Traders focused on what they could on the Middle East yesterday, but the tape had other plans.

Oil pulled back from recent highs and equities drifted higher into the close, with the S&P 500 finishing within roughly 4% of its all-time highs despite an active shooting war in the Persian Gulf.

The ratio between short-term and long-term VIX futures climbed above 1.0, reaching its highest level in eleven months. (Source: Bloomberg)

The ratio between short-term and long-term VIX futures climbed above 1.0, reaching its highest level in eleven months. (Source: Bloomberg)

The rising VIX threatens the relative serenity we’ve been observing across the headline indexes. While WTI crude oil is up 65% year to date, the S&P 500, Dow and Nasdaq are down a scant 2-3% respectively.

Year to date, gold and silver have each tacked on roughly 20%.

In the futures market, traders paid more for protection from the military excursion in Iran over the next few weeks than for protection months out.

That noticeable inversion typically appears when hedging demand concentrates around immediate uncertainty rather than any long-term structural risk.

At the same time, the one-month put-call skew on the S&P 500 pushed toward 12 points, the highest level since December 2021, just before the 2022 bear market began.

As Andrew Packer will tell you in the Grey Swan Trading Fraternity, options markets showed a willingness to pay a premium for downside insurance relative to upside participation – in addition to the higher cost in the options space for elevated volatility.

Meanwhile, asset managers sold a near-record amount of S&P 500 futures last week. Hedge funds reduced exposure at one of the fastest rates on record.

Commodity trading advisors liquidated approximately $75 billion in global equities over the past month and are approaching a net short position.

The market’s headline indexes have held their ground, relatively speaking, among all the Persian Gulf hand-wringing. It’s worth a closer look at what’s causing this unique setup.

🔁 Retail Investors Keep the Floor Intact

The fund managers are short the index through futures and ETFs while remaining long individual equities.

As bearish options expired without paying out, dealers who sold those options have been forced to “unwind” their hedges.

The unwind requires buying back stocks and helps to keep the index afloat. Each expiration cycle creates enough demand for large index stocks that the indexes have barely moved, even with higher volatility (VIX).

At the same time, as we’ve been noting for months now, retail investors have been buying into equity mutual funds and ETFs at a historic pace.

Inflows remained steady, providing another layer of demand beneath the market and causing the bearish puts to expire worthless.

The result is a market that absorbs negative news about the progress in the Gulf with ease. If prices remain in the -2% to -3% range, the unwind process continues to generate new buying, ad infinitum.

In our forecast for Grey Swan in 2026, we anticipated a rise in stock indexes, enabling individual investors to squeeze out professional short positions. We still anticipate the cycle will end in a crack-up boom at some point.

What we didn’t forecast is that it would go on as long as it has. Or to such a remarkable degree.

The market’s throwing twists in the story on the screen… as the tension builds, the suspense is killing us!

⛽ Energy Costs Move Into the Real Economy

While equities held steady, energy prices moved through the system with more force.

The average retail price of gasoline rose $0.49 in a single week to $3.63 per gallon, the highest level since June 2024. Prices are now up $0.73 from early January and nearly 14% higher than a year ago, reversing a long stretch of year-over-year declines.

Diesel prices surged more than 36% over the past month.

That increase is passed directly onto the prices consumers pay. Farmers pay more to run equipment. Trucking firms pay more to move goods. Retailers absorb higher distribution costs before passing them along.

Electricity prices and natural gas have already been rising. Gasoline is now catching up.

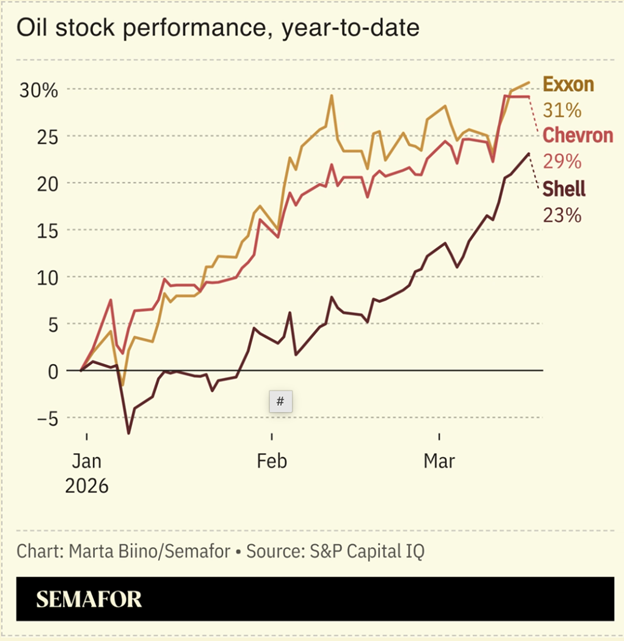

Some clear early winners during the Iran excursion of 2026. (Source: SEMAFOR)

Brent crude traded near $104 per barrel after renewed strikes on energy infrastructure and shipping routes in the Gulf.

Iranian officials indicated that disruptions would target tankers associated with specific countries. Traffic through the Strait of Hormuz remains constrained, and insurers continue to reprice risk for vessels entering the region.

The United States exports liquefied natural gas, crude oil, diesel, gasoline and jet fuel. As foreign demand increases amid supply disruptions, domestic prices rise to meet global bids.

Energy economist Philip Verleger told Reuters, “The costs of all products will rise.”

Side note: the odds are still 99% the Fed will not cut rates tomorrow.

💣 The Global Energy Protection Racket

The financial architecture around “defense” is expanding, as one would expect. It’s a natural feature of the landscape in the Empire of Debt.

In 1961, President Dwight Eisenhower alluded to how it works. In his farewell address, he warned about the military-industrial complex — a system where defense contractors, the Pentagon and Congress formed a durable loop around procurement and spending.

That loop includes financial capital. Here’s how it works.

Venture firms, private equity groups and Wall Street banks are allocating capital toward defense technologies, autonomous systems and next-generation weapons platforms. The Pentagon has introduced an investment-banking function, and bankers are actively seeking mandates tied to defense financing.

David Ulevitch of Andreessen Horowitz described the model in practical terms: private capital assumes early-stage risk in exchange for the possibility that a small number of investments generate outsized returns.

“Our loss ratio will be reasonably high,” Horowitz says. “We only need 20 winners.”

Funding from Wall Street blends seamlessly with taxpayer-backed procurement. The development risk of the new machines of warfare is shifted toward investors. Production contracts and deployment timelines tie those investments back into government spending. Only Wall Street gets to see the bulk of the upside.

The system expands through political ambition, budget allocations and capital markets. In that order.

🔋 Energy Sets the Constraint

Energy remains the binding constraint across the system.

War in the Middle East has placed pressure on infrastructure, shipping routes and supply chains. Price increases move through production, transportation and consumption simultaneously.

Louis-Vincent Gave described the mechanism in simple terms: “Energy is the dark force of our economic systems. Once it goes up a lot, everything else dies.”

Higher energy costs feed into inflation, influence interest-rate expectations and alter capital allocation decisions. Businesses prioritize supply security. Governments reassess strategic reserves and production capacity.

China enters this phase with a different structure. Its industrial system is built around long-term planning, domestic production and energy coordination. Western economies rely more heavily on global supply chains and imported inputs.

⚓ Chokepoints and Power

While we were in Panama, the comparison to Singapore came up repeatedly.

Both countries function as global logistics and financial hubs. Both represent military chokepoints of varying degrees. Both sit astride critical maritime routes. Both rely heavily on foreign capital and service-based economies.

The divergence appears in how each is built on those advantages.

Singapore pursued a long-term industrial policy. It moved from labor-intensive manufacturing in the 1960s to technology and innovation-driven industries over the following decades.

Electronics, precision engineering, chemicals and biomedical sectors anchored that transition. The government identified industries, attracted multinational partners and invested heavily in human capital.

Panama’s growth has centered on the canal, logistics and financial services. Services account for roughly 75% of GDP. The economy benefits from geography but shows less diversification and higher income inequality.

Singapore built around its chokepoint. Panama put tolls up at either end of the Canal.

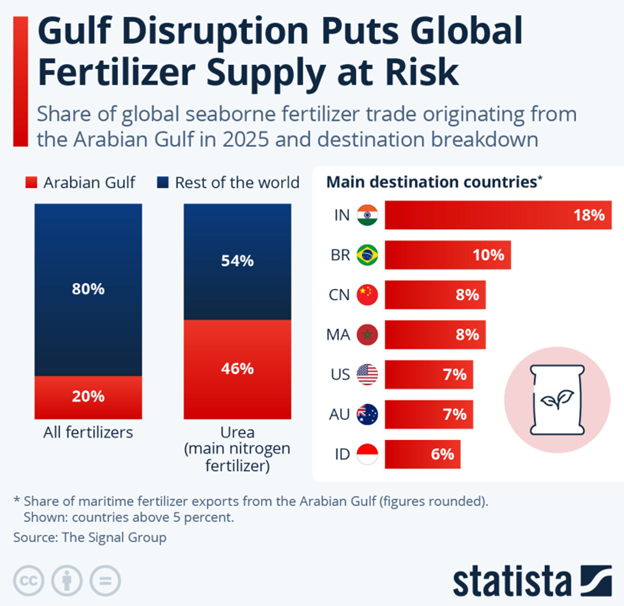

Farmers, globally, are at risk of higher diesel prices and a lack of fertilizer at a critical point in the growing season. (Source: Statista)

Farmers, globally, are at risk of higher diesel prices and a lack of fertilizer at a critical point in the growing season. (Source: Statista)

The Strait of Hormuz remains one of the most important chokepoints in the global economy. A significant portion of the world’s oil, LNG and to the farmers’ dismay, fertilizer moves through that narrow passage every day.

If the Strait gets choked up, prices for everything go up immediately.

Ray Dalio framed the pattern through historical precedent: control over key trade routes has marked transitions in global power, from the Dutch Republic’s shipping networks to Britain’s naval dominance.

Energy flow, military capacity and financial strength converge at these chokepoints. When one of those variables shifts, the others adjust. Not always in predictable ways.

First, the prices move. Then the money follows.

🍀 St. Patrick and the Edge of Empire

Today is a common day for corned beef and cabbage and Irish whiskey. And drunken debauchery for young folks the world over. Regardless of your heritage, you’re tempted to wear green, except, of course, if you’re English.

It wasn’t always that way.

St. Patrick was born in Roman Britain during the later years of the Roman Empire. His name was Magonus Saccatus Patricius. His family belonged to the Romanized elite.

At sixteen, he was abducted by Irish raiders and taken to herd animals in what is now Northern Ireland. He spent six years in captivity before escaping and returning to Britain.

Years later, after studying in Gaul, he returned to Ireland as a bishop. He preached in terms people understood, using the three-leaf shamrock to explain the Trinity. He established churches and monastic centers across the island.

Those monasteries preserved texts from Greece and Rome after imperial authority receded. Manuscripts were copied, stored and carried across regions beyond the reach of the empire that produced them.

The fable of him chasing the snakes out of Eire is largely thought to be a euphemism for the destruction of the mystical power Pagan Druids held over the tribes of the land. Of the two religions, the Druids were more likely to encourage drunken debauchery.

Or so we’ve come to believe.

If you’d like to learn more about St. Patrick, we recommend you read the historic details in St. Patrick: Patron Saint of Ireland…And a Roman Citizen! (Source: Classical Wisdom Daily)

“May your pockets be heavy and your heart be light.”

— Addison

P.S. This week in Grey Swan Live!, we’ll return to its regular time slot at 2 p.m. ET / 11 a.m. PST.

This Thursday, we’ll be joined by our natural-resources specialist, Shad Marquitz, for a look at volatility and opportunity in oil, energy, rare earths and precious metals following the Iran bombing excursion.