Oil backed away from its flirtation with $120 a barrel quicker than a politician backs away from a campaign promise yesterday.

But the number was just round enough to encourage a whole round of headlines in the news cycle.

By the close, traders had decided — for a few hours at least — that the worst might not compound immediately. By mid-day today, WTI was back in the $79 range. Still, energy prices remain roughly 25% above where they stood before the U.S.–Israel strikes on Iran began.

The S&P 500 hasn’t recovered the 2% it dropped last week. Curiously, volatility remains high even though the major indexes are all but flat. The VIX jumped to 31 yesterday.

February job losses continued to fan oil price fears, reaching well beyond DOGE’s government trims and into private payrolls.

That is where we stood this morning: oil off the peak, employment making traders nervous, inflation ticking back up, and boardrooms adjusting quickly behind the scenes.

🛢️ Energy Shock Moves Through Balance Sheets

Saudi Aramco’s CEO warned of “catastrophic consequences” if the Strait of Hormuz remains blocked. As you have no doubt heard ad nauseam this past week, “one-fifth of the world’s oil passes through that channel.”

Amena Bakr reports at Semafor that Iraq’s output has fallen from roughly 4.2 million barrels per day to about 1.7 million. Abu Dhabi, Kuwait, and Iraq have slowed production as tankers wait in the Gulf. Some producers possess alternative routes. Others depend entirely on Hormuz.

Geography is reasserting its leverage.

“The U.S. is a $30 trillion economy that has proven hard to knock off its course and investors are still holding on to a lot of that optimism,” writes Liz Hoffman at Semafor, “Just look at how rapidly the markets turned positive yesterday on the suggestion that oil worries may subside. But it’s a CEO’s job to boost the company’s bottom line. And while they may use euphemisms like ‘uncertain macroeconomic outlook,’ ‘financial discipline,’ or ‘right-sizing for current conditions,’ layoffs will follow not because the economic conditions demand it — but because the economic fears allow it.”

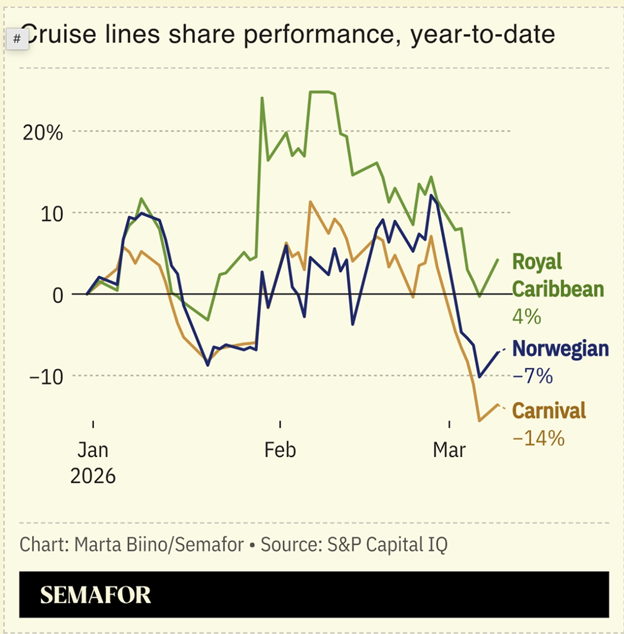

Hoffman points to the Cruise Line business to illustrate how price disruptions ripple through the economy.

Fuel hedging separates competitive companies in calmer times. In volatile weeks, it separates earnings, including Carnival, a heretofore strong performer in the Grey Swan model portfolio. (Source: SEMAFOR)

Royal Caribbean hedged roughly 60% of its fuel exposure near $75 oil. Norwegian hedged about half at slightly higher levels. Carnival did not hedge.

At $100 oil, Carnival faces fuel costs 10–20% above its peers.

Airlines largely stopped hedging after losses in the early 2010s. Those decisions looked prudent when oil stayed stable. They look different now.

Arithmetic is rarely dramatic. It is decisive.

💼 AI Cover and Corporate Payrolls

AI exuberance in the stock market has given executives room, rather… an acceptable excuse to act.

During the pandemic, companies hired aggressively and hesitated to reverse course publicly. Now, earnings calls reference “discipline” and “efficiency.”

Energy volatility and geopolitical risk create cover. Layoffs follow because boards reward margin defense during uncertainty.

February’s job losses extended into the private sector. Retail investors are withdrawing funds from retirement accounts such as 401(k)s, as laid-off workers feel pressure to adjust spending quickly.

Households respond before economists model the shift.

Inflation remains and will remain stubborn. Especially with the M2 and government deficits swelling to meet the demands of the Iran conflict.

The Federal Reserve meets next week under open pressure from the White House to cut rates. There’s still time for the Fed to act… but odds at Polymarket still say they will leave rates unchanged.

📉 Treasury and the Futures Temptation

Monetary policy influences liquidity. It does not refill strategic petroleum reserves.

Bloomberg and Reuters both report that Treasury officials are evaluating oil futures trades — buying longer-dated contracts while selling shorter ones — to influence gasoline prices.

The approach resembles 2012’s Operation Twist in the interest-rate market.

Amos Hochstein, former U.S. energy envoy, told Semafor: “You can’t financial-paper-exercise your way out of it.” Joe Brusuelas at RSM warned that such trades could invite “the mother of all short squeezes.”

Maybe the Treasury would be better off leaving the futures markets to speculators.

The oil futures market trades in the trillions. It does not yield easily to intervention or political pressure.

“The Fed can print reserves, the Treasury can print money, but neither can print oil,” Brusuelas said.

Releasing barrels from the Strategic Petroleum Reserve or suspending the federal gas tax are established tools. Leveraged futures positions introduce counterparties that most average Americans filling up their gas tanks will not understand.

With oil trading in an elevated, but still reasonable range, the pressure to release oil reserves has waned. Probably a good thing since the Trump administration has been striving to replenish the empty reserves it inherited.

🌏 China’s Long Preparation

Unlike the U.S., Jason Bordoff of Columbia University notes that China has prepared for supply volatility for years. The country holds more than two months of oil in onshore storage. Sanctioned barrels from Russia, Iran, and Venezuela sit offshore in tankers. Domestic production exceeds that of several regional peers.

China leads in EV deployment and renewable installation. Its economy consumes less oil per unit of GDP than the United States. Installed renewable capacity does not reprice daily once built. Fossil fuels do.

China learned from Europe, following the Russian invasion of Ukraine, 2020-present, that dependency carries costs. China’s strategy reduces some exposure. It does not eliminate risk.

Supply chain dependency is a significant driver of the Trump reset and realignment strategy, which employs tariffs and incentives to reshore manufacturing. Will the strategy pan out in time to prevent “affordability” issues from flipping the purse strings in the House in November? That’s the political question of our time…

🇨🇳 Beijing Logistics and Corporate Delegations

Three weeks before President Trump’s trip to Beijing, corporate participation remains unsettled. Executives in aviation, autos, technology, and finance report no formal invitations yet.

Hmn…

When UK Prime Minister Keir Starmer and German Chancellor Friedrich Merz visited Beijing earlier this year, they brought roughly 90 executives combined.

We’re left to assume the actual plans still depend on the President’s assessment of the progress in the war being waged on Iran and the mess it has created in the Gulf.

✈️ Buffett Steps Back, Ackman Steps Forward

Warren Buffett left his post at Berkshire Hathaway to the presumably capable hands of Greg Abel in January.

Now, Bill Ackman wants to take a shot at replacing Berkshire Hathaway at the top fund spot for retail investors on Wall Street.

Ackman has filed to take Pershing Square public. Again.

Pershing’s management company reported roughly $250 million in profit last year on $763 million in revenue. Investors in the proposed vehicle would receive exposure not only to portfolio holdings but also to fee income.

Ackman once turned $200 million into $4 billion through macro trades during Covid and inflation spikes. His 2024 listing attempt found little appetite. This filing adds participation in the management entity itself.

Markets crudely evaluate cash flow durability in volatile periods like the one we’re about to enter. The timing of Ackman’s filing will matter. We’re interested… more to come.

🌴 Panama, the Canal, and the Dollar Question

A Grey Swan member wrote from Panama City after attending a Living and Investing event in January.

Phalen F. noted the subway — $40 by taxi from the airport, $1.50 by train in the opposite direction. He asked some good questions: about expansion timelines and road development toward Boquete… and how energy disruption affects canal revenue. He questioned Panama’s use of the U.S. dollar amid currency erosion and global conflict.

The canal’s revenue depends on trade volume and routing decisions. Those decisions are all in flux given events halfway around the world.

Energy shocks certainly alter tanker flows. Container traffic, also impeded by tariff uncertainty, follows broader demand.

Dollarization removes currency volatility locally while importing U.S. monetary policy wholesale. Stability has a cost and a benefit, especially given the government’s penchant for spending money out of thin air and fighting wars in the Middle East.

These are all good questions that straddle lifestyle considerations and the Canal position as a global chokepoint for trade and energy supply.

On the slate: We’ll be reviewing infrastructure plans, canal sensitivity, and jurisdictional considerations on site this week in Panama City with Ronan McMahon and Alfredo Alemán.

Geography, as we mentioned above, regains importance when chokepoints get choked.

— Addison

P.S. This week, Grey Swan Live! will be recorded from Panama City during The Gathering with Ronan McMahon’s team.

An aerial render of a recent RETA deal in Cap Cana. Some of RETA’s top deals occur in exquisite beachfront areas in Panama and Mexico.

We will review the Ipanema and Beachwalk briefings in context — infrastructure, canal exposure, jurisdiction, and long-term capital allocation. The canal still moves ships. Capital decides where it anchors.