President Donald Trump’s Federal Reserve chairman appointee, Kevin Warsh, wants a new deal between the Treasury and the Fed.

He calls it a “Modern Treasury-Fed Accord” — a structural reset modeled on 1951, when the Fed stepped out from under the Treasury’s wartime rate caps and reclaimed the right to let interest rates float.

Warsh’s version aims at a different excess.

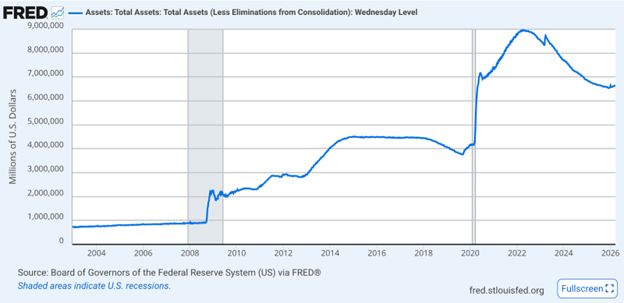

In response to the biggest economic own goal in modern history (the Pandemic Lockdowns), the Federal Reserve went into crisis-free-money-orgy mode. Warsh’s modern accord would roll back the Fed’s role in bailing out banks and financial firms who have misallocated capital spending. (Source: Federal Reserve.)

The Fed’s balance sheet sits near $6.6 trillion, down from the Biden-era social justice free money orgy of $9 trillion.

Warsh argues an activist Fed distorts markets, subsidizes fiscal decisions made for social justice or climate initiatives and muddies the line between monetary policy and sound budget management in Congress.

In plain English: he wants the central bank smaller, simpler and able to lower rates.

Whether that restores independence or rearranges it is the fight now underway in Washington, D.C. and in the bond market.

🏛️ 1951, Revisited

The 1951 Accord ended the Fed’s obligation to keep borrowing costs down after World War II.

Treasury debt had ballooned. Rates were pinned low to keep financing manageable. The central bank regained discretion only after a bruising standoff.

Warsh sees echoes.

Debt is high again. The Fed bought trillions in Treasurys and mortgage-backed securities after 2008 and again in 2020.

Quantitative easing became routine. It was being used as both a carrot and a stick on Wall Street and in the real economy.

Warsh argues the central bank crossed into “fiscal-like” territory by absorbing the risk duration of bonds and intentionally compressed yields to “help” finance government debt.

Warsh’s Modern Treasury-Fed Accord proposal: shrink the balance sheet materially. Sell longer-dated bonds and mortgage paper. Hold mostly short-term Treasury bills. He would replace “forward guidance theater” with rule-based communication focused only on communicating the Fed’s role in managing the nation’s currency… and by extension the reserve currency of central banks across the Western financial system

No mysticism. Fewer improvisations. A smaller footprint.

When all is said and done, no Fed thumb on the scale of a free market capital.

If it sounds tidy, one only needs to remember: markets are not tidy.

📉 Billification and the $39 Trillion Question

Shifting the Fed’s balance sheet from long bonds to T-bills will have a direct impact on the bond market.

Long-term bonds set mortgage rates, corporate borrowing costs and the discount rate for equities.

T-bills anchor liquidity and collateral markets.

When the Fed owns fewer long bonds, private investors must absorb more of the risk and will demand compensation for it. Yields would then find their own level in the market. Rather than Fed policy determining what they should be.

When the Fed concentrates its buying on T-bills, the Treasury can lean more heavily on short-term issuance. Bills are cheaper when short rates are lower. The temptation is obvious.

Warsh’s critique of the Powell Fed boils down to this: If Treasury and the Fed “coordinate” balance sheet size and issuance strategy, the lines blur. Monetary tightening becomes a shared decision. Shared decisions dilute accountability.

An independent Fed would be free of the Treasury’s burden to fund spending… which is determined by a broken Congressional system.

This is all theoretical, of course.

Even now, bond traders do not wait for press conferences. They’re already pricing supply, duration and rollover risk on the fly.

Critics say a steeper yield curve will likely occur if short rates fall while long rates drift higher, driven by private investors’ demand for higher yields to fund the government.

If that ends up being the case, so be it.

💻 The AI Bet

Warsh’s most controversial idea sits inside the rate framework he’d propose were he in the Chairman’s seat.

His argument harkens back to the Greenspan Fed in the late 1990s during the first wave of the information revolution.

The argument claims that AI raises productivity in ways backward-looking models fail to capture. If output per worker climbs, the economy’s speed limit rises. Rates can stay lower without igniting inflation.

For reference, Warsh invokes the 1990s method — anecdotal evidence from business leaders, esoteric data, investment cycles — rather than waiting for lagging, often suspect, government data releases.

The data sets he’d rely on include real-time corporate capex on data centers. Automation trends. AI deployment curves. All of which would be leading indicators. The focus would be on encouraging technological innovation in the real economy rather than having the central bank play handmaiden to politics and bloated government spending initiatives…

Critics within the Fed counter that borrowing to finance AI infrastructure pushes up capital demand and rates. They warn against overestimating productivity before it shows up in national accounts.

The “P-word” — productivity — has broken forecasts before, including during the dot-com boom and crash on Wall Street in 2000 to 2001.

For investors, the question is not theoretical. You can measure it and decide whether it’s working for your bottom line or not.

Manufacturing and agriculture are projected to drive the majority of value creation, with manufacturing expected to see $235–$259 billion in value added in India alone by 2035. (Source: Penn Wharton)

If the Fed embraces AI-driven disinflation, short rates may fall sooner and faster than traditional models suggest. If that productivity fails to materialize, policy could and likely will whipsaw withe political response to natural market forces.

“So be it,” a Chairman Warsh would say. Place your bet and get on with it.

Technology infrastructure, semiconductors, cloud operators and energy suppliers sit at the center of that bet, which is why Warsh’s “radical” plan jives hand in glove with the Trump grand realignment strategy.

Enter Scott Bessent.

🏦 Bessent’s Hand on the Wheel

Treasury Secretary Scott Bessent aligns with Warsh philosophically and has said so explicitly. Bessent described the Fed’s expansion under Jerome Powell and his predecessor as a “gain-of-function” mutation.

The Fed, increasingly since the 2008 financial crisis, has become “activist” in its mandate; an active participant in the economy and in financing the political aims, most notably those of the Biden-era agenda.

Already, Bessent has urged patience. Balance sheet shrinkage cannot be rushed, he warns.

When pressed, Bessent has suggested it may take a year before any firm direction emerges. But with Warsh at the helm, the final decisions would remain “in the hands of the Fed,” asserting Fed independence from the get-go.

The partnership resembles two therapists agreeing that you have to stop the patient from injecting heroin, but debate methadone regimen to follow.

Kick the habit too fast and the patient dies. Too slow, the addiction lingers and a relapse is likely.

⚖️ The Powell Probe

Meanwhile, the Warsh confirmation path has stalled in Washington’s tangled underbrush. A thicket of motives and incentives only the sludge critters who dwell underneath understand.

Federal prosecutors in Washington, D.C., are investigating whether Powell misled Congress regarding cost overruns on the Federal Reserve’s headquarters renovation.

The sordid details of the story one could only find in the political thickets on the banks of the Potomac:

- The Allegations: The DOJ is examining whether Powell’s June 2025 testimony falsely denied that “lavish perks”— such as private elevators and elite dining rooms — were included in the project, which is currently estimated to be $700 million over budget. The total renovation of the Eccles Building – Fed’s HQ palace – exceeds $4 billion.

Not exactly the hallmark of a smaller, less obtrusive bank.

- Powell’s Defense: He has characterized the probe as a “pretext” and “retaliation” for his refusal to cut interest rates as aggressively as the White House demanded.

- Judicial Ruling: On March 13, 2026, Chief U.S. District Judge James Boasberg quashed the DOJ’s subpoenas, stating the government had offered “no evidence whatsoever” of a crime beyond “displeasing the president.”

Despite the ruling, U.S. Attorney Pirro, former co-host of Fox News’ The Five has pledged to appeal.

Powell’s term as chair ends May 15. He has signaled that he will remain as chair pro tem if confirmation drags out.

The central bank’s leadership transition sits in procedural limbo while the bond market continues to trade every morning at 8:20 a.m.

🎭 Warren’s Letter

On the other side of the aisle, Sen. Elizabeth Warren, stretching the absurd as far as even her imagination can go, has opened an inquiry into Warsh’s past social ties to Jeffrey Epstein.

Emails released by the Justice Department suggest invitations to events in 2010. Warren requests clarity on attendance and communications. No wrongdoing has been alleged, of course.

The letter adds needless friction to an already delayed schedule. Even scheduling the hearings wastes time and taxpayer money. And it has nothing to do with the Fed’s role in the banking system or mortgage rate reform.

In the markets, the delay adds anxiety and uncertainty to investors’ already long list of reasons not to act… as if the Iran conflict wasn’t already enough.

📈 What Will Move The Needle

This week, the debate alone unsettled bonds.

Abetted by concerns over the war in Iran, the yield on the 10-year lept up to 4.4% as bond buyers demanded a higher return for lending their money to the government. (Source: Trading Economics)

“Warsh shock” became trading-desk shorthand for a shift toward rule-based discipline and balance-sheet contraction. It’s a shock because if Warsh gets his way, the Fed will return to being a “lender of last resort” rather than the bailout vendor of first resort. No more free goodies for you.

Gold and silver investors suffered the largest one-day drops in history (9% and 30%, respectively). The dollar index rose alongside the oil shock from the Iran war.

In short, markets respond in real time to anticipated liquidity conditions, just as crops respond to weather forecasts. Any delay in confirmation only further seizes liquidity.

🧭 The Structural Question

The 1951 Accord clarified authority after a war-financed debt surge. Warsh proposes a new accord amid the pandemic-era government spending binge, another era of crisis-elevated debt.

The difference today lies in scale and speed. Treasury issuance rolls daily. Global capital reallocates to new events in milliseconds. Artificial intelligence compresses decision cycles. Social media amplifies rhetoric.

Warsh wants to take all this into account to determine how the Fed can best facilitate a booming economy. Rather than waiting to see if the data reflects a set of policy decisions with predetermined outcomes.

A rule-based Fed with a smaller balance sheet would restore clarity for investors, business owners and mortgage holders. It would restore economic decision-making to those who make them, rather than to policies set by social engineers in Washington, D.C.

To make good decisions on their own, investors do not need prophecy or moral guidance. They just need the markets and banks to work and the government to get out of the way.

The Federal Reserve holds trillions in assets. Trillions more than they need to.

In 1951, the argument concerned capping rates. This year, it concerns how much of the balance sheet should exist at all.

The old Accord ended fiscal dominance needed to fight the most destructive war in human history. The new modern accoard one is an attempt to prevent its return.

Markets will test the theory long before historians name it. That is, if Tillis and Warren would just stop talking for a minute…

~ Addison

P.S. In yesterday’s Grey Swan Live!, I connected with Shad Marquitz to examine volatility and opportunity across oil, energy, rare earths, and precious metals following the Iran bombing excursion.

We’re in the middle of an active shooting war in the Persian Gulf … Oil has surged … Year to date, gold and silver have each tacked on roughly 20% … Gasoline and diesel prices are spiking…

And yet, the stock market is barely reacting. So, we unpacked what’s going on and the opportunities for investors today.