The U.S. 20-year Treasury yield moved back above 5.00% before the open this morning, less than 24 hours after President Donald Trump said the Iranians are begging for a ceasefire.

Whether that claim holds up is anyone’s guess. The market and the economy remain in wait-and-see mode.

A quick scan of the macro tape looks like a parking lot after a Grateful Dead concert in the early 1980s.

Goldman Sachs joined Moody’s and Morgan Stanley in raising U.S. recession odds to 30%, the third increase in 90 days.

Oil remains the hinge. Overnight, WTI pushed back above $96 after Qatar’s energy minister warned prices could reach $150 within two weeks. In July 2008, oil reached $147, and the U.S. economy stalled soon after. The stock market followed within 60days.

That kind of price increase, we know from experience, rubs an economy – built on just-in-time consumption and layered debt across households, corporations, and government – the wrong way.

As long-term Treasury debt rose, mortgage rates approached 7% again. Gasoline moved toward $4 per gallon nationwide. Fertilizer and helium prices are making headline news.

Employers appear to be adjusting. Hiring has slowed as energy costs rise and productivity gains from AI remain uncertain. Retail margins have narrowed.

Politics run alongside all of this “chaos. Betting markets now place the odds of Republicans losing the House of Representatives in November at 84%. So… what’s a sitting president to do?

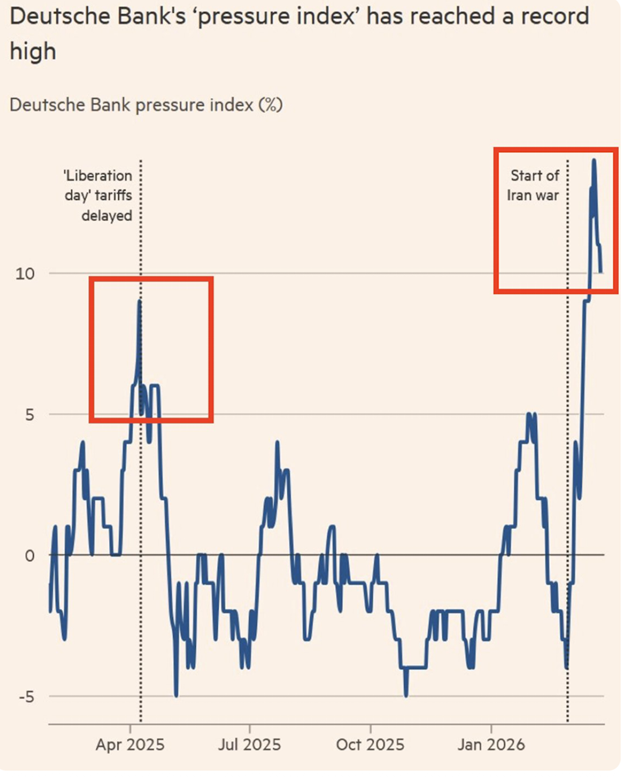

📊 The Pressure Index Hits the Ceiling

In an effort to get a bead on Trump’s very public and transparent policy reversals, Deutsche Bank strategists constructed a composite index to anticipate when he’s likely to crack under pressure and yield to political pressure.

According to Deutsche Bank’s Pressure Index, we’re due for a policy reversal from President Trump. But as Larry Fink suggests, now that the fight’s underway, the danger of leaving the job undone is global recession, or worse. (Source: Deutsche Bank and Financial Times)

According to Deutsche Bank’s Pressure Index, we’re due for a policy reversal from President Trump. But as Larry Fink suggests, now that the fight’s underway, the danger of leaving the job undone is global recession, or worse. (Source: Deutsche Bank and Financial Times)

The Pressure Index tracks approval ratings, inflation expectations, equity prices and Treasury yields based on a sequence observed through 2025 trading: tariff announcements were followed by equity declines, approval ratings weakened and policy adjustments followed within days.

The same components now align more tightly.

The S&P 500 Index has declined more than 5% from its January high. The 2-year Treasury yield has recorded its largest monthly increase since the last tightening cycle.

Futures markets now price a Federal Reserve rate hike! That was unthinkable a month ago, before hostilities began on February 28. From the administration’s view, Kevin Warsh’s confirmation to replace Fed Chair Jerome Powell will not arrive soon enough.

We’ll also get a glimpse of what Trump has up his sleeve at the Saudi-backed Future Investment Initiative (FII) Priority Summit on Friday, March 27, in Miami Beach. The Prez is scheduled to deliver a keynote address. Click here for our immediate forecast and how to play the investment angle.

🪖 Four Military Options, One Map

In an interview with the BBC posted to X this morning, BlackRock’s Larry Fink said “the quiet part out loud.”

Fink implied the U.S. must finish the war with Iran at all costs, because losing it means a great(er) recession. Potentially a Depression, even.

“If there’s a cessation of war and Iran remains a threat… we could have years, years of $100 to 150 oil.”

Still, opening the Strait of Hormuz to the free movement of freight remains a complex puzzle.

Axios reported four Pentagon options under consideration: blockading Kharg Island, seizing Larak, taking Abu Musa and adjacent islands or interdicting Iranian oil shipments east of the Strait of Hormuz.

Each option intersects with the same shipping geometry. It’s the very definition of a chokepoint.

Kharg handles the majority of Iranian crude exports. Larak and Abu Musa sit near the narrow passage where one-fifth of global oil flows.

Interdiction on the eastern side reaches cargo already moving toward Asian buyers. Control over those points determines which barrels move, which ships clear insurance and which routes remain viable.

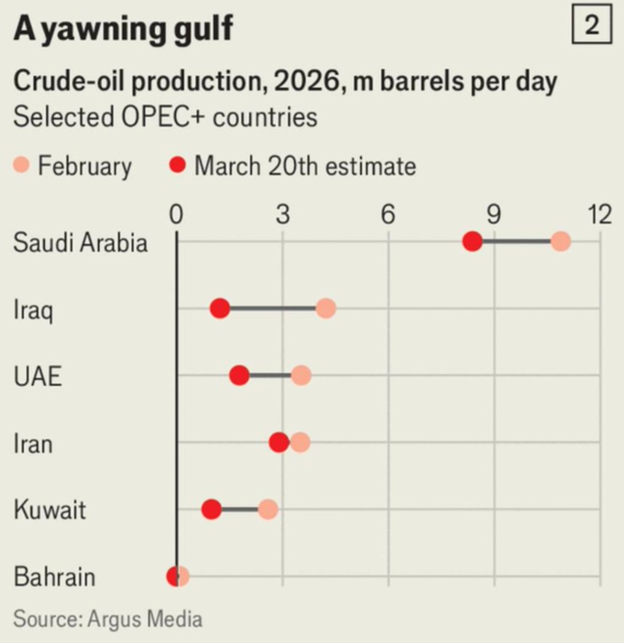

Gulf producers have reduced output by roughly 10 million barrels per day, removing volume from global markets while prices remain above $100 per barrel. (Source: Argus Media)

In a very real way, this is not the United States’ or Israel’s problem, even if they forced the issue. The dependency sits unevenly across importing nations:

- Japan at 73%

- South Korea at 70%

- Pakistan at 60%.

- India at 42%

- China at 40%

In addition to reduced production, cargo that does not pass through Hormuz has been forced to plot longer routes, extending transit times and boosting insurance premiums.

🌍 Debt, the Cycle, and the World Spirit

Amid the fog of war and reams of not-so-savory data, it helps to step back and look at the longer arc of history.

Ray Dalio describes a “Big Cycle” driven by five forces moving together: the financial system, domestic politics, the international order, technology and natural disruptions.

Late in that cycle, debt grows faster than income, internal divisions widen, external pressures build and lenders demand higher compensation. Treasury yields are where those forces meet a price.

Georg Wilhelm Friedrich Hegel framed the progression differently.

The “World Spirit” moves from one dominant power to the next as each system exhausts the principle that made it effective.

In monetary terms, that principle shows up as the reserve currency.

Since the Age of Exploration, the sequence has followed a familiar path. Portugal opened global trade routes. Spain followed with silver-backed currency and defaulted under the weight of imperial wars. The Dutch built a financial system centered in Amsterdam and lost discipline as banking supported state obligations.

France extended its influence through military reach on the continent.

Britain financed global trade through the Industrial Revolution and ceded leadership after two world wars pushed debt toward 250% of gross domestic product (GDP).

The United States inherited the system in the 20th century, formalized it at Bretton Woods in 1944 and extended it through Treasury markets and dollar settlement.

Each transition followed the same mechanics: war financed with debt, balance sheets stretched and creditors demanding higher yields or moving capital elsewhere.

The United States now operates within that same structure. Public debt exceeds 120% of GDP. Annual interest expense has moved beyond $1 trillion. Treasury issuance continues to fund deficits and military commitments. Yields adjust to clear that supply.

Global trade still clears largely in dollars, but settlement channels are branching. Sanctioned energy flows move outside traditional systems. Digital rails develop alongside sovereign currencies. Large commodity consumers operate outside the U.S. alliance structure.

🪨 Capital Rotates Toward Inputs

So, what’s an investor minding his own business to do? One thing you can do is admit that daily populist politics is annoying at best. A waste of time on a good day. Better to remember that simple principles serve investors and nations better than complex ones. Save. Invest. Produce.

Lather. Rinse. Repeat.

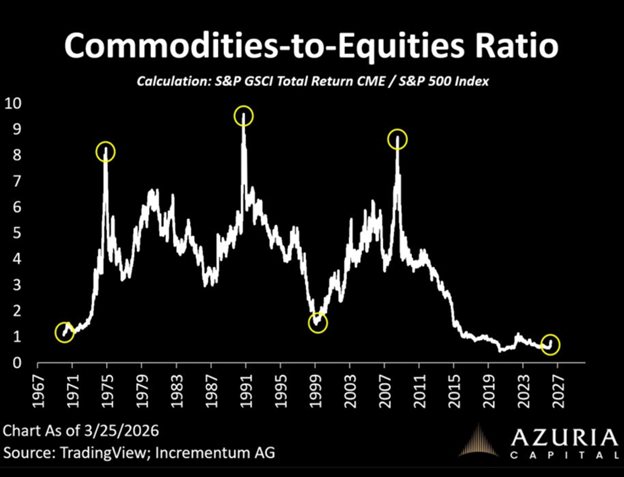

A wider view of markets shows that shifts during the conflict and financial stress, caused by debt failures or otherwise, point toward commodities and natural resources.

We fondly recall the seismic shift towards natural resources and rare earths following the 2008 global financial crisis. You can see the spike depicted here on this graph of the S&P GSCI Total Return Index, a premier, broad-based commodity benchmark vs. the tech-heavy S&P 500. We’re due for another reversal. (Source: Tavi Costa on X; Azuria Capital)

In our last Grey Swan Live! with Shad Marquitz, we covered 22 companies that are poised for dramatic growth during a new commodity bull market. If you’re a paid member and missed the video, you can see it here.

Commodity markets remain small and undervalued relative to financial assets priced against them, yet they set the cost base for production.

Energy, metals and raw materials feed directly into manufacturing, logistics and construction. We’ve been discussing a new Grey Swan portfolio exclusively aligned with the boom we see coming in 2026 and beyond. Let us know if you’re interested in learning more. Send an email: Feedback@GreySwanFraternity.com.

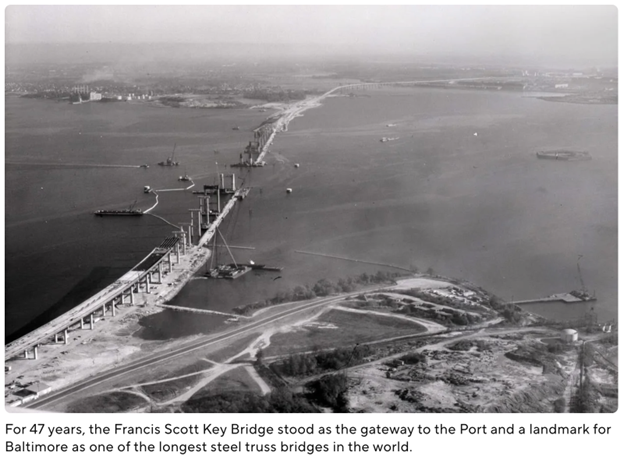

🌉 Baltimore’s Very Own Chokepoint

For 47 years, the Francis Scott Key Bridge carried traffic into the Port of Baltimore.

On March 26, 2024, the Singapore-registered cargo ship Dali lost power and struck one of the bridge’s support piers, sending a construction crew into the Patapsco River.

The bridge sits at the entrance to the Port of Baltimore, a logistics hub that generates roughly $70 billion in annual economic impact and supports tens of thousands of jobs tied to autos, bulk goods and container traffic.

When the bridge collapsed, maritime access was blocked, supply chains along the Eastern Seaboard were disrupted and cargo shifted to already congested ports.

The span carried more than 11 million vehicles annually, including hazardous cargo that cannot pass through tunnels. It connects highways, shipping lanes and industrial supply chains at a single point.

The Key Bridge rebuild is underway. Still.

Demolition is complete, contracts are in place and foundation work and design continue. The replacement — a cable-stayed span — is projected to cost between $4.3 and $5.2 billion and reopen around 2030 after delays and revisions.

And like most infrastructure that is in any way tangential to Washington, D.C. — geographically or otherwise — progress moves at the speed of grift.

~Addison

P.S. If you’re also looking to pack your bags and set off for new horizons, you’re in luck.

Today on Grey Swan Live!, we dove into international real estate with the piece we filmed in Panama. We sat down with Ronan McMahon at The Gathering, hosted by Ronan and our friends at Real Estate Trend Alert (RETA).

RETA members are able to get exclusive discounts on real estate projects in top destinations like Panama, Mexico, Portugal and more.

We’ll be publishing the 2026 RETA Index report with Ronan’s top destinations to buy in 2026, along with the replay.

Ronan and his team will also make their masterclass in international real estate available to paid-up members of the Grey Swan Investment Fraternity.

This masterclass is your complete roadmap to owning overseas in 2026. In six videos, they will take you through everything you need to know, starting right at the beginning.

They aren’t holding anything back. Ronan is sharing all the key lessons he’s learned in two and a half decades of buying and scouting real estate overseas.

After you watch the replay, you can take advantage of a special gift for Grey Swan members to join Real Estate Trend Alert for free … and for life! Details here.