Through the first 41 trading days of 2026, the S&P 500 traded within a 2.7% range — the narrowest start to any year since 1928. The first 41 days of 2008 spanned roughly 35%. In 2020, the range ran near 15%. Even the placid 1950s never opened this tight.

Global Markets Investor did the heavy lifting on this one:

To put this into context, the 2008 Financial Crisis produced a ~35% range over the same period, 13 times wider, while the 2020 Crisis saw ~15%, or ~450% wider.

Even the quietest decades in market history, including the 1950s, 1960s, and the years leading up to the Financial Crisis, never saw trading in the first 41 days this calm.

This comes despite massive moves beneath the surface. S&P 500 stock dispersion is up to 25 points, the highest on record.

And measures how differently individual stocks are moving versus the overall index. In simple terms, while the overall index appears calm, individual stocks are swinging wildly in different directions, some surging, others plunging.

The last time dispersion was this elevated, markets were in crisis.

Individual stocks swung sharply while the index barely moved. The equal-weight S&P 500 ETF rose 5% year to date. The Magnificent 7 ETF fell 6%.

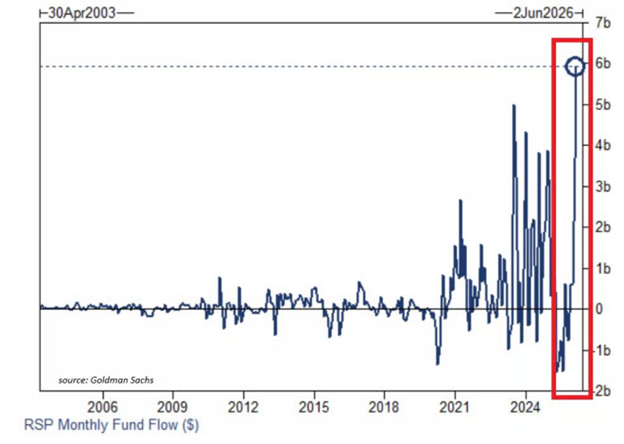

That is a 12.5-point gap in just over two months. February alone pulled $6 billion into equal weight — the largest monthly inflow in its history.

While the index looks sedated, the movement of capital is anything but.

Yesterday on Grey Swan Live!, our friend John Robb described this environment as the textbook formation of a Grey Swan: high impact, structurally plausible, and broadly visible — yet still underappreciated in its systemic consequences. More below.

🛢️ Energy Markets Lose Their Buffer

We’ve been providing details all week: Since the Iran intervention, roughly 20% of global oil flows through the Strait of Hormuz have been disrupted, rerouted, or had insurance withdrawn.

Brent pushed through $92 in trading today… tanker traffic has slowed to minimal, and insurance premiums, those that haven’t been yanked, expanded dramatically. Fuel oil exports through the Gulf collapsed. Asian refiners trimmed output. Shipping detours added time and cost to deliveries between Asia and Europe.

Energy markets once operated with buffers: inventories like the Strategic Oil Reserve, spare shipping capacity, and redundant suppliers.

This week, the slack has thinned.

The strategy and tactics of modern warfare have evolved dramatically in the Russia-Ukraine conflict. Many of the drones flying from Russia into the frontlines and cities across Ukraine have been designed and built by the same Iranian forces who are launching drones by the thousands, targeting 7 of their Gulf neighbors –

Networked conflict — drones, asymmetric strikes, chokepoint pressure — does not require full-scale war to destabilize flows. It only requires the credible threat of disruption.

Markets now price threat persistence, not just physical damage. Insurance premiums rise before tankers are hit. Freight costs jump before inventories run dry. Futures curves steepen on expectation alone.

That reflexive repricing is what Robb calls systemic fragility: tightly coupled networks reacting to small shocks with outsized moves.

What we’re seeing has moved beyond media headlines to infrastructure and trade network stress.

From Robb’s perspective, there’s more mayhem to come. A lot more. We encourage you to watch the replay of yesterday’s Grey Swan Live! with John Robb, details below.

We’re already following up with Robb’s advice. In the Grey Swan Trading Fraternity this morning, Andrew Packer issued a trade to get long oil prices. Since then, oil is on the move, up another $4, touching $92 per barrel for the first time in over four years.

🏦 The Fed’s Narrow Corridor

The BLS jobs report came out this morning at 8:30 am. The report itself caused a stir across the financial press.

February payrolls fell by 92,000; a surprise after January printed strong.

No single month determines Fed policy, but the labor market remains low-hiring, low-firing, steady, and vulnerable.

This week’s spike in oil prices from $65 to $92 complicates the Fed’s dual mandate. If… when… oil remains elevated, consumer spending will absorb the hit. If consumers pull back, growth slows.

Lather, rinse, repeat.

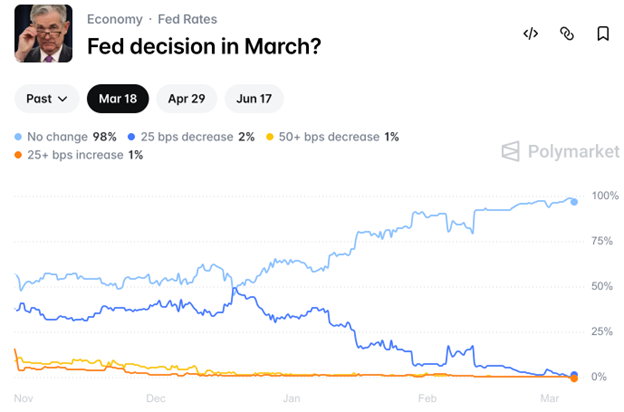

The Fed, awaiting its new chairman, now balances inflationary pressure from energy with softness in the hiring data. Still, Polymarket puts the odds .25 rate cut on March 18 at less than 1%. (Source: Polymarket)

🌍 Capital Still Prefers Liquidity

Earlier this week, the dollar index rallied sharply as foreign capital sought U.S. liquidity during global stress. Frontier markets sold off. Developed markets showed strain.

When flows tighten in frontier markets, the money fled toward depth and settlement reliability.

The equal-weight S&P 500 ETF, $RSP, attracted +$6billion in February 2026, the highest monthly figure in its history. (Source: Global Markets Investor and Goldman Sachs)

The shift back into U.S. markets occurred at the fastest pace since 2008.

As our opening salvo today reveals, despite very little movement in the topline indexes, volatility has hardly been eliminated.

But the money isn’t flowing everywhere. Private credit – which we’ve covered for over 18 months and more extensively this week – continues to show strain.

This morning, BlackRock capped the total redemptions in their private credit fund, effectively holding $26 billion in capital hostage.

That comes a day after BlackRock wrote down a $20 million private credit deal to zero. Not a fifty-cent-on-the-dollar haircut – a total loss.

Regional bank Western Alliance is suing Jefferies bank over the nonpayment of $126 million tied to loans to FirstBrands, one of the, ahem, first companies to reveal the cracks in private credit.

Time will tell – and soon – which cracks the market first: Iran, or the credit markets.

🔌 Dollar 2.0 Plumbing

We close this week where we began regarding the Clarity Act.

The regulatory environment that will eventually pave the way for a huge flow of capital into the digital space will have to wait another week for any meaningful announcement from legislators. CoinDesk released this video to help clarify what the freakin’ hold up in the Senate is:

The Clarity Act remains stalled in the Senate over stablecoin yield provisions. Banks lobby against yield-bearing stablecoins. And so on, ad infinitum (Source: CoinDesk).

The Clarity Act remains stalled in the Senate over stablecoin yield provisions. Banks lobby against yield-bearing stablecoins. And so on, ad infinitum (Source: CoinDesk).

On Tuesday, Trump posted on Truth Social that he and the White House team want the act on his desk before summer.

While the statute lingers, Kraken’s banking subsidiary has received a Federal Reserve master account from the Kansas City Fed, granting it direct access to Fedwire.

Crypto infrastructure now connects to sovereign payment rails. That’s a big deal.

In short, while “K-Street Violence” continues, the plumbing moves forward. We’re keeping a close eye on this one and our recommendations from the Dollar 2.0 research posted in the Grey Swan member library.

🧭 Where the Grey Swan Forms

Let’s recap a busy week in a speed round: Record dispersion. Record-tight index range. Energy flows disrupted. Insurance withdrawn. Shipping rerouted. Oil elevated. Payroll volatility. Legislative delay. Digital rails expanding.

Robb’s definition fits: a visible, high-impact development that reshapes systems while most participants treat it as temporary.

A Grey Swan does not arrive with sirens. It builds through pressure points. It reveals fragility already embedded in networks — energy, finance, logistics.

When a river looks flat from the bank, that’s usually where the current runs fastest underneath. Don’t argue with the river. Watch the eddies, keep your balance and mind your footing.

Hyman Minsky, eat your instability heart out.

— Addison

P.S. There aren’t too many conversations we have that will shake your worldview and make you rethink your assumptions about the market and the economy. Yesterday’s Grey Swan Live! with John Robb, author of Brave New War and a Grey Swan Investment Fraternity contributor, did just that.

John’s analysis of the U.S. military strikes in Iran and their strategic decision to decapitate the Iranian regime is fraught with unknown unknowns we hadn’t yet considered. That’s the value of having a former advisor to the Joint Chiefs of Staff on kinetic network warfare in the fraternity.

The conversation sent Andrew and I into the futures markets looking for ways to isolate portfolio risks should the U.S. and Israeli bombardments fail to restrain a decentralized and highly motivated, mobile Iranian drone network.

Passage of oil and natural gas through the Strait of Hormuz has been paralyzed for an indeterminate period, and the longer prices rise, the more insatiable global financial markets and the U.S. domestic economy will become.

John covered the strategy employed against Iran, its impact on neighboring countries, and what it means for the dollar and other assets. His analysis was shocking and sobering:

Robb’s expertise on network warfare is central to understanding the Trump strategy for killing 40 top Iranian leaders and what’s likely to happen next. The methods, technology and strategy of open warfare have changed dramatically since the Russian invasion of Ukraine in 2020.

If you were unable to attend, it’s worth your time to click on the replay. We’ll have the video up on site later today for members. If you’re not yet a member, click here to sign up and join the fraternity today so you can get caught up on the war and the longer-term implications as the missiles and headlines currently fly.