Reading the monthly CPI report this morning, it’s hard not to see the side “excursion” in Iran as an egregious own goal by the Trump administration.

At the very least, it will make retaining the majority in the House of Representatives in November that much harder.

The episode gives a twinge of intrigue and suspense to the AI bubble narrative we had been heretofore preoccupied by…

What we’d rather be doing is keeping our eyes on the aureate horizon—the “golden age” every civilization, including ours, assumes it is building toward.

But we are also beholden to statistics, more statistics and damned lies. Let’s begin…

🛢️ Energy Prices Jump in March

The Bureau of Labor Statistics (BLS) reported that consumer prices rose 0.9% in March from February, the largest monthly increase since the inflation spike in 2022.

Energy did the heavy lifting. The energy index jumped 21.3% in a single month—the biggest move in records going back to 1957—as tanker traffic through the Strait of Hormuz slowed during the Iran conflict.

Gasoline and diesel prices rose more than a dollar per gallon over the same stretch. The annual CPI now reads 3.3%, up from 2.4% the month before, matching economist expectations reported by Dow Jones and The Wall Street Journal.

That number lands on desks in Washington just days before a different kind of conversation. Michael Kratsios, director of the White House Office of Science and Technology Policy, and Reid Hoffman, a founder of the PayPal Mafia will sit with policymakers and CEOs at Semafor World Economy next week and ask a question that doesn’t fit neatly into a CPI release: Can the current version of American capitalism carry another half-century of technological leadership?

The version that built Silicon Valley and is starting to look very different today?

Federal funding flowed through defense research and university labs during the Cold War. Immigration policy expanded the talent pool. Venture capital-backed engineers who left established firms to start new ones. The internet’s backbone emerged from public investment before private companies turned it into a commercial system.

With the impending mega IPOs like SpaceX sucking all the oxygen from the room, the burden is shifting from public markets to private balance sheets.

Data centers, chips, and power supply are financed by firms spending at a scale that rivals earlier national projects. At the same time, consumer demand has concentrated.

Moody’s Analytics estimates the top 10% of earners now account for nearly half of consumption, a reversal of the broad middle-class demand that supported earlier expansions.

🌎Hegel’s World Spirit and the Long Debt Cycle

The big picture: In Georg Wilhelm Friedrich Hegel’s framework, the “World Spirit” moves through nations that organize economic and political life in ways that define an era.

President Trump is duly tapped into the “Hegelian Dialectic” as my tutors at St John’s Graduate Institute in Philosophy would call it.

In modern history, that role has often aligned with the issuer of the world’s reserve currency. Portugal, Spain, the Netherlands, France, Britain, and the United States each held that position in sequence, with financial systems expanding alongside political reach.

Each cycle carried its own balance sheet. Spain financed wars across Europe and defaulted multiple times in the sixteenth century.

The Dutch extended credit through trade and military commitments that strained their system.

Britain’s debt climbed toward 250% of GDP during the world wars before financial leadership shifted.

The United States now operates with public debt exceeding $36 trillion and annual interest costs above $1 trillion.

So, we ask again: Can the current version of American capitalism carry another half-century of technological leadership?

Through the fog of a double-edged ceasefire, we keep calm and carry on.

Please Note: To that end, in the Grey Swan Trading Fraternity, Andrew Packer has been keeping on the short view in the markets. In one two-day trade, he closed a 207% gain on CoreWeave (CRWV) calls this morning.

Please keep your eyes peeled on Monday for the launch of a new portfolio of Shadow Stocks, too, that will help us trade headline news cycle events in quick bursts.

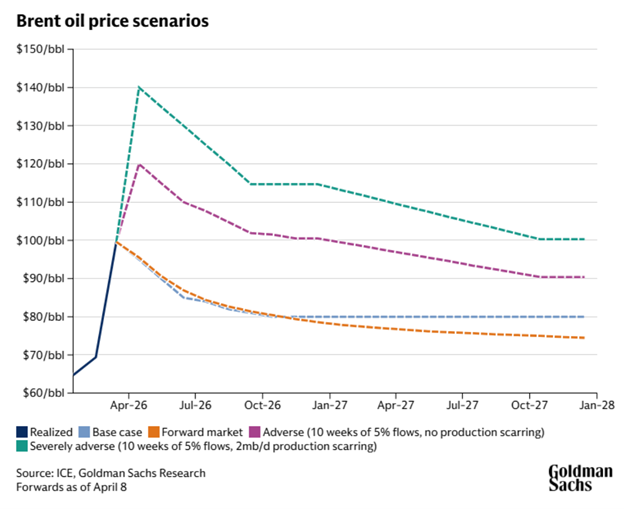

🛢️ Oil Prices Fall After Ceasefire

Brent crude settled in at $95 per barrel this morning, down from $109 Tuesday after the announcement of a two-week ceasefire between the United States and Iran.

Taking a peek at Goldman Sachs trading notes, the bank continues to forecast an $80 average price in the fourth quarter, a level set after raising expectations in March due to Gulf supply disruptions.

Daan Struyven, co-head of global commodities research, says the forecast is tied directly to their assessment and speed of recovery in tanker traffic and regional production. (SourceL: Goldman Sachs.)

Daan Struyven, co-head of global commodities research, says the forecast is tied directly to their assessment and speed of recovery in tanker traffic and regional production. (SourceL: Goldman Sachs.)

That said, a delay in reopening the Strait of Hormuz by a month shifts Goldman’s expected average toward $100. A prolonged reduction in output of two million barrels per day pushes projections toward $115. Which, umn, we don’t want to see.

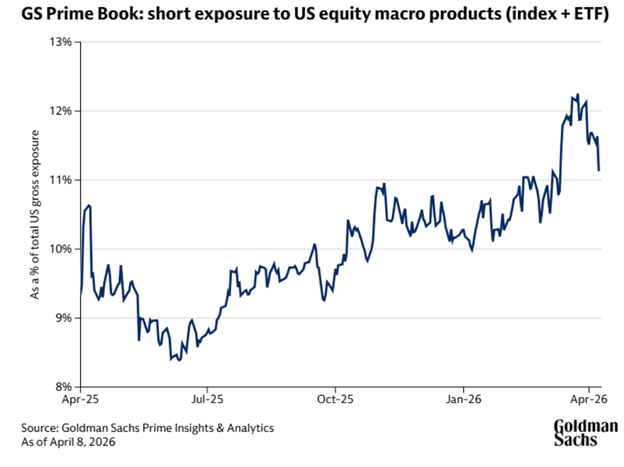

📉 Investors Cover Short Positions

Here’s an interesting note to tack on to the market action this week.

Traders covered their shorts faster than anticipated, suggesting the market is treating the “excursion” in Iran as just a distraction.

During the Iran escalation mid-March, large investors piled short positions over geopolitical concerns on top of their previously nervous shorts due to the extreme concentration of capital in AI stocks.

Since the ceasefire, those short have returned to their average level of concern for rising indexes.

🛠 Three New Investment Themes Identified

Goldman Sachs CIO Digest highlights three areas drawing capital, which we’re well aware of.

Commodities tied to energy and artificial intelligence infrastructure are receiving increased attention as demand for power rises.

And as we’ve been speculating, a pipeline of large public offerings is forming among firms positioned in AI systems and services. Japan is shifting toward higher interest rates and a tighter labor supply after decades of deflation, changing its role in global capital markets.

The same report flags additional risks in credit markets, particularly in lower-quality U.S. collateralized loan obligations with software exposure.

First-quarter earnings begin next week.

Energy companies report early. Firms with direct exposure to fuel costs report later in the season. The sequence runs from producers receiving higher prices to downstream companies reporting the effect of those costs as they move through production and distribution.

That’s how the rat gets digested through the belly of the boa.

📊 Small-Caps Lead the Way Out Of Crisis

During the aftermath of the 2008-09 financial crisis, we recall quite fondly calling the shift in markets away from large-cap and financial stocks to small-cap start-ups in tech and the commodities sector.

Our colleague Adam O’Dell is making a similar observation in Money & Markets this morning.

Adam reports his portfolio moved through the conflict with several positions above pre-war levels, including MARA Holdings, YPF SA, Rush Street Interactive, Natural Gas Services Group, Amprius Technologies, and TSS Inc. Amprius rose nearly 60% during the period, and TSS increased about 30%.

Across the small caps, the Russell 2000 index is up 6% this year, while the S&P 500 remains down with increased pressure in SaaS stocks and AI hyperscalers.

As an aggregate, from April 1999 to April 2006, the Russell 2000 outperformed the S&P 500 by 99%. From January 2008 to March 2014, small caps outperformed large caps by 28.2%.

Those periods followed heavy infrastructure investment, including telecommunications networks, which also involved natural resources and rare-earth supply chains… and they are set up to repeat the cycle again in 2026.

It’s Friday. We leave you for the weekend with one eye on the aureate horizon and the other on the energy and commodities ticker tape.

Enjoy the weekend,

~ Addison

P.S. It’s an appropriate year to be contemplating America’s Golden Age.

That’s why this week on Grey Swan Live!, we sat down with Dr. Mark Skousen at — right as markets are trying to find their footing again.

With headlines shifting, oil prices stabilizing and investors recalibrating expectations in real time, he’ll be breaking down what’s signal… and what’s just noise.

And he’ll share where the most compelling opportunities could be taking shape as this next phase of the market unfolds.