President Donald Trump ordered a five-day pause on U.S. strikes against Iranian power plants and energy infrastructure, describing “productive discussions over the past two days toward fully resolving hostilities in the Middle East.”

The pause marks the first direct negotiations since the war began on February 28. It applies specifically to power generation and export-related energy facilities. The order remains conditional; strikes resume if negotiations stall.

The clock runs for five days.

📈 Futures Jump, Crude Breaks

On Wall Street, S&P 500 futures rose 2.5% within minutes of the announcement. At the outset of hostilities in the Gulf, we listed the Kobeissi summary of Trump’s crisis playbook here in Swan Dive.

The strategy includes an announcement late on Friday that makes markets nervous and a Truth Social post before the open on Monday morning. This morning’s rally fits the bill by something like 100%.

WTI crude fell 11% as traders recalculated near-term supply risk tied to Iranian export capacity.

Gold and silver recovered from last week’s historic sell-off, a liquidation that followed rising oil prices and renewed inflation fears. Energy producers gave back early-session gains. Refiners retraced part of their war premium.

Airlines and transport names firmed up as jet-fuel assumptions shifted. Options desks repriced volatility lower and rolled off short-term hedges.

The move unfolded on screens before the first tanker changed course.

We’d say Trump is being overly dramatic if, in fact, so many lives and livelihoods weren’t at the whim of social media.

🛢️ Hormuz Still Sets the Terms

With that said, the Strait of Hormuz remains effectively closed. Transit through the passage still depends on naval escort patterns, insurance underwriting and clearance from regional authorities.

Several carriers continue to reroute or idle vessels while bean counters at underwriters’ desks in London and New York assess their ships’ exposure.

Iran’s Foreign Ministry, of course, denies direct talks with Washington, D.C. and accuses the White House of “buying time” while regional de-escalation efforts continue.

The pause reopens a diplomatic window; an “off-ramp” for the Trump administration, a cynic would argue.

⚠️ A (Feeble?) Warning to the Funding Channel

Curiously, Mohammad Bagher Ghalibaf, Speaker of Iran’s Parliament and former IRGC commander, posted late Sunday on X: “Financial entities that finance the US military budget are legitimate targets.”

Ghalibaf added, “Purchase them, and you purchase a strike on your HQ and assets. We monitor your portfolios.”

The language identifies holders of U.S. Treasurys as active participants in the conflict.

In other words, the Iranian threat shifts attention from physical infrastructure to financial infrastructure — clearinghouses, banks and institutional investors that hold U.S. sovereign paper.

📊 Foreign Holders of U.S. Debt Add to Their Positions

No one seems to care. Or at least, leading up to Ghalibaf’s threat, they didn’t.

The most recent tabulations available show that as of January, foreign holdings of U.S. Treasurys increased $34.8 billion to $9.31 trillion, according to the Treasury Department.

Japan added $39.8 billion, lifting its position to $1.23 trillion — the highest level in three years. The United Kingdom added $29.3 billion to $895.3 billion, near a record.

The European Union increased holdings by $8 billion to $2.13 trillion.

Even China added $10.9 billion to $694.4 billion, near its lowest level since 2008.

Japan’s purchases reflect yield differentials between U.S. Treasurys and Japanese government bonds, as well as coordination on semiconductor supply chains and defense posture in the Pacific.

The U.K. operates as a global financial hub, recycling capital through the city while aligning with sanctions enforcement and NATO commitments.

European Union members continue to hold Treasurys as reserve assets while negotiating tariff and AI regulatory frameworks with Washington, D.C.

China’s incremental addition occurred amid aggressive gold buying that we’ve been chronicling.

Altogether, foreign holdings of U.S. Treasurys totaled $9.31 trillion in January.

The broader pattern shows that the Western financial system’s allies have either maintained or expanded their dollar exposure amid an active Middle East conflict.

🧮 Thirty Years of Arithmetic; A $99 Trillion Bill

How long can that trend last? It’s a question worth asking…

The Congressional Budget Office (CBO) released new projections on Friday.

The new CBO forecasts show debt held by the public at 99% of gross domestic product (GDP) in fiscal 2025, rising to 175% by 2056 under current law.

That’s a trend that would make a classical economist break out in hives.

Federal outlays will increase from 23.1% of GDP to 27.9% over that period.

As has been the case since the 1980s, revenues will rise more slowly, reaching 18.8% of GDP, down from prior projections that anticipated 19.3%.

The estimates predate the Supreme Court ruling that invalidated portions of tariff collections, suggesting potential downward pressure on future revenue assumptions.

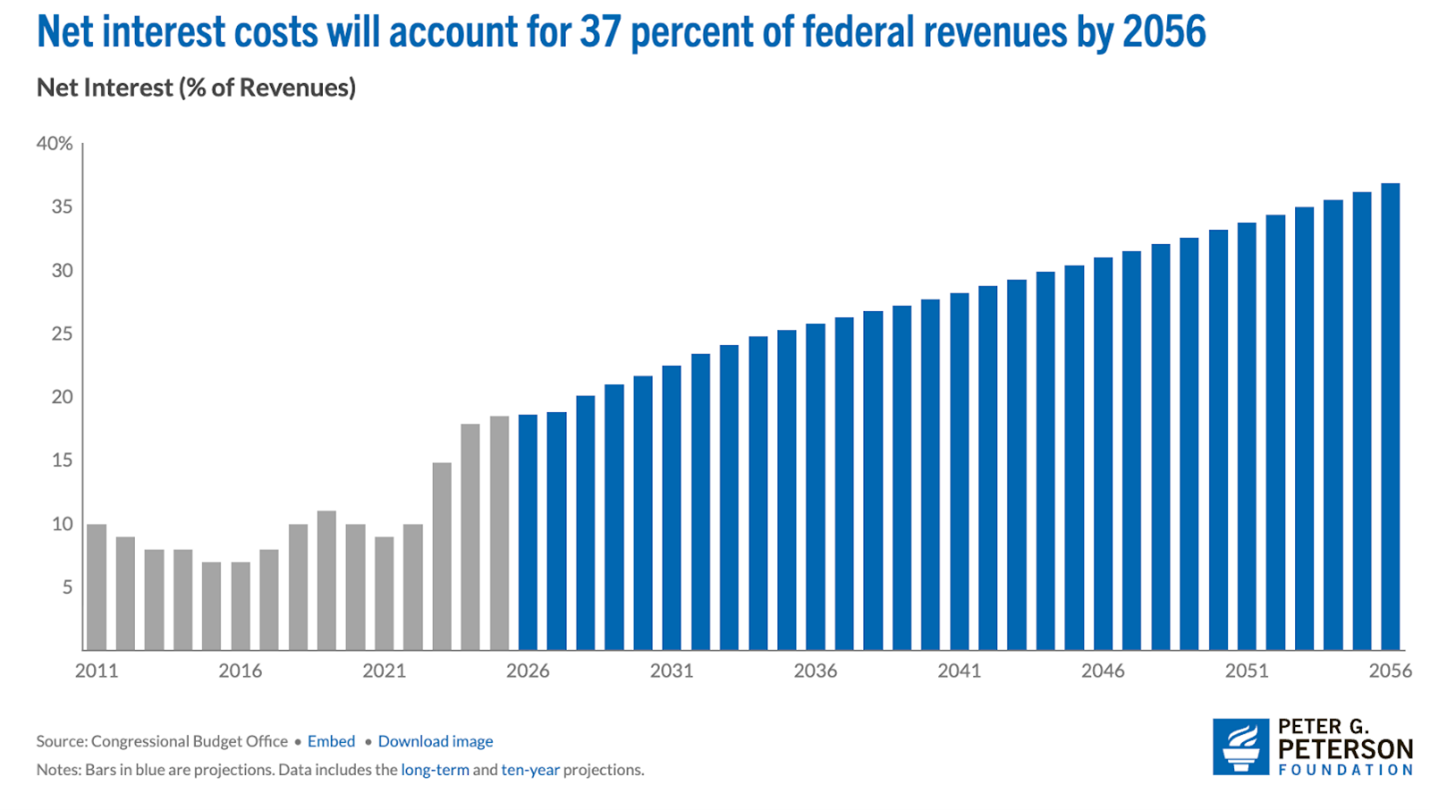

Interest rates on outstanding debt average 3.4% this year and reach 4.2% by 2056. The CBO projects a cumulative interest costs of $99 trillion across three decades. (Source: The CBO and Peter G Peterson Foundation)

By 2056, interest accounts for 6.9% of GDP and approximately 37% of federal revenues. Interest outlays surpass defense spending today, exceed Medicare by 2028 and overtake Social Security by 2047 under current projections.

Social Security’s Old-Age and Survivors Insurance Trust Fund depletes in 2032, triggering an automatic 23% reduction in benefits absent legislative action.

The Medicare Hospital Insurance Trust Fund depletes in 2040, 12years sooner than prior estimates.

Real GDP growth averages 1.7% annually across the 30-year horizon, declining from 2.4% in 2026 to 1.5% by the end of the projection window.

🌴 Miami: Oil, AI and Capital Formation

The stakes are high for Trump to get his grand realignment strategy firing all pistons before the November 3 midterm elections.

On Thursday, March 26, Trump is expected to attend a Saudi-hosted conference in Miami, typically held in Riyadh.

As we’ve been forecasting, the event places Saudi capital and influence on U.S. soil as discussions center on energy output, AI infrastructure and long-term industrial alignment.

Earlier this year, energy equities advanced sharply following the overnight capture of Nicolás Maduro. Exxon, ConocoPhillips, Chevron, Halliburton, and Schlumberger moved higher as markets repriced access to Venezuelan supply.

Those oil production shifts translated directly into stock price hikes and massive capital investment decisions.

The modern Saudi Arabian state has been built on hydrocarbons and its outsized influence on the OPEC nations. With Venezuela out of the way and Iran otherwise occupied, the Saudis appearto be calling the production shots in Opec once again.

Following a series of meetings with Trump, the Saudi Prince Mohammed bin Salman has publicly announced that he wants his country’s capital strategy and influence to extend into AI, large-scale data centers and grid expansion.

What’s at stake? Energy and AI share the same constraint: reliable megawatts.

AI processing requires continuous electricity at an industrial scale. In the prince’s view, hydrocarbon revenue can finance generation capacity to power server farms.

Andrew Packer has been providing stalwart guidance during the Middle East conflict to our Grey Swan Trading Fraternity members. If you’d like a closer look at the trades that major swings in the energy and resource markets have resulted in, please review: Urgent: Middle East Alert.

📜 “OK” and Endurance

On March 23, 1839, editors at the Boston Morning Post abbreviated misspelled phrases for amusement. “Oll Korrect” – kitchy spelling of the slang of the day – became “OK.” The Boston Morning Post printed the term as part of a joke.

When President Martin Van Buren sought reelection, his supporters organized the “O.K. Club,” referencing “Old Kinderhook,” his hometown in New York.

Opponents claimed Jackson invented the abbreviation to disguise his own illiterate misspelling of “all correct.”

Years later, Columbia linguist Allen Walker Read later traced the term’s origins and dismissed alternative theories involving rum ports, army biscuits and Native American signatures.

Read even debunked the widely popular social media meme that OK was how Americans planned to meet their French girlfriends at the docks, greeting troop transports:

The mademoiselles would say “Au quai.”

The young hayseeds would reply “OK!” with a thumbs up, knowing not what they’d agreed to.

As romantic as that one sounds, “OK” entered political vocabulary long before the U.S. was engaged in the European world wars and has survived partisan bickering ever since.

Trump’s crisis playbook seeks a fresh OK every Monday for the markets, regardless of whether he’s spooking them with tough tariff talk, territorial ambitions in Panama and Greenland or lobbing very expensive high-tech doodlebugs at a target in the Gulf.

At least this morning, he got a big one.

~ Addison

P.S. Last week on Grey Swan Live!, our natural-resources specialist, Shad Marquitz, provided a prescient look at gold and oil price volatility; the “whack-a-mole” trading environment set in motion by the war in Iran.

Shad systematically covered the mosaic of natural resource opportunities in oil, liquefied natural gas, antimony, tungsten and precious metals following the Iran bombing excursion.

If you’re looking for more than just a further investment in gold, look no further – Shad shared a list of smaller-cap companies that look promising across the commodity space now.

The replay is up on our site now. And catch Shad’s article in our recently-released March issue, looking at merger & acquisition activity in the gold miner space.

This week, we’ll have my interview with Ronan McMahon from Panama City. Stay tuned for more details before Thursday, March 26, at 2 p.m. ET.