“Bond yields and inflationary pressure from higher oil prices,” argued our portfolio director, Andrew Packer, this morning, “make a rate cut at Warsh’s first FOMC meeting unlikely.”

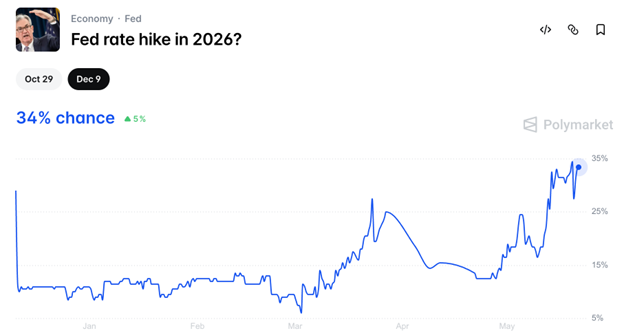

Indeed, since the beginning of March, and the onset of violence in the Persian Gulf, the Polymarket odds of a rate hike in 2026 have jumped to 35%.

You’ll note the picture Polymarket has published alongside the odds for a rate hike in 2026 still includes Jerome Powell. Perhaps it’s fitting since he elected to stay on the board, against tradition, following Kevin Warsh taking his spot as chairman of the Federal Reserve on Monday. (Source: Polymarket)

You’ll note the picture Polymarket has published alongside the odds for a rate hike in 2026 still includes Jerome Powell. Perhaps it’s fitting since he elected to stay on the board, against tradition, following Kevin Warsh taking his spot as chairman of the Federal Reserve on Monday. (Source: Polymarket)

Despite CEO Jensen Huang’s hour-long victory acceptance speech on Maria Bartiromo this morning following Nvidia’s earnings release last night, the most important market story in America right now is not the AI chipmaker.

The real drama is the 30-year Treasury yield sitting above 5%.

Under the old rules of globalization and falling inflation, that should not be happening right now.

For 40 years, investors learned to expect the same pattern every time trouble arrived. The Federal Reserve cut rates, borrowing costs drifted lower, growth stocks bounced back and Wall Street returned to business as usual, like a saloon piano player who somehow knows the tune no matter how many chairs get smashed during the fight.

This time, the piano sounds out of tune.

Jamie McGeever observed on Tuesday in Reuters that incoming Federal Reserve chairman Kevin Warsh is entering a Treasury market that is increasingly trading “without a safety net” because investors no longer assume the Fed can indefinitely suppress long-term borrowing costs through quantitative easing and emergency bond-buying programs.

That single shift explains why the market suddenly feels so strange.

The old financial regime depended on falling long-term interest rates almost as much as it depended on globalization itself. Cheap borrowing supported growth stocks, private equity, commercial real estate and government deficits all at once. Money flowed through the system like cheap beer through a casino bar at three in the morning.

Now the bond vigilantes are increasingly worried about inflation, debt expansion and industrial competition than reassured by another round of easier Federal Reserve policy.

The Fed rate-cutting cycle under Powell began in September 2024. By July 2025, the 30-year Treasury crossed the 5% threshold.

Last Thursday, on May 14, the U.S. Treasury Department sold $25 billion of 30-year bonds at a yield of 5.046%, the highest auction yield since 2007.

We’re interpreting this as the commencement of “The Great Race.”

Hear us out.

In today’s Swan Dive we’re going to tick off five current signals in the market that mirror the structural shift that led to the inflation of the early 1970s.

🛢️ The First Signal: The Physical World Is Suddenly Expensive Again

For roughly 40 years, the global economy rewarded anything that floated above the physical world. Software beat steel. Financial engineering beat manufacturing. Investors poured money into businesses that required little more than code, branding and cheap financing.

Now the physical economy is barging back through the front door like an oilman wearing muddy boots into a Manhattan cocktail party.

This morning, brent crude climbed above $108 a barrel (again) after negotiations tied to Iran’s nuclear program stalled again, renewing concerns about disruptions through the Strait of Hormuz.

Meanwhile, copper prices continue to rise as utilities, semiconductor manufacturers and AI infrastructure projects compete for industrial materials needed to expand electrical systems across the United States.

Price hikes don’t get trapped inside commodity charts. Airlines raise fares. Utility companies pass infrastructure costs onto customers through monthly bills. Contractors revise bids because transformers, wiring and industrial equipment no longer remain at predictable prices long enough to guarantee projects months in advance.

Artificial intelligence itself, Huang admitted on Bartiromo, now behaves less like a software story and more like a giant industrial electricity project.

Battery-storage construction across the United States reached record levels during the first quarter as technology firms rushed to secure electricity for AI infrastructure. The Electric Power Research Institute (EPRI) estimating data centers could consume as much as 17% of U.S. electricity generation by 2030 compared with roughly 4% today.

The digital economy suddenly depends on turbines, substations, cooling systems and natural-gas pipelines. Silicon Valley spent twenty years pretending the future lived in “the cloud.” Turns out the cloud needs an awful lot of copper wiring and electricity.

📈 The Second Signal: The Bond Market No Longer Trusts Easy Money

During the long era of structural disinflation, the Fed could usually pull long-term borrowing costs lower simply by cutting short-term rates. Investors trusted that inflation would remain contained and globalization would keep prices manageable over time.

That confidence appears to be cracking.

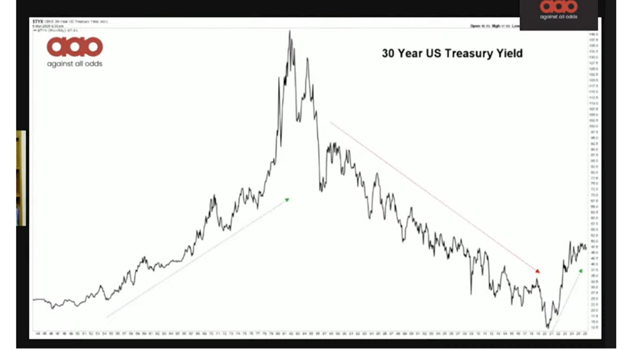

During a presentation we’ve dubbed The Great Race yesterday, we included this chart of the 30-year Treasury yield. The far right of the chart shows what we believe indicates a shift from structural disinflation of the last 40 years to a new ear of structural inflation, as bond investors require a bigger paycheck for lending the US government money. (Source: Against The Odds)

Jamie Dimon, CEO of JPMorgan Chase, warned Wednesday during the bank’s annual investor conference in New York that governments, utilities and corporations are all competing for financing at the same time.

In addition to blowing stuff up in the Middle East, the Trump Administration needs money for semiconductor subsidies, military expansion and industrial rebuilding tied directly to competition with China.

Utilities need financing for electrical-grid expansion linked to AI infrastructure. Semiconductor manufacturers require billions for fabrication plants that may take years before generating meaningful profits.

Meanwhile, lenders increasingly demand higher returns before locking money away for thirty years.

That is where Warsh enters the story.

The Federal Reserve, after 2008, repeatedly rescued financial markets whenever borrowing costs climbed too quickly. Warsh appears far less interested in rescuing financial assets and far more focused on preserving confidence in the Treasury market itself.

That is a major regime change hiding in plain sight.

Markets are already pricing in a world where Kevin Warsh takes the Fed chair . (Source: Investopedia)

A Warsh Fed may tolerate structurally higher long-term rates because it believes preserving faith in the dollar system matters more than protecting stock valuations every time Wall Street gets nervous.

That may sound harsh until you realize the alternative involves the bond market losing confidence in the government’s ability to manage debt and inflation at all.

💵 The Third Signal: Dollar 2.0 Is Already Under Construction

The third signal involves the Trump Administration quietly preparing for a world where the old globalization system no longer guarantees endless foreign demand for U.S. debt.

This month the Treasury Department expects federal borrowing to rise substantially because tax collections weakened while spending continued climbing.

But unlike earlier periods, today’s spending increasingly revolves around semiconductor manufacturing, military systems, AI infrastructure, domestic energy and strategic supply chains.

This is not temporary recession stimulus. It is industrial policy tied directly to geopolitical competition.

That helps explain why Treasury Secretary Scott Bessent has become increasingly supportive of stablecoin infrastructure and digital-dollar systems.

Most people hear “stablecoins” and picture crypto gamblers wearing hoodies in Miami nightclubs. But the strategy underneath is much more serious than that. Most dollar-backed stablecoins hold Treasury bills and short-term government debt as reserves. If digital-dollar systems become embedded in global trade and international payments, they create a new source of demand for U.S. government debt just as traditional foreign buyers become less reliable.

Under Bessent’s direction, policymakers increasingly view stablecoin infrastructure as strategically important because digital-dollar systems could help preserve global demand for dollar assets even as countries pursue alternative settlement systems outside the traditional post-Cold War financial order.

That is Dollar 2.0.

The old dollar system depended heavily on foreign governments recycling trade surpluses into Treasury bonds through globalization. Dollar 2.0 attempts to rebuild demand for dollar assets through digital payment rails, Treasury-backed stablecoins and financial infrastructure designed for a more fragmented world.

Warsh appears focused on restoring confidence in long-term Treasury markets through tighter monetary discipline, while Bessent appears focused on expanding global demand for dollar assets through Dollar 2.0 infrastructure.

Together, they look less like caretakers of the old system and more like engineers trying to rebuild the monetary engine while the car is still moving down the highway.

💻 The Fourth Signal: The Stock Market Looks Like the Nifty Fifty All Over Again

According to Bloomberg data cited this week by the Financial Times, the Magnificent Seven technology companies now account for roughly one-third of the S&P 500’s market capitalization.

That level of concentration exceeds the Nifty Fifty era in the early 1970s – the last time investors convinced themselves that a small group of dominant growth companies could keep rising forever, regardless of inflation or economic conditions.

Then inflation changed the environment completely.

The same risk exists today because many retirement accounts still depend heavily on the same giant technology companies that benefited most from cheap money and falling interest rates during the globalization era.

Investors spent years believing technology and financial assets could float above the physical economy indefinitely.

Structural inflation changes that equation because higher borrowing costs eventually pressure long-duration growth assets while capital starts flowing toward businesses tied directly to energy, industrial production and infrastructure.

🏗️ The Fifth Signal: Money Is Rotating Toward the Real Economy

The final signal confirms the rotation we’ve been writing about since the Grey Swan fraternity was founded in 2024.

While the mainstream financial media remains hypnotized by AI stocks and mega-cap technology companies, utilities, industrial firms, defense contractors, and commodity producers have quietly started taking leadership across large parts of the market because countries now compete for semiconductor capacity, electrical infrastructure, energy security, military systems and industrial independence.

Those priorities require steel mills, uranium, pipelines, transformers, copper mines and enormous amounts of construction. Our next addition to the roster of offerings to Fraternity members will be a high intensity review of opportunities in the natural resource, precious metals and rare earths space. You’ll want to keep your eyes peeled for that one!

Despite the bells and whistles that distract individual investors during earnings season, the market is increasingly rewarding businesses tied to physical infrastructure and resource security because investors are beginning to understand that the next decade may depend less on frictionless globalization and more on who controls energy, materials, manufacturing and the systems that keep modern economies running.

The old regime rewarded software engineers and financial engineers. The next one may reward electricians, miners, welders and whoever owns the copper.

~ Addison

P.S. The market still thinks this is another ordinary Fed cycle. That may be the biggest mispricing of all.

The bond market, commodity markets and the quiet rotation underneath the stock market increasingly suggest we are moving into a world where money becomes more political, energy becomes more strategic and industrial capacity matters again.

Investors who continue managing portfolios as though it is still 2017 may discover the next decade behaves a lot more like 1974.