At a White House briefing scheduled for noon today — an hour chosen, one suspects, for its symbolic proximity to deadlines — Treasury Secretary Scott Bessent attempted to soften the ritual sting of Tax Day.

Standing beside Small Business Administrator Kelly Loeffler, he assured reporters the “Big Beautiful Bill” was performing exactly as advertised.

The market, ever agreeable when liquidity is plentiful, seemed to nod along. As Bessent outlined the benefits, the S&P 500 Index climbed to fresh record highs, as though the act of redistribution itself were a form of stimulus.

In Bessent’s accounting, the benefits arrive in tidy bullet points:

- Households are receiving larger refunds this filing season, with the Treasury projecting that between $100 billion and $150 billion will be returned to taxpayers.

- The legislation makes the 2017 tax cuts permanent, removes federal taxes on tips and overtime income, expands relief for seniors and increases the Child Tax Credit by a permanent $500.

- Roughly 12 million small business owners are seeing average tax savings of $7,000 under the new provisions.

- The average filer, we’re told, can expect $1,000 to $2,000 deposited back into their accounts — just as soon as the machinery of government completes its leisurely turn.

On the surface, it’s a generous arrangement. A bit like a restaurant that returns a portion of your bill after quietly raising the menu prices.

🏦 U.S. Deficit Expands, Again

Not to dampen market euphoria, but if you’re keeping score at home: Government tax receipts increased 5% year over year (YOY) to $385 billion. The credit card got charged… 4% more, totaling $549 billion.

The official U.S. budget deficit totaled $164 billion in March, exceeding expectations by an additional $12 billion; a figure that will almost certainly be revised upward once the final costs of the Iran excursion are tallied.

Wars, like home renovations, rarely come in under budget and suffer from “mission creep.”

Every year, on this date, the Peter G. Peterson Foundation issues your tax receipt with the smug hope of getting taxpayers to digest what their government is spending your money on. (Source: Peter G. Peterson)

Every year, on this date, the Peter G. Peterson Foundation issues your tax receipt with the smug hope of getting taxpayers to digest what their government is spending your money on. (Source: Peter G. Peterson)

Over the first six months of fiscal year 2026, the U.S. deficit reached $1.17 trillion, the third-largest on record. Interest expense increased 7% YOY to $623 billion for the same period.

You’ll note interest is now the second-largest federal spending category behind Social Security.

🧮 U.S. Tax Revenues Lag Peers

The Peterson receipt came with this curious feature of the United States’ financial system.

A full year into President Donald Trump’s rearrangement of the global tariff structure, federal revenue continues to rely on individual income taxes, which account for a larger share of total receipts than in any other G7 economy.

Canada, France, Germany, Italy, Japan and the United Kingdom each combine income taxes with a national value-added tax, which ranks among their largest revenue sources. The United States does not impose a national consumption tax. That honor is reserved for 45 of the 50 states.

Corporate income taxes in the United States are set at roughly 26%, near the G7 average of 27%, while capital allowances and credits reduce effective tax rates slightly below peer levels.

Governments across the OECD increasingly rely on tax-based incentives to drive business research and development, and U.S. firms report R&D spending above the G7 average as a share of GDP.

Taxes on labor remain lower than in most G7 countries, with OECD data showing a smaller portion of total compensation paid through income and payroll taxes across multiple household types.

Total federal revenue, measured as a share of the economy, remains below that of other advanced economies.

In short: Americans are taxed less directly than their peers — and borrow more to make up the difference.

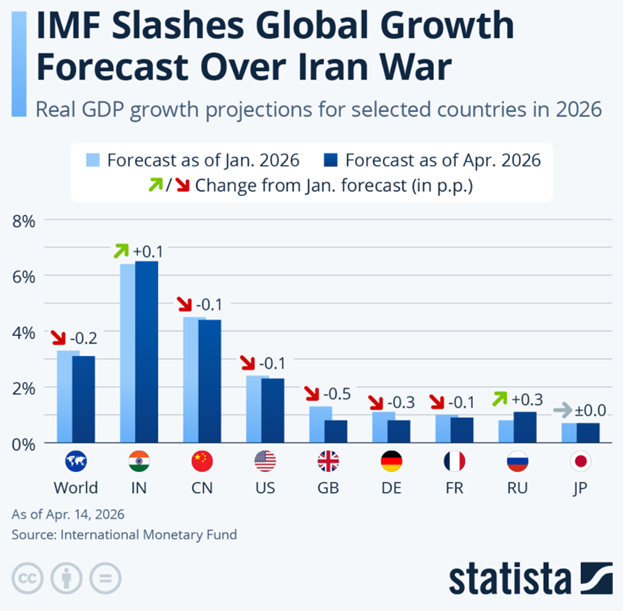

📉 IMF Cuts Growth Forecast

Also a fitting tribute to Tax Day, the International Monetary Fund reduced its 2026 global growth forecast to 3.1% from 3.3%, assuming the conflict in Iran remains limited in duration, intensity and scope, with disruptions easing by midyear.

The IMF projected growth rising to 3.2% in 2027, still below the 2000 to 2019 average of 3.7%.

If the energy shock from the blockade of the Strait of Hormuz is prolonged, the IMF estimated growth could fall to 2.5% in 2026, with further declines toward 2% if additional damage occurs to regional energy infrastructure.

Across the board, the IMF dinged global growth expectations. The United Kingdom’s forecast was reduced to 0.8% growth, Germany’s to 0.8%, and forecasts for the United States, France and China were revised lower by smaller margins.

Only India and Russia, say quants at the IMF, will grow this coming year. India’s outlook improved following reduced tariffs on exports to the United States, while Russia’s outlook improved with higher commodity prices supporting export revenues.

Forecasting, in polite company, is still considered a science. For his part, Bessent dismissed recession forecasts from the IMF and World Bank as overreactions and suggested U.S. GDP growth could exceed 3% to 3.5% in 2026.

📈 Stock Indexes Reach New Highs

The S&P 500 traded above 7,200 intraday for the first time since January, advancing roughly 0.4% to 0.5% during the session. The Nasdaq Composite gained about 1% and extended its run to 11consecutive advancing sessions, while the Dow Jones Industrial Average declined approximately 220 points in afternoon trading.

Technology and growth stocks led the advance, with index-heavy names absorbing the majority of flows during the session. Financial stocks moved higher following first-quarter earnings from Bank of America and Morgan Stanley that exceeded analyst expectations on revenue and net interest income.

Energy shares declined nearly 10% over the prior 11sessions as crude prices pulled back on expectations tied to negotiations in the Middle East. Trading activity concentrated early in large-cap names and extended as systematic buying programs followed the initial move higher.

🧠 Index-schmindex – Shadow Stocks Are On Fire

With today’s surge, the S&P 500 has now rallied for nine straight trading days. And despite some concerns over energy supply chains, prices are now up by nearly 3% on the year.

All three major indices have been relatively flat in 2026, trading within narrow ranges. But individual equities have recorded gains of 100% to 300% over short periods.

As we’ve mentioned, this is a historically rare trading setup we’ve been treated to so far this fiscal year.

In very broad strokes, the AI trade is messing with the traditional flow of capital across all sectors:

Capital concentrated in companies tied to specific catalysts, including data center construction, semiconductor supply agreements, and energy infrastructure buildouts are still linked to AI “demand.”

Firms building compute capacity have committed to large capex investments, while smaller firms using that infrastructure are reporting revenue growth tied to new applications and contracts.

Price movements have been following earnings revisions, project announcements, and capacity expansions rather than broad index flows.

It’s a curious setup, indeed. To borrow the Goldman Sachs term, “dispersion” across sectors has fueled individual stocks, with some advancing sharply while others are getting whacked.

The index remained “range-bound” over the same period. We dug deep into the research on this Shadow Stocks for a new upgrade to our daily email publications. (See details on the upgrade in the P.S. note below.)

🏛️ Federal Reserve Drama Heating Up

Despite the Justice Department’s probe into Federal Reserve Chairman Jerome Powell’s alleged perjury before Congress, Secretary Bessent also urged the Trump administration to slow their roll… and suggested the Federal Reserve should “wait and see” before adjusting interest rates while the Iran conflict remains unresolved.

Bessent broke ranks with President Trump, saying the central bank is “doing the right thing by sitting and watching” developments in energy markets and inflation data.

As we reviewed yesterday, and again this morning, inflation data released Friday showed consumer prices rising three times faster in March than in February, driven by increases in oil and gas costs tied to the conflict.

Core inflation excluding food and energy rose slightly less than forecast.

Bessent said, “If ever there was ‘Team Transitory,’ it’s this,” and added that earlier expectations for growth above 4% will require recovery from the current quarter’s slowdown.

Trump’s still posting on Truth Social and X that interest rates are going down as soon as he can get Kevin Warsh confirmed to the chairman’s seat. We expect the drama to escalate next week, now that cheerleading over the Big, Beautiful Bill has reached its peak! More to come…

📜 Well, Nobody’s Perfect, Right?

If it’s not too obnoxious to point out on National Tax Day, the third President of the United States, the man whose most famous quote is “the government that governs best, governs least,” died in debt.

Thomas Jefferson inherited land, income and productive assets, yet owed more than $100,000 at his death in 1826.

Most of the money he spent during the construction and reconstruction of Monticello over nearly three decades went toward imported materials, expanding the estate’s acreage and maintaining a large personal library and a collection of imported European wines.

Jefferson famously entertained frequently and extended financial support to friends and relatives, at times assuming their debts. He used slaves as collateral for loans arranged through Dutch banking houses.

Between March 1802 and March 1803, Jefferson recorded construction expenses totaling $3,587.92, equivalent to more than $1 million today. And he had to borrow extensively to complete the work.

Curiously, as president, Jefferson argued that eliminating the national debt should be the federal government’s highest priority, opposing Alexander Hamilton, who supported using the national debt as a financial instrument.

Apparently, even the most eloquent advocates of fiscal restraint have a way of living beyond it.

Today, the once-vibrant debate over the national debt and how it should be used has all but disappeared from the electoral platforms of both national parties.

~ Addison

P.S. While today’s roller-coaster market drags on and headlines distract investors, the real action is happening where few are looking.

In this week’s Grey Swan Live!, we’ll show you how to cut through the noise, identify these “shadow stocks,” and understand the catalysts driving triple-digit moves — before they become obvious to everyone else.