Here’s a first. We never thought we’d spend a Friday midday watching the swearing in of a Federal Reserve chairman like it was the launch scene from a political thriller.

Yet there we sat watching Kevin Warsh take the oath, standing next to his wife Jane, beneath the chandeliers in the East Room of the White House.

Supreme Court Justice Clarence Thomas swore him in as traders around the world watched Treasury yields, oil prices and the possibility that the most important financial regime change in 40 years had just become official.

Kevin Warsh is pushing an agenda centered on modernizing the Federal Reserve, improving real-time economic data, and restoring credibility to monetary policy after years of inflation volatility. (Source: Fox Business)

Historically, Wall Street tends to get nervous when a new Fed chair arrives. A quick search through the financial press yesterday morning suggested the consensus expected markets to wobble once Warsh officially took control of the central bank.

Instead, the exact opposite happened.

While President Donald Trump spoke and Warsh delivered his remarks, the S&P 500 Index, the Dow and the Nasdaq all drifted toward fresh new historic highs. Gold barely moved. Silver sold off briefly before trading sideways. Bitcoin, apparently, had better things to do.

A few hours in, and the market is unafraid.

At least for now.

The calm matters because Warsh is inheriting a Federal Reserve trapped between two very different worlds.

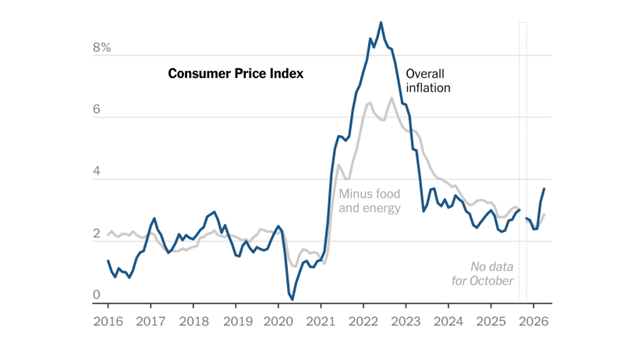

A year ago, markets still expected the Fed to continue cutting rates as inflation cooled. Now inflation is rising again under pressure from the Iran war and tariffs, while the bond market increasingly debates whether rates may eventually need to move higher instead.

Warsh now sits at the center of the enormous challenge:

How do you restore confidence in the dollar system without detonating the financial bubble that cheap money created in the first place?

🎩 Warsh Thinks the Fed Lost Its Way

Kevin Warsh has spent two decades giving speeches, writing essays and sitting for interviews about what he believes the Federal Reserve should actually do. Unlike many central bankers who speak in language so dry it could dehydrate a cactus, Warsh tends to speak like a man who believes the institution wandered off course years ago and never fully found its way back.

His argument has remained remarkably consistent.

Warsh believes the Federal Reserve damaged its own credibility by relying too heavily on backward-looking inflation models, gigantic balance-sheet expansion and endless public commentary about future rate decisions. He rejects the old Phillips Curve framework that treats strong employment and rising wages as the primary engine of inflation. In Warsh’s view, inflation comes more directly from excessive government spending and central-bank intervention than from workers earning larger paychecks.

He also believes the Fed measures inflation poorly. Warsh has criticized the central bank’s preferred inflation gauges as rough approximations treated with false precision, and he has proposed building a real-time inflation tracker using millions of live prices moving through the economy.

From groceries to housing to energy, inflation continues to weigh on consumers and remains one of the most closely watched risks in the economy. (Source: New York Times)

The “2% target” belies the mockery that econometrics truly is, in our opinion.

That may sound wonky until you realize how weight Bernanke, Yellen then Powell put on the data the Fed has used to “understand” inflation correctly.

If Warsh is right, the central bank spent years treating the symptoms while missing the disease. Warsh, channeling Hayek, has said there’s no amount of data in the world that could make setting a precise target like 2% achievable or even desirable.

Money is not a science. The market can determine its most effective price far better than a bureaucrat.

🔥 The Iran War Changed the Equation

A year ago, Warsh could argue both that the Federal Reserve needed to restore credibility and that conditions for lower rates were approaching. The energy shock tied to the Iran war pulled those two ideas apart.

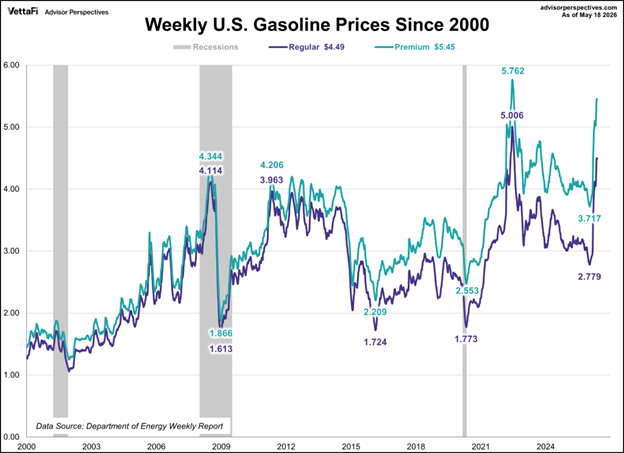

Gasoline prices are climbing again. Energy markets are tightening. Tariffs continue to push up costs across supply chains and manufacturing. Suddenly, the conventional wisdom shifted from “When will the Fed cut again?” to “Will the Fed eventually need to raise rates instead?”

Gas prices are rising again across the country, adding fresh pressure to consumers already dealing with stubborn inflation and higher everyday costs. (Source: Department of Energy)

That is a very different world from the one investors grew used to after each of the last seven financial crises dating back to 1987.

Warsh prefers to frame inflation as a form of monetary deterrence theory.

At a State Street conference last summer, according to remarks reviewed by The Wall Street Journal, Warsh argued that if the public believes the Fed will keep inflation low and stable, energy shocks and tariffs remain temporary price increases rather than becoming embedded throughout the economy.

“Eisenhower knew as a warrior, we can avoid wars if we’re prepared for one,” Warsh said. “The same thing is true with inflation.”

In other words, credibility itself becomes monetary policy.

The problem is that credibility becomes much harder to maintain once inflation starts rising, while wars, tariffs and industrial competition all demand enormous amounts of spending at the same time.

📈 The Bond Market Is Testing the New Fed Already

The bond market wasted no time testing the new regime.

Between September 2024 and December 2025, the Federal Reserve cut short-term interest rates six times. Under the old rules of globalization and structural disinflation, long-term borrowing costs should have been lower.

Instead, long-term Treasury yields climbed anyway.

That tells you lenders increasingly fear inflation and government borrowing more than they trust the Fed to control them easily.

Warsh now faces a balancing act difficult enough to make a circus acrobat sweat through his tuxedo. If he cuts rates too aggressively, markets may conclude the Fed no longer takes inflation seriously, which could drive long-term yields even higher. Mortgage rates could rise instead of fall. Commodity prices could surge further. The dollar itself could weaken.

At the same time, Warsh spent years criticizing the Federal Reserve for expanding its balance sheet into a $6.7 trillion mountain of assets that distorted financial markets and quietly subsidized government borrowing. He wants the Fed’s footprint smaller, quieter and less entangled in politics.

That creates tension inside the system immediately because shrinking the balance sheet generally pushes long-term interest rates higher, even while lower short-term rates attempt to stimulate borrowing.

Trying to lower rates while shrinking the Fed’s footprint at the same time may feel like trying to cool a campfire while somebody else keeps throwing logs onto it.

💵 Dollar 2.0 Is Scott Bessent’s Side of the Equation

This is where Scott Bessent enters the picture.

Among all the dignitaries standing inside the East Room after the ceremony, President Trump walked directly toward Bessent first. The gesture looked deliberate because it probably was.

Warsh and Bessent increasingly resemble the two halves of the same strategy.

Warsh appears focused on restoring credibility to long-term Treasury markets through tighter monetary discipline, less Federal Reserve activism and a smaller balance sheet. Bessent appears focused on preserving global demand for dollar assets through digital-dollar infrastructure and stablecoin systems we’ve started calling Dollar 2.0.

Most people still hear “stablecoins” and picture crypto speculators drinking tequila beneath neon lights in Miami. But underneath the jargon sits a much more serious Treasury strategy. Dollar-backed stablecoins generally hold Treasury bills and short-term government debt as reserves. If those systems become embedded in global trade and cross-border payments, they create a fresh source of demand for U.S. debt just as the old globalization system becomes less stable.

That matters because the old financial order depended heavily on foreign governments recycling trade surpluses into Treasury bonds almost automatically.

As we outlined yesterday, The Great Race is changing that system.

Countries increasingly compete for energy, semiconductors, industrial capacity and strategic resources while simultaneously searching for alternatives to the old post-Cold War financial architecture.

Warsh and Bessent appear to understand that the old monetary regime cannot simply be restarted with another round of cheap money and optimistic speeches from the Federal Reserve.

The machine itself is being rebuilt now.

🧠 The Real Question Facing Markets

Markets still look strangely calm.

Stocks continue drifting higher. AI companies continue absorbing oceans of capital. Investors still buy dips like gamblers convinced the roulette wheel somehow owes them another winning number.

But underneath the surface, something much larger is shifting.

Warsh wants a quieter Fed that speaks less, intervenes less and restores trust through discipline rather than constant rescue operations. Bessent wants to modernize the dollar system before the fractures inside globalization widen further.

Both men now inherit a world where inflation no longer behaves politely, where energy shocks arrive through war, where tariffs reshape supply chains and where the bond market increasingly refuses to obey the old rules.

That is why a Federal Reserve swearing-in suddenly felt important enough to watch like live theater.

Immediately following the ceremony, the President made a beeline for Treasury Secretary Scott Bessent, whom he called “central casting” in his second administration. Trump made a point of shaking Bessent’s hand first among all the dignitaries assembled for the ceremony.

With Warsh sworn in, the stakes are no longer theoretical. The two most powerful men in Washington are on the job, facing enormous historical odds that they can stay the collapse of the empire of debt… for one more day.

~ Addison

P.S. Warsh may discover very quickly that the hardest part of rebuilding credibility is convincing markets the Federal Reserve can tolerate pain long enough to restore discipline. Wall Street spent fifteen years living like a teenager with his father’s credit card. What are they supposed to do now that the bill has finally arrived?

Monday is Memorial Day. Markets are closed. Enjoy your burger and beer, if that’s your thing. We’ll tune back into the drama on Tuesday.