Private credit remains one of the biggest challenges for investors right now. That’s because issues are emerging that could pose significant spillover effects on the stock market and the economy.

Yet even as the cracks widen, the curtain is being drawn over them to hide them from sight. Don’t fall for it.

How did we get here?

Private credit refers to loans made to businesses by third parties, typically business development companies (BDCs) and asset managers such as BlackRock or Apollo.

These companies embraced private credit following the 2008 financial crisis.

That’s because traditional banks stopped lending to small businesses. And they were too small or unprofitable to go public.

This environment created a great opportunity to earn higher yields than traditional loans. And most early private credit deals paid off handsomely for investors.

Like any move in the stock market, too much of a good thing became too much of a good thing.

More lenders flooded into the space, drawn by solid returns. And they took on an increasing number of questionable loans.

We’re now starting to see cracks in these loans. The collapse of First Brands late last year was a warning shot across the bow. Now, other private credit deals are coming to light.

And that’s the problem. As these deals emerge, we’re seeing the quality of the loans, the borrowers involved and the financial institutions that own them.

In other words, nobody knows who owns garbage until the stink hits.

That’s why financials as a whole have been tanking since the start of the year, even after being one of the best-performing sectors of 2025.

BDCs and asset managers like BlackRock and Apollo are down by more than 20% year to date.

In early March, BlackRock even limited withdrawals from its $26 billion private credit fund. That’s hardly a vote of confidence.

Other private credit issuers similarly started to limit – or “gate” as they call it – withdrawals from private credit funds.

If anything, it’s a sign of how this asset class is fairly illiquid, so there could be pandemonium if everyone heads for the exits at once.

But we’re also seeing that banks were making some of these loans — or providing the capital to the asset managers who were. And pension funds and family offices were investing in private credit deals.

When uncertainty rises in loan quality and loan markets, credit markets can freeze up quickly.

And that’s more dangerous to the market right now than the ever-changing headlines coming out of the Middle East.

At its best, private credit is just one more speedbump in the markets over time — and this trade may not work out as markets shake off the fears.

At its worst, it could be a repeat of the subprime loans that tipped over into the broader financial system in 2008.

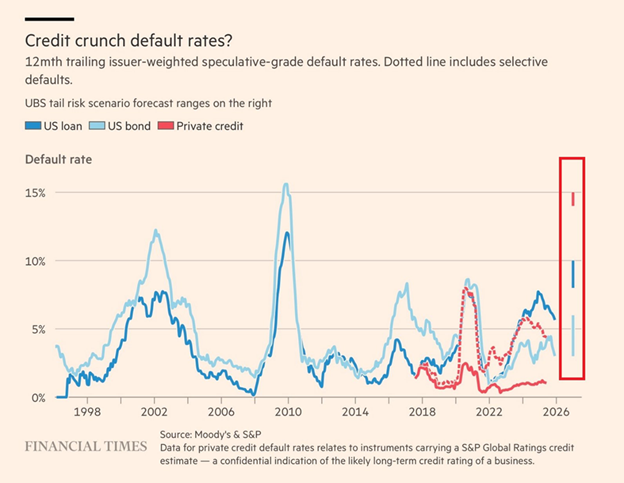

The Financial Times estimates that, based on available data, private credit could see a 15% default rate.

Private credit defaults are on track to soar based on the limited information available.

While the headline risk grows, so does the opportunity. Today, the average business development company has a book value of 0.73. That’s a 25% discount for the assets on their books.

Assuming some loans are valued at zero – a very real thing happening in the private credit markets right now – there’s still some value for the rest of the books of business as a whole.

Daring investors could start to accumulate shares of BDCs during a crisis.

Historically, during a credit crisis, like in 2008, BDCs can trade for as little as 0.35 times their book value.

In other words, they trade at $1 per share for every $3 in loan values.

BDCs tend to bounce higher when market fears subside – often driven by factors such as an emergency Federal Reserve rate cut. Aggressive investors could target names in the private credit space with an eye toward profiting in a crisis.

The top names to watch here are asset managers BlackRock (BLK) and Apollo (APO), and in the BDC space, Main Street Capital (MAIN) and Hercules Technologies (HGTC) are attractive names that pay high yields.

(Full disclosure: I’ve been long Hercules since early 2020 amid the COVID panic, and picked up some Main Street Capital during last year’s tariff tantrum.)

These aren’t specific recommendations. Rather, it’s a watch list. The private credit market will likely get worse before it gets better, but knowing what names to buy during peak fear – and names trading for 50% of their book value or less – gives you the right game plan for handling this situation.

Just remember: BDCs can have different tax implications, so make sure that it works for you and your situation.

But if any of these names drop at least 50% from their highs, chances are we’re closer to the end of a private credit panic than the beginning. That would be a great buying opportunity.

When I first started warning about private credit, they were just singing the national anthem. Now, we’re still in the early innings.

~ Andrew

P.S. These insights first appeared in the March 2026 issue of the Grey Swan Investment Fraternity monthly bulletin.

While the market has just had the mother of all rebounds, and now trades above pre-Iran conflict levels, there’s trouble in the private credit space that will continue to fester – and investors will continue to try and get as much capital out of the space as they can in the quarters ahead.

However, this has now become a slow-rolling crisis that will take time to play out. As JPMorgan Chase’s CFO reported on the company’s quarterly conference call this morning, even the biggest of the too-big-to-fail banks have about $50 billion in exposure to private credit.

They’ll want to do anything possible to delay any defaults or crisis. And over the past week, banks have started creating default swaps for private credit deals – a move that will allow them to first hedge their positions and then profit from any collapse.

For now, the trouble in private credit is on the back burner, but the signs for more trouble remain.