“Your topline piece for October 2024,” writes Pete OC from Melbourne, Australia… followed by“In the bulletin was one of the most underreported but consequential stories in markets: on the long yield going up after the Fed just cut.”

Pete did us “a solid,” as my kids would say, reminding us this morning of our core mission, helping readers manage their money through a morass of social media and political propaganda.

We aim to take a long, hard look at the markets each day. Pete was picking up what we’ve been lying down.

“In the November 2024 bulletin,” Pete continues, “You wrote ‘the end of the globalization trade is hard assets’ and advocated moving money into the real economy ahead of the Great Race for natural resources.

“That was well before tariff issues. You and the team recommended silver, copper, gold, uranium, rare earths and now oil early enough for readers to position ahead of the huge pump in each asset. Also, defense stocks and utilities… and digital assets, too.

“Honestly, bravo on calling the rotation into the real economy. Your work over the last few years is A+…”

Of course, we’re going to republish those kind words, right?

Program note: Back in the fall of 2025, we began backtesting what we call Shadow Stocks – individual stocks that trade wildly on headline news stories, but are not reflected in the major stock indexes.

Some topline successes have produced 172%, 330% and 395% – all in three months or less. Shadow stocks look like a sleeper way to multiply your pile in this midterm year dominated by political news.

We’re not quite ready to release the names of these stocks. But keep your eyes peeled. A major upgrade to your Grey Swan daily emails is on its way! Look for new details as we get our research together… likely, early next week.

Back to today’s headlines…

📈 This Ain’t A “Real” Stock Rally

Stocks opened higher by roughly 3% this morning after headlines confirmed a ceasefire agreement with Iran. The reaction came fast enough to suggest traders had their fingers on the buy button before the ink had even reached an agreement.

If you glanced at a chart without context, you might assume the world had solved geopolitics, inflation and snack food guilt all in a single overnight session.

Margin debt on the Wilshire 5000, the broadest index of US stocks, reached historic highs even as the market topped prior to the missiles flying in Iran. (Source: Yardeni Research)

Margin debt on the Wilshire 5000, the broadest index of US stocks, reached historic highs even as the market topped prior to the missiles flying in Iran. (Source: Yardeni Research)

Here are some gritty mechanics of yesterday’s rally: Large-cap funds entered the week carrying cautious exposure after several sessions of uneven price action. Many had layered that caution on top of debt; a hedge against bad news from the war.

Following the ceasefire announcement, when futures lifted overnight, short positions began to cover aggressively into strength. Then the algos kicked in… adding to long positions as prices rose.

Et voila.

The market was demanding positive news out of the Middle East. The President took the lead in delivering it on Truth Social.

As always, we caution: be careful what you wish for.

📊 Valuations Stretch (Again) With The Rally

Beneath the morning’s enthusiasm, valuation levels remain where they stood before the ceasefire crossed the wires.

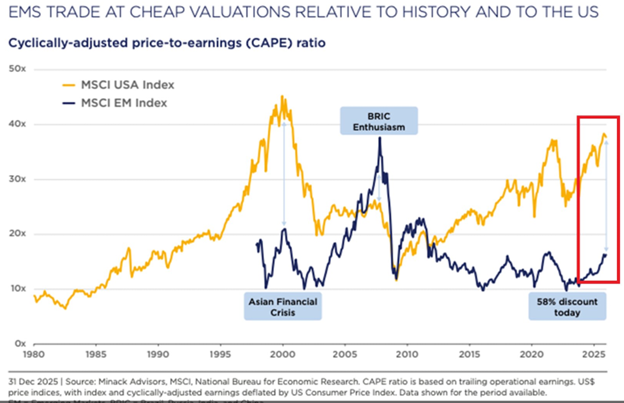

The U.S. MSCI Index trades near a Shiller P/E of approximately 39 times earnings, a level last seen during the late stages of the dot-com cycle when capital chased growth stories ahead of realized cash flow.

The spread between US stocks and their int’l counterparts is roughly sixty percent. The gap has widened over time as capital has favored liquidity, institutional depth and the perceived policy backstop embedded in U.S. markets. (Source: Minack Advisors, MSCI and National Bureau for Economic Research)

The spread between US stocks and their int’l counterparts is roughly sixty percent. The gap has widened over time as capital has favored liquidity, institutional depth and the perceived policy backstop embedded in U.S. markets. (Source: Minack Advisors, MSCI and National Bureau for Economic Research)

Emerging markets, on the other hand, trade closer to 16 times earnings, closer to the historical mean.

No new mega AI earnings revisions accompanied today’s move. Analysts did not publish upgrades ahead of the open, and no material change to forward guidance appeared in the pre-market tape.

The adjustment occurred solely due to market sentiment (euphoria). When multiples expand like this… without a corresponding change in earnings… the difference sits in the expectation that investors are willing to pay for future capital gains only. It’s gambling… not investing.

🌍 Conflict Data Accumulates Outside the Screen

The Iran ceasefire – even if it holds – arrives in a global environment where conflict has been trending in the opposite direction.

According to an IMF report released on X this morning, in 2024, more than 35 countries experienced conflict within their own territory, and roughly 45% of the global population lived in regions affected by some form of warfare.

Since 2010, conflicts have resulted in more than 1.9 million deaths.

These are macro figures and do not respond to a single agreement like the dubious “double-edged” ceasefire Trump lifted markets with yesterday.

Globally, damage accumulates over time, and the conflicts leave their mark in places that do not appear on stock screens.

As we’ve seen in the Gulf conflict, production capacity declines where infrastructure is damaged. Trade routes adjust as risk and insurance premiums increase. Governments divert spending toward military operations first, toward reconstruction later.

When hostilities pause, the next phase begins. Roads, ports and power systems require repair. Governments issue debt or reallocate budgets to fund those projects. Contractors receive payment, materials move and timelines extend. Those flows pass through balance sheets and fiscal accounts over months and years.

You can see from today’s market action that there is a huge disconnect between the ongoing conflicts and the U.S. stock market.

World economies are still actively seeking new leadership, production routes and supply chain alternatives as the Trump Great Reset takes shape.

🇯🇵 Japanese Bonds Lead the Way In A World of Debt

In Japan, the bond market continues to move in a direction that reflects supply, demand and the absence of a buyer that once absorbed both.

The 30-year Japanese government bond yield has reached approximately 3.74 percent, near the highest level since the instrument was introduced in 1999. The 10-year yield trades around 2.4 percent, a level not seen since the late 1990s.

The most recent 30-year auction drew a bid-to-cover ratio of 3.12, weaker than both the prior month and the twelve-month average of 3.36.

Buyers participated, though not with the same appetite that characterized earlier sales when yields were lower and central bank support was more visible.

Japan’s deficit spending continues to unimpeded.

Parliament approved a ¥122 trillion budget for fiscal year 2026, including roughly ¥9 trillion allocated to defense spending. Debt now exceeds 220 percent of GDP, the highest among developed economies.

At the same time, the Bank of Japan has been reducing its holdings as part of quantitative tightening.

With the central bank stepping back, a larger share of issuance must be absorbed by private investors. Those investors require higher yields to compensate for duration risk and inflation uncertainty, reflected in both auction demand and secondary market pricing.

You can bet Treasury Secretary Scott Bessent is au courant, keeping an eye on the Japanese bond market as a harbinger for events to come during the regularly scheduled Treasury auctions. (As we noted this morning, $8 trillion of US debt needs to roll over in 2026 alone. )

In the 1930s, economist Freeman Tilden wrote A World In Debt about the rising level of debt across all major global economies and the depression the debt wraught when the wheels of commerce ground to a halt. Debt levels today, exceed those that concerned Tilden then. (Source: Steve Hanke)

In the 1930s, economist Freeman Tilden wrote A World In Debt about the rising level of debt across all major global economies and the depression the debt wraught when the wheels of commerce ground to a halt. Debt levels today, exceed those that concerned Tilden then. (Source: Steve Hanke)

Economist Steve Hanke dropped this nugget on X this morning: Global debt now stands near $348 trillion, more than three times global GDP.

Within the G7, debt levels have risen from roughly 20% of GDP in the post-war period to over 100% today.

As yields move higher, the cost of servicing that debt rises alongside them, feeding back into fiscal calculations.

🥇 Central Banks Buy The Gold Dip

Yesterday, a reader asked in our Grey Swan Trading Fraternity live session if we’re still bullish on gold. Our simple answer is: yes.

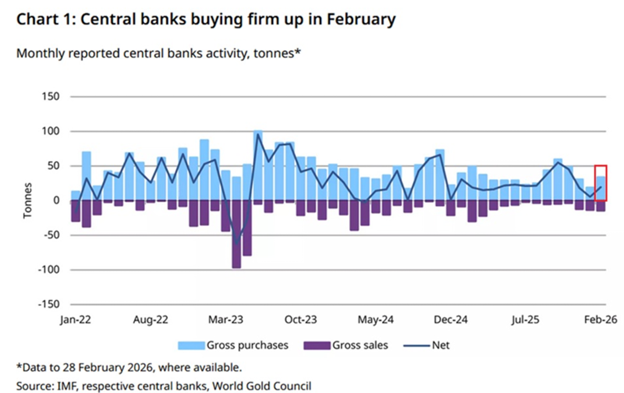

While equity markets respond to headlines and bond markets adjust to supply, central banks continue to accumulate gold through steady reserve allocation. As a group, central banks added approximately 19 tonnes in February, marking the 23rd consecutive month of net purchases.

Leading up to the action in Iran, China added 1 tonne of gold to its reserves, extending a 16-month purchasing streak and bringing its total above 2,300 tonnes, or roughly 10 percent of its reserves. (Source: World Gold Council)

The National Bank of Poland led the activity with a 20-tonne purchase, bringing total reserves to roughly 570 tonnes, or about 31% of its foreign exchange holdings.

Uzbekistan added 8 tonnes, lifting its reserves to approximately 407 tonnes, or about 88% of its total holdings.

On the other side of the ledger, Turkey reduced holdings by 8 tonnes in February and later sold an estimated 120 tonnes in March to fund foreign exchange operations during the Iran conflict. Russia reduced holdings by 6 tonnes over the same period.

These transactions appear in reserve data rather than intraday price movements.

Maybe it’s just us, but acquiring gold at a lower price is still a good idea for your own reserves.

~ Addison

P.S. This week on Grey Swan Live!, we went on camera with Dr. Mark Skousen — and this is exactly the kind of market he thrives in.

With sentiment shifting, volatility cooling and narratives changing by the hour, he joined us to cut through the noise and focus on what’s actually driving prices right now.

Plus, he revealed where the smartest opportunities may be emerging as a result of this chaotic environment.