Every generation eventually discovers that the economic rules it grew up with were not permanent after all.

We found ourselves quoting Heraclitus this week during a conversation in which our oldest son was trying to decide his next moves, his job and prospects. He is happy with the position he’s in and the work he’s doing, but the restaurant around him is making surprising changes.

Apparently, Heraclitus never actually said the exact phrase “the only constant is change.” But you get the idea. The Greek philosopher “flourished” some 2500 years ago, halfway around the planet from us, but in this one paraphrased quote aptly nailed the sentiment.

The investors who came of age during the long bull market of the 1980s and 1990s learned to trust a world in which inflation generally drifted lower, interest rates followed suit and globalization seemed capable of producing an endless supply of inexpensive goods.

Factories moved overseas, supply chains stretched across oceans, and capital flowed effortlessly toward software, finance and businesses that could grow without much physical infrastructure.

That arrangement produced extraordinary wealth. It also created habits of thought that may become increasingly dangerous during the decade ahead.

It also created this extraordinary investment opportunity:

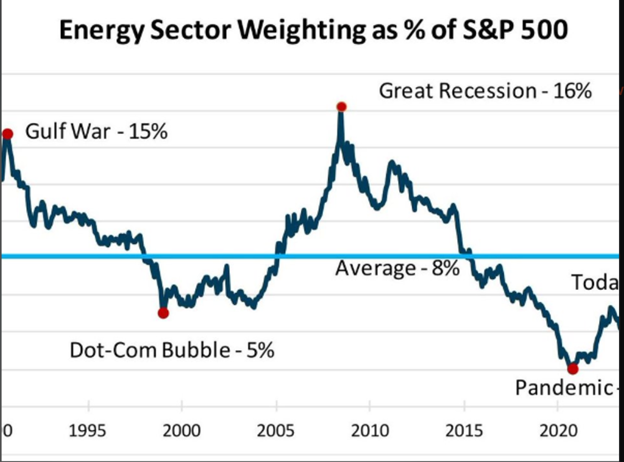

Despite pandemic-era economic lockdowns, broader trends have driven the allocation of S&P 500 capital to historic lows. We first identified the opportunity several years ago, when we published a small start-up we called The Wiggin Sessions. (Source: Andrew Packer, X)

One reason so many investors feel disoriented today is that they continue trying to interpret new developments through a framework built for a different era.

Artificial intelligence gets discussed primarily as a technology story. Tariffs are discussed as a trade policy. Gold gets discussed as a hedge. Treasury yields get discussed as a bond-market problem.

Yet the deeper forces driving all those investment theses are, or at least appear to be, connected. At a time when the AI data center and infrastructure build out is creating record energy demand… why is the energy sector valued at a mere 3.2% of the S&P 500 Index?

“The Great Race,” which we’ve introduced to you this week, is simply our attempt to describe what’s actually happenin’.

⚡ From the Age of Cheap Money to the Age of Competition

For most of the past forty years, the global economy rewarded efficiency above almost everything else. Businesses built supply chains wherever costs were lowest. Governments generally preferred stable trade relationships to industrial rivalry.

Investors rarely needed to think very hard about where copper came from, who controlled energy supplies or whether semiconductor production concentrated too heavily in one part of the world because the system appeared to function smoothly enough that those questions remained largely invisible.

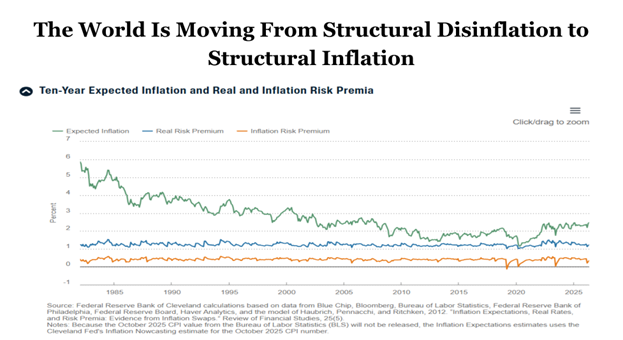

Global inflation has evolved far beyond the post-pandemic supply shock most investors originally expected. What began as temporary disruptions tied to stimulus spending, supply chain bottlenecks, and reopening demand has gradually transformed into something far more structural. (Source: Federal Reserve Bank of Cleveland)

The pandemic exposed many of those assumptions. So did the war in Ukraine. So did the growing rivalry between the United States and China.

Today, governments increasingly concern themselves with access to energy, semiconductor manufacturing, critical minerals and industrial capacity because each of those inputs now carries strategic importance. Countries are no longer simply trying to maximize efficiency. They are trying to reduce vulnerabilities.

That shift carries consequences.

When multiple nations simultaneously pursue the same resources, the result tends to be higher costs, longer construction timelines and greater competition for labor and capital. The inflationary pressures emerging from those dynamics look different from the temporary price spikes policymakers spent years debating after the pandemic. They increasingly resemble the early stages of a world where industrial competition becomes a permanent feature of economic life rather than a temporary disruption.

🛢️ The Industrial Side of Artificial Intelligence

Artificial intelligence sits at the center of this story because it highlights the difference between how investors see the world and how the world actually works.

Most people encounter AI through applications. They use chatbots, search tools and software platforms. Those experiences naturally lead investors toward technology companies, as software remains the most visible layer of the stack.

Beneath that layer sits a vast industrial system.

Nvidia (NVDA) CEO Jensen Huang has repeatedly described the AI economy as a multi-layer structure resting upon energy generation, semiconductor manufacturing, data centers and cloud infrastructure long before consumers ever interact with the applications themselves.

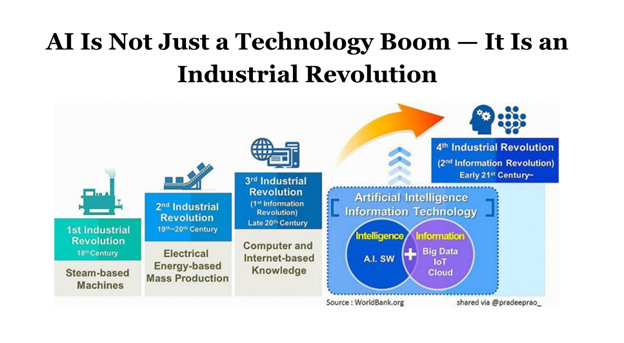

Much like electricity, the internet, or mobile computing before it, AI is beginning to reshape how businesses operate, how capital is allocated, and how productivity scales across entire industries. (Source: WorldBank)

That observation helps explain why utility executives, pipeline operators, electrical-equipment manufacturers and natural-gas producers increasingly find themselves participating in conversations that supposedly revolve around artificial intelligence.

The technology may feel futuristic. Building it requires concrete, steel, copper, electricity, cooling systems and financing.

That reality is already reshaping investment flows. Utilities once viewed as sleepy income investments suddenly find themselves discussing unprecedented demand forecasts. Data-center developers increasingly compete for access to electrical generation. Nuclear energy, which spent years wandering through the financial wilderness, has reentered conversations about long-term power supply. The physical economy keeps showing up beneath what many investors still describe as a software revolution.

📈 The Bond Market And Regime Change

Meanwhile, the Treasury market continues delivering one of the most important signals in global finance.

The Federal Reserve cut rates six times between September 2024 and December 2025. During much of the past forty years, that would have led long-term yields to decline as investors anticipated slower growth and easier financial conditions.

Instead, long-term yields remain elevated.

Long-term Treasury yields continued climbing as investors demand higher compensation for holding U.S. debt amid ballooning deficits, sticky inflation pressures and growing doubts that rate cuts alone can stabilize the economy. (Source: TradingView)

Bond investors appear increasingly concerned that the next decade may require enormous spending on industrial infrastructure, energy systems, semiconductor capacity, military modernization and technological competition at precisely the moment government debt already sits near historic highs.

That concern helps explain why Kevin Warsh has become such an important figure. His challenge extends beyond managing inflation. He inherits a Treasury market seeking reassurance that America’s financial foundations remain credible even as the country embarks on one of the largest industrial transitions in generations.

The bond market is not forecasting catastrophe.

It is asking whether the promises accumulated during the age of globalization remain compatible with the investments required by the age of artificial intelligence.

Those are not necessarily the same thing.

🌎 Following the Logic of the Trump Reset

Many observers still treat the Trump Administration’s actions as a collection of disconnected events.

One week brings tariffs. Another brings discussions with Saudi Arabia. Then come semiconductor restrictions, stablecoin legislation, critical-mineral negotiations or renewed interest in energy development.

Viewed individually, each story appears to belong in a different section of the newspaper. Viewed together, a broader pattern emerges.

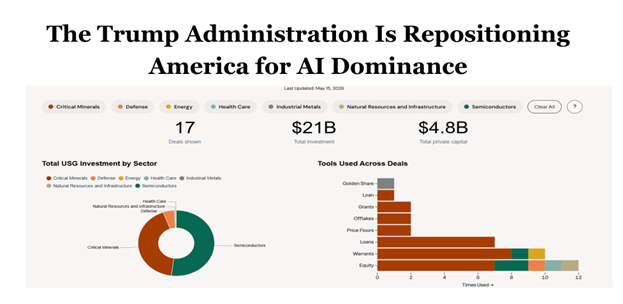

From reshoring semiconductor production to securing energy infrastructure and accelerating domestic manufacturing, Trump’s strategy goes far beyond tech policy alone. (Source: Grey Swan)

The administration increasingly appears focused on positioning the United States to dominate the infrastructure supporting the global AI economy. That objective extends far beyond software. It touches energy production, semiconductor manufacturing, resource security, capital formation and the future architecture of the dollar itself.

That is where Treasury Secretary Scott Bessent’s enthusiasm for stablecoins begins fitting into the same conversation as Kevin Warsh’s focus on Treasury-market credibility.

It is where Dollar 2.0 comes into play. And it is why energy policy, industrial policy and monetary policy increasingly resemble interconnected parts of a single national strategy rather than separate policy debates.

The administration seems to understand something many investors are only beginning to appreciate: artificial intelligence may ultimately become less important as a software story than as an industrial story.

And industrial stories tend to reward different assets than software stories do.

🧠 Savvy Old Guys, Maybe We Ought To Listen…

One reason The Great Race matters is that investors do not have to speculate entirely about how this transition might unfold.

Some of the world’s most successful capital allocators have been repositioning for years.

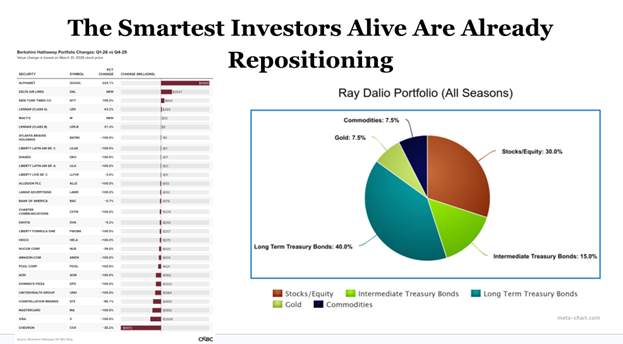

Warren Buffett continues allocating enormous sums toward energy and industrial assets while maintaining unusually large cash reserves. Ray Dalio regularly warns about debt cycles, currency pressures and geopolitical fragmentation while maintaining exposure to hard assets and commodities. Stanley Druckenmiller frequently discusses energy shortages, industrial rebuilding and the consequences of underinvestment in resource production.

The old playbook built around cheap money and endlessly expanding valuations is becoming harder to rely on. Rising bond yields, persistent inflation pressures, geopolitical fragmentation, and massive AI-driven capital spending are all forcing a rethink of where money flows next. (Source: Meta-Chart)

Their approaches differ. Their time horizons differ. Their portfolios certainly differ.

Yet all three appear increasingly attentive to the same underlying reality: the physical economy matters more than many investors have grown accustomed to believing.

That does not mean technology becomes unimportant. Quite the opposite. Artificial intelligence may become one of the most important economic developments of the century.

But every data center still requires power. Every semiconductor plant still requires construction. Every electrical grid still requires maintenance. Every industrial renaissance still depends upon resources, labor, financing and infrastructure.

History often rewards investors who recognize those relationships before they become obvious.

“The Great Race” may ultimately prove to be one of those moments when understanding the plumbing becomes just as important as admiring the architecture.

~ Addison

P.S. Investors spent much of the past generation studying balance sheets, software metrics and central-bank statements. The next generation may spend considerably more time studying electrical grids, energy supplies, semiconductor fabs and commodity flows.

The market has a habit of telling us what matters long before economists find the right vocabulary to explain it. Present company included.

“Chapter 47”, if you’ve been following along this week, is an investigation of how President Trump could possibly address the historically unnerving level of U.S. government debt.

If you’re a paid-up fraternity member, you won’t want to miss the Grey Swan Live! Andrew and I recorded yesterday. We dig deep for about an hour into the thesis that is driving the Fraternity forward. Take a look: