recession since 1945. War ranks as the most destructive force across the full historical sample.

History shows that oil price spikes often precede a recession, as higher energy costs result in a cutback in spending in other parts of the economy. The Fed can only make it worse. (Source: Federal Reserve)

Weather disruptions — crop failures, transport breakdowns — play the same role in earlier centuries. The 2020 pandemic lockdowns were in a category all their own.

Across the centuries, the sequence runs the same way. A shock reduces supply. Prices rise. Policy responds to those prices. Credit tightens. Investment slows. Output falls below the trend and does not recover the lost ground.

Goodspeed identifies policy as an accomplice rather than the origin.

Credit controls, rate hikes and delayed responses extend the damage once the shock has already taken hold.

Goodspeed cites episodes in 1948, 1970 and 1980 where tightening cycles reduced access to financing and prolonged downturns.

In the present case, oil prices driven by war feed into inflation data. If the Fed responds to that data with higher rates, it raises the cost of capital precisely where new supply and productivity gains would otherwise emerge.

⚙️ Warsh’s Proposal: Free the Fed

Warsh’s critique lands on the Fed model itself. The Fed reacts to trailing indicators: CPI, employment revisions and other lagging measures of economic activity that reflect conditions already in motion.

Warsh’s proposed “modern accord”: with Treasury updates the 1951 framework for a system now carrying nearly $39 trillion in federal debt. The Fed maintains monetary credibility. Treasury manages its own debt. Capital markets determine the clearing price of funds.

Under that structure, the Fed does not attempt to offset an energy-driven inflation impulse with tighter policy. It avoids amplifying the shock.

The operating principle reads cleanly: Mr. Powell, first do no harm.

Free the Fed, free the mind.

🎢 The Warsh Shock

Warsh’s approach introduces a second-order effect that trading desks have already begun to map. Lower rates under a forward-looking framework do not include a commitment to support asset prices.

Capital becomes cheaper at the margin. Risk increases for the investor.

Companies embedded in infrastructure — power generation, transmission, data centers — retain access to capital. Firms controlling proprietary data or operating within regulated systems continue to issue debt.

Single-product software firms, IT consultants and businesses without durable data advantages face wider spreads.

Goldman Sachs notes that credit spreads for software issuers have widened by more than 250 basis points this year, raising borrowing costs unevenly across the sector.

The AI buildout itself requires roughly 500,000 additional workers in power and grid-related roles by 2030.

Construction crews, electricians, engineers and lineworkers fill the gap as data centers scale. Lower rates facilitate that buildout. And the market determines at what rate they’re willing to borrow in order to read the economic terrain.

At the same time, the absence of a policy backstop forces capital discipline.

In Warh’s view, the Fed’s response should be: “You break it, you own it.”

Projects succeed or fail based on cash flow and execution, not on the expectation of rescue. After two decades of Fed intervention, ZIRP and QE 1, 2, 3, 4… the market recoils at the very thought of it.

The “Warsh Shock” is the sell-off that would arise upon his confirmation to the chairman’s post. In our view, the Warsh Shock would be as temporary as the energy shock would be, too, after a quick cessation in hostilities in Iran.

📉 The Alternative: Tightening Into the Shock

If the Fed holds rates steady or raises them in response to oil-driven “Energy Shock” inflation, the effect moves through balance sheets immediately. Then sits around and hampers the many productive benefits that can and should be accrued from AI adoption.

Borrowing costs rise across consumer credit, mortgages and corporate issuance. Venture funding slows. Capital expenditure gets deferred. Hiring pauses in sectors already adjusting to AI displacement.

Goldman Sachs estimates roughly 300 million jobs globally are exposed to AI automation, with about 25% of U.S. work hours susceptible to automation. Workers displaced from knowledge industries do not move easily into the physical infrastructure roles now in demand.

An AI-driven expansion depends on upfront investment — compute, power, logistics and skilled labor.

And cheaper credit. The Fed could royally screw that up simply by keeping its heel fixed in its existing model.

🗼 How Innovations Find Their Way To the Mainstream

On March 31, 1889, Gustave Eiffel climbed a structure that many Parisians wanted dismantled before it was finished. More than 100 design proposals had been submitted for the Exposition Universelle.

Eiffel’s iron lattice tower — 984 feet tall, supported by four masonry piers and connected by curved columns — was selected and then immediately criticized.

Artists signed petitions calling it an eyesore. Engineers questioned its stability. The elevators, designed by the Otis Elevator Company, were not yet operational on opening day.

The Eiffel Tower shocked and awed citizens of Paris when it was erected for the Exposition Universelle in 1889. Now it attracts 7 million visitors to Gay Paris each year. (Source: The History Channel)

The Eiffel Tower shocked and awed citizens of Paris when it was erected for the Exposition Universelle in 1889. Now it attracts 7 million visitors to Gay Paris each year. (Source: The History Channel)

Eiffel climbed the stairs himself with a small group and raised the French tricolor at the top. Fireworks were set off from the second platform. The exposition opened weeks later with the tower as its entrance.

The philosopher Arthur Schopenhauer famously described the progression of new ideas in three stages: ridicule, opposition and acceptance. The tower passed through each. It later served as a radio transmission point, and it was preserved when its 20-year lease expired in 1909.

The structure still stands. Eiffel himself reached the summit on foot and hoisted the flag.

~ Addison

P.S. Grey Swan Live! returns this week with Ian King, this Thursday at 2 p.m. ET.

While financial markets have seen big price swings over the past few weeks, AI development rolls on. And the crypto markets move, glacially, towards increased clarity. Ian has his eye on the pulse of the markets

Ian’s view of the Clarity Act and Defi revolution, covering everything from tokenization to all our “Dollar 2.0” ideas to modernize the U.S. dollar and financial system – are key topics for discussion.