For most of our investing lives, risk seemed relatively easy to identify.

A retiree bought Treasury bonds because they were considered safe. A pension manager bought the S&P 500 Index because America was expected to grow. A balanced portfolio owned a 60-40 split of stocks and bonds, which generally moved in opposite directions during periods of stress.

A look across markets today reveals a more complex world: The Dow, S&P 500 and Nasdaq are all down 2% to 3%. Bitcoin is down 5%. Gold and silver are down 3% and 6%, respectively.

Here’s the thing. The prevailing wisdom… the “buy the dip” mandate… and 60-40 rule of thumb… those assumptions outlining risk in your portfolio were all shaped during one of the most unusual periods in modern history.

China entered the global trading system and became the world’s manufacturing center. The Soviet Union collapsed. Europe pursued deeper integration. Advances in computing and communications allowed corporations to coordinate production across continents with astonishing efficiency.

Goods became cheaper to manufacture, inflation drifted lower and interest rates followed. Capital moved easily across borders while supply chains stretched around the globe.

For nearly 40years, the forces of globalized trade in goods and services, labor, transport, tariffs and treaties all reinforced one another.

Investors who came of age during that period learned to view globalization, low inflation and steadily falling interest rates as “normal.” The world around us today would have looked far less familiar to investors in 1995.

A utility executive in Virginia spends his days fielding calls from technology companies searching for electrical capacity that does not exist.

Governments negotiate over semiconductor equipment, transmission infrastructure and rare-earth minerals with an intensity once reserved for oil fields and shipping routes.

Data center developers increasingly discover that access to power determines where projects get built and whether they get built at all.

To the point we’ve been belaboring here in the Dive: The digital AI economy has made physical infrastructure important again. There is no turning back. The Rubicon has been crossed.

🌎 The Treasury Market Is Asking Different Questions

One of the more interesting observations we found corroborating our Great Race these came through research highlighted by Shanaka Anslem Parera on his Substack page.

For generations, foreign governments have accumulated dollars through trade and invested them in Treasury securities. Countries that needed access to global commerce needed dollars. Countries holding dollars needed somewhere to store them. Treasury bonds became the natural destination.

That relationship helped finance decades of American borrowing.

Today, global demand for dollars remains strong. International trade continues to run through dollars. Dollar funding remains essential to the global financial system.

Investors love debating de-dollarization in theory. In practice, the world continues to hold dollars, borrow dollars and transact in dollars at a scale no rival currency can match. (Source: Bloomberg)

Yet investors increasingly require greater compensation to lend money to Washington for thirty years.

The Federal Reserve spent much of 2024 and 2025 lowering short-term rates. During the globalization era, long-term Treasury yields would normally have followed lower.

Instead, 30-year yields climbed above 5% as lenders demanded additional compensation for financing deficits stretching decades into the future.

Foreign reserve managers diversify holdings more actively than they once did. China continues to develop payment systems outside traditional dollar channels. Governments increasingly hold strategic reserves in a wider range of assets than they did a generation ago.

Those decisions eventually work their way into mortgage rates, commercial lending costs and business investment decisions throughout the economy.

A family purchasing a home in Phoenix may never think about reserve-management decisions taking place in Beijing or Riyadh. But their mortgage lender sure will.

🧭 Lyn Alden’s Wild West

Lyn Alden also chimed in. Lyn’s the resident economist with George Gammon’s outfit. She’s spent years documenting how unusual the post-Cold War environment really is.

The decades following the collapse of the Soviet Union created conditions that investors eventually came to mistake for permanent features of the landscape. Global trade expanded. Manufacturing moved toward lower-cost regions. Financial capital flowed freely. Supply chains lengthened. Central banks spent much of the period fighting disinflation rather than inflation.

That world rewarded a specific style of investing: Growth stocks flourished. Long-duration assets flourished. Financial engineering flourished. Borrowing money became steadily cheaper.

The Great Race foists a different set of incentives. Individual investors like you need to pay attention right now.

Countries now compete for semiconductor production, electrical generation, strategic minerals and industrial capacity because economic strength increasingly depends upon controlling the infrastructure supporting advanced technologies. Supply chains designed solely around efficiency are increasingly giving way to those designed around reliability, resilience and national interest.

The regime change is visible whenever governments subsidize domestic chip fabrication, negotiate access to critical resources or intervene directly in industries they once left to markets.

Investors accustomed to globalization’s tailwinds increasingly find themselves navigating a world where politics, industry and national security intersect in ways they have not for decades.

🧠 Mythos And The National Security Economy

Artificial intelligence offers perhaps the clearest example of that transition.

For years, Silicon Valley and Washington occupied separate spheres. Technology companies built products. Government agencies regulated them.

The reported use of Anthropic’s Mythos model inside intelligence operations reveals how rapidly that distinction has disappeared.

Software capable of identifying cyber vulnerabilities, analyzing massive quantities of information and automating complex decision-making processes carries obvious commercial value. The same capabilities carry equal value for intelligence agencies, military planners and national security officials.

The conversations surrounding frontier AI increasingly resemble discussions once reserved for aerospace systems, cryptography or satellite networks.

Questions about computing infrastructure quickly become questions about energy supplies. Questions about model access become questions about national security. Questions about investment become questions about strategic advantage.

Technology firms now negotiate not only with customers and shareholders but also with governments seeking influence over systems considered vital to future economic and military competitiveness.

The boundaries separating technology policy, industrial policy and national security policy continue to fade.

🏛️ When The House Joins The Game

During the era of globalization, investors generally treated governments as referees.

Governments established rules, adjusted tax rates, regulated industries and intervened occasionally during crises.

The Great Race we’ve already entered has changed that relationship entirely.

Tariffs influence industrial investment decisions. Export controls shape technology markets. Energy policy influences where data centers are constructed. Government subsidies determine the location of semiconductor fabrication plants. Defense priorities affect research spending, manufacturing capacity and supply-chain development.

Companies operating inside strategic industries increasingly build plans around government decisions.

Investors evaluating those companies increasingly evaluate government execution alongside corporate execution.

A utility company seeking approval for transmission expansion, a chip manufacturer planning a fabrication facility and an AI company searching for power capacity all encounter the same reality.

The state now sits at the table where many of the most important economic decisions are made.

⚖️A World In Debt, Already

And it’s entirely fueled by debt. Public debt. Which the bond vigilantes are currently pricing much higher than during the 40-year era of aggressive globalization.

Grey Swan contributor Mark Jeftovic made this observation on Grey Swan Live! yesterday:

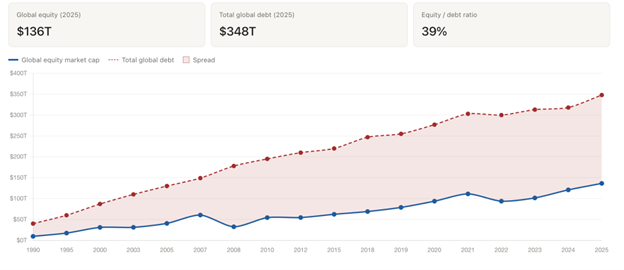

Most people who follow markets already know that global debt is bigger than global equity. The number gets quoted often enough that it has lost its meaning. As of 2025, total global debt sits at roughly $348 trillion. Global equity market capitalization sits at roughly $136 trillion. Debt is more than two and a half times the size of equity, and the ratio has been getting worse for decades.

The spread between global debt and asset valuations narrows slightly during boom years. But somehow the public debt never really gets addressed. And then, the next crisis begets public support for piling even more debt on the pile. And so on, ad infinitum. (Source: The Sovereign Capitalist)

The spread between global debt and asset valuations narrows slightly during boom years. But somehow the public debt never really gets addressed. And then, the next crisis begets public support for piling even more debt on the pile. And so on, ad infinitum. (Source: The Sovereign Capitalist)

“Now look at the crisis years,” Mark suggests.

“In 2007, the spread was about $89 trillion. By 2010, it was $141 trillion. Equity got cut nearly in half between 2007 and 2008. Debt accelerated because debt was the policy response.

“Bank bailouts, sovereign deficits, central bank balance sheets, QE. All of it lands on the debt side of the ledger. None of it puts equity back where it was.

“Same story in 2020. Equity briefly cratered. Debt jumped by more than $30 trillion in a single year, the largest absolute increase ever recorded. By the time the dust settled, the spread had blown out by another $80 trillion.”

💰 Following The Money

And now we face an inauguration of state-owned capitalism, Western-style.

“Senior U.S. officials have held preliminary discussions with major artificial intelligence companies about the potential for the federal government to acquire some shares in their firms,” reports the tech letter Notus.

“Sam Altman, the CEO of OpenAI, has discussed the idea with senior Trump administration officials periodically since the president began his second term.

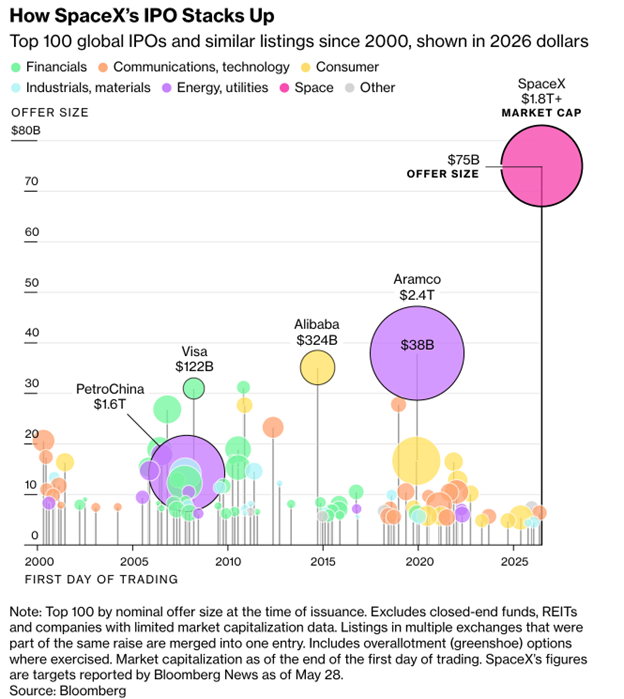

There’s a lot of hand-wringing and breathless anticipation over prospective IPOs for Anthropic and OpenAI. Neither holds a candle, yet, to the fervor over next week’s historic valuation of the SpaceX IPO. Adding the government as a shareholder makes things even messier and fraught with risk for individual investors. (Source: Bloomberg)

“Altman first pitched the concept directly to President Donald Trump in a conversation in early 2025, and has discussed it again with senior administration officials in recent weeks as a way to more broadly distribute the economic benefits of AI to the public.”

“The problem is that the government would be a shareholder and a regulator at the same time, which creates substantial conflicts of interest,” tech skeptic Nat Purser told Notus. “Many conservatives who oppose government interventions in the economy were critical of Trump’s deal with Intel, and would probably have even bigger gripes if OpenAI or Anthropic and the president came to an agreement.”

💵 From Whence Real Economy ROI?

Among the safety concerns, you can also add investor fears that all the buildout spending in AI is great for Wall Street banks and fast-cash brokerage firms, but lacks a defined ROI that makes sound investment sense.

During New York Tech Week, IBM Vice Chairman Gary Cohn questioned whether industry spending on artificial intelligence may be running ahead of measurable returns.

Similar concerns accompanied railroads, electrification and the early internet.

Investors funded infrastructure long before they could accurately calculate the returns because the infrastructure had to exist before the returns could emerge.

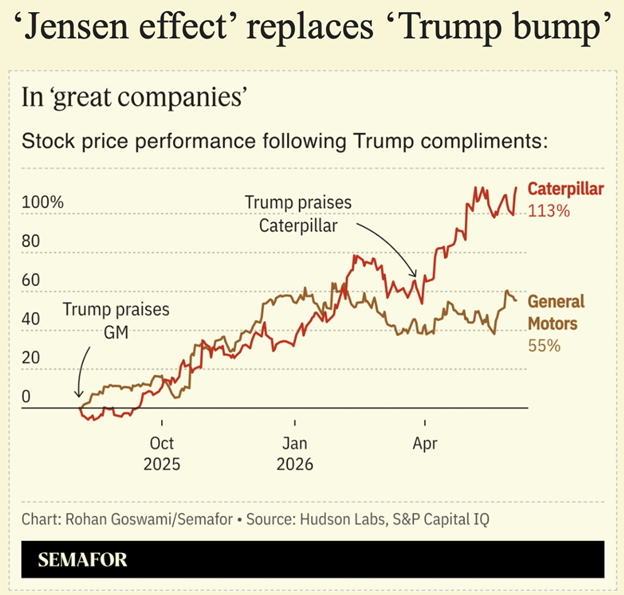

A reading of the influence of Trump on prospective government acquisitions of publicly traded securities. Jensen Huang has increasingly had a similar effect talking up companies in Nvidia’s customer base. Trump’s economic strategy is increasingly designed to benefit directly from the influence the two men have on the stock market, both publicly and in their own portfolios. (Source for the chart: Semafor)

A reading of the influence of Trump on prospective government acquisitions of publicly traded securities. Jensen Huang has increasingly had a similar effect talking up companies in Nvidia’s customer base. Trump’s economic strategy is increasingly designed to benefit directly from the influence the two men have on the stock market, both publicly and in their own portfolios. (Source for the chart: Semafor)

Jensen Huang’s influence increasingly reflects his position near the center of that system. Every major AI project ultimately traces back through chips, fabrication capacity, energy supplies and financing.

The supply chain stretches from power plants to pension funds. If there’s no ROI on the AI buildout… the entire financial system is at risk. Again.

🪖 D-Day And Destructive Industrial Power

Tomorrow marks the eighty-second anniversary of D-Day.

When Allied forces crossed the English Channel on June 6, 1944, they carried with them the output of factories, shipyards, railroads, oil fields and financial institutions that had spent years preparing for that moment. The invasion itself lasted hours. The industrial mobilization supporting it took years.

The ships approaching Normandy represented steel production, energy production, manufacturing capacity, logistics networks and financial resources assembled across an entire continent.

All wars have their root cause in economic disadvantage and in the failure of politics to reach civilized agreements. Military power has advanced in step with technological and industrial capacity.

The technologies change. The machines of death get more complex and efficient. The underlying relationships do not. Adding the government to the list of owners… on the public’s debt… just seems like a bad idea.

And yet, the Great Race dictates that the countries that generate abundant energy, build advanced infrastructure, finance large-scale projects and translate innovation into productive capacity tend to shape the world that follows.

~ Addison

P.S. Eighty-two years ago, the factories, power plants and transportation networks supporting the Allied war effort determined the outcome of a global conflict long before soldiers reached the beaches of Normandy.

Today, the competition revolves around semiconductors, electrical grids, artificial intelligence and industrial capacity, but the deeper question remains remarkably familiar: who can build, finance and power the future first?

Yesterday on Grey Swan Live!, Mark Jeftovic joined us to cover the latest developments in the crypto space – including the Clarity Act and the Fate of Dollar 2.0.

Crypto has taken a back seat to the AI trade in recent weeks, but those lamenting crypto’s poor performance may not have much longer to wait, with so many positive catalysts on the horizon.

Mark’s conversation revealed when this crypto bear market is likely to end, the potential positive catalysts from the Clarity Act, and how to set up your business so you can get paid in crypto during this bear market.

The replay is up on the site for our members who weren’t able to join live.