“Should I buy gold at this price?” The question comes with the regularity of Metamucil and promise.

The answer:

“Well, yes.”

Not to be flippant, but the answer is “yes.” Although perhaps not for the reasons dominating financial media. We’re going to get to the three specific reasons why gold is a good buy at this price in just a minute. First, a few programming notes for you:

- The financial press, online, on TV and on social media, is pining for details on the US-Iran peace deal. None have been released. But commodities traders, anticipating Friday’s planned signing ceremony, have knocked the price Americans pay for oil (WTI Crude) down to $72 bucks a barrel this morning.

We’re going to dig into the market reaction and forecast of our own on the Grey Swan Trading Fraternity live podcast tomorrow, Wednesday, June 17, 2026 @ 3 p.m. EST/12 p.m. PST. If you’re a trader, you’ll want to tune into the adjustments Andrew is making, assuming the peace deal sticks.

2. Tomorrow, June 17, 2026, we’ll also hear the first comments from new Federal Reserve Chairman Kevin Warsh.

According to a Wall Street Journal expose, presumably published with Warsh’s approval, the first thing we should expect from a Warsh Fed is… nothing. No rate change. And an adamant belief Warsh has that the Fed should stop overexplaining its every move.

During the press conference tomorrow, Warsh is slated to articulate the fundamental changes he’s going to mandate under his tenure. We’re looking forward to it, frankly, and hope Warsh is bold enough to articulate his more radical plans right out of the gate. We’re going to tackle the specifics of those ideas in tomorrow’s Dive. Look for them tomorrow.

3. Last Friday, the U.S. government banned foreign actors from using Anthropic’s Mythos and Fable 5 platforms — the most powerful AI systems ever created.

Now, there are growing signs that it may be preparing to bring that technology under its control.

This Thursday at 2 p.m. ET/11 p.m. PST, Ian King joins us on Grey Swan Live! to discuss Mythos, the AI arms race, and why control of artificial intelligence may become the defining political and economic issue of the next decade.

We’ll also connect the dots between:

- The growing push for AI dominance.

- The future of the Clarity Act.

- Dollar 2.0 and the tokenization of financial markets.

And why crypto may be far more important than current prices suggest.

The headlines are focused on AI stocks.

We’re more interested in who controls the infrastructure of the future. And how ownership will impact the Great Race.

We’ll get to all of those critical infrastructure ideas with Ian on Thursday. These questions are more critical to your money than you may realize. Certainly more than SpaceX’s current valuation now that it’s trading live. Don’t miss Grey Swan Live! at 2 p.m. on Thursday.

Now, on to the question we’ve been getting in all our communications lately:

🥇 Should You Buy Gold At This Price?

Gold’s spectacular run over the last three years has created the impression that the easy money has already been made. Bullion doubled in price as inflation surged, central banks accumulated reserves at a historic pace, and investors sought protection from geopolitical instability. This year’s correction has understandably raised questions about whether the trade has run its course.

We don’t think so.

Three factors continue to support a constructive long-term outlook for gold: central bank buying, persistent federal deficits and the ongoing expansion of the U.S. money supply.

None are particularly exciting.

None involve a celebrity CEO launching a rocket, unveiling a humanoid robot or promising to replace your accountant with artificial intelligence. But unlike the market’s latest fascinations, these three forces have a habit of sticking around long after the headlines move on.

And because gold is still priced in dollars on the global market, all three continue to matter.

🏦 Central Banks Continue to Accumulate

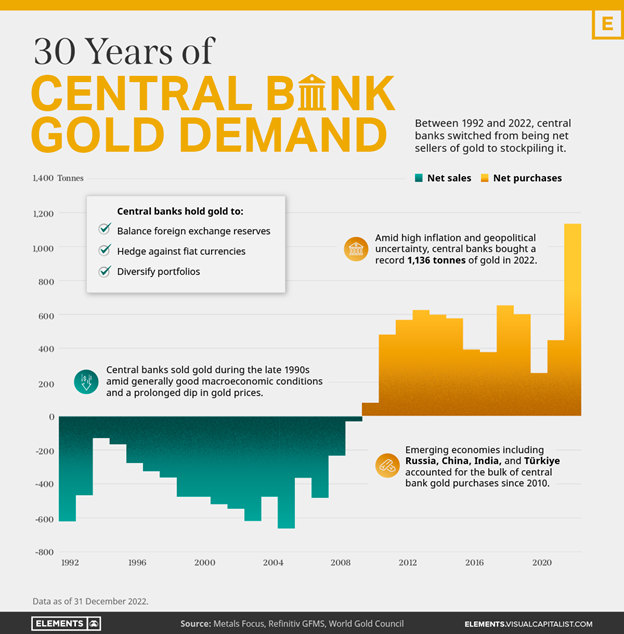

The most important development in the gold market over the past several years has not been retail investor demand or exchange-traded funds. It has been the steady accumulation of gold by central banks.

The implementation of Basel III, passed in 2023 and implemented in July 2025, gives gold the same tier-one liquidity status as the U.S. dollar and U.S. treasuries. That makes gold more attractive to central banks seeking to hold reserves outside the U.S. dollar.

According to a recent survey by the World Gold Council and YouGov, 45% of central banks expect to increase their gold reserves over the next 12 months. That is the highest reading recorded since the survey began in 2018. Only one central bank reported plans to reduce its holdings.

For the third straight year, central banks are buying gold at a historic pace, with nations from Asia to the Middle East steadily increasing their reserves as they seek protection from geopolitical tensions, inflation, and dependence on the U.S. dollar. (Source: Visual Capitalist)

The significance is not simply that central banks are buying. It is that they continue to buy after gold has already experienced one of the strongest advances in modern history.

Normally, buyers become scarce after prices double. Wall Street’s favorite strategy is to show up late to the party, spill a drink on the carpet and declare itself a genius. Central banks, by contrast, tend to think in decades rather than quarters. They aren’t trying to beat next month’s earnings estimates. They are trying to protect national reserves against a world that appears to be growing less predictable by the year.

Many central banks appear to view this year’s pullback not as a warning sign but as an opportunity. Shaokai Fan of the World Gold Council noted that several institutions delayed purchases during 2025 because they considered the market too expensive. The recent decline appears to have changed that calculation.

The demand is particularly concentrated among emerging and developing economies. More than half of central banks expect to increase reserves over the coming year, compared with less than one-fifth in advanced economies.

For investors, the implication is straightforward. When some of the largest and most patient buyers in the world continue accumulating an asset after it has already doubled in price, it pays to pay attention. Central banks are not perfect market timers. But neither are they known for impulse purchases.

📉 The Federal Deficit Keeps Growing

The second factor is fiscal policy, which is a polite way of saying Washington continues to spend money like a teenager who just discovered Dad’s credit card.

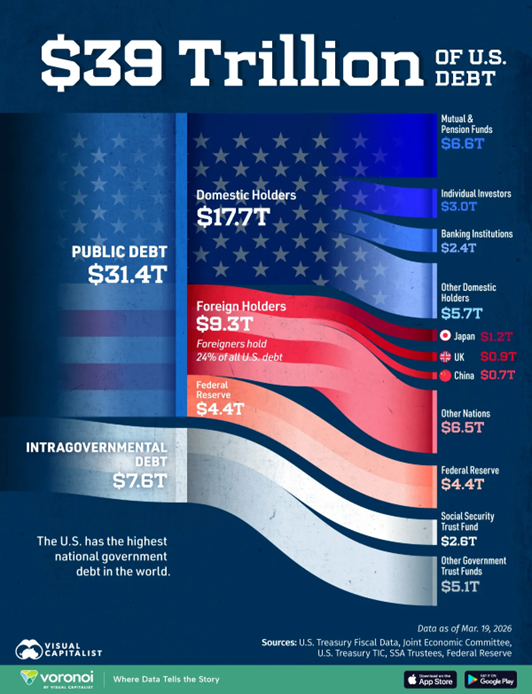

The federal government is expected to run a deficit of approximately $2 trillion in fiscal year 2026. In nominal dollar terms, that would rank as the third-largest annual deficit in American history, trailing only the extraordinary spending associated with the pandemic years of 2020 and 2021.

Viewed relative to the size of the economy, the projected deficit equals roughly 5.8% of GDP. That is well above the historical average and remarkably large considering the country is not mobilizing for World War III, rescuing the banking system or mailing stimulus checks to every household with a mailbox.

America’s national debt has climbed past $39 trillion, raising concerns about long-term fiscal sustainability and increasing the likelihood that future governments will face difficult choices between higher taxes, reduced spending, or larger deficits. (Source: Visual Capitalist)

The composition of the deficit is perhaps even more important than the headline number. Increasingly, spending growth is being driven by structural obligations rather than temporary emergency programs.

Interest payments on the national debt continue to rise as Treasury securities issued during the era of near-zero interest rates mature and are refinanced at much higher yields. At the same time, demographic realities are pushing spending on Social Security and Medicare steadily upward as the population ages.

In other words, the deficit is beginning to resemble a snowball rolling downhill. Every rotation makes it larger, and every year makes it harder to stop.

These are not expenses that policymakers can easily trim around the edges. They are embedded in the federal budget itself.

Investors often debate whether deficits are inflationary in a given year. A more useful question may be whether Washington appears capable of reversing the trend. Judging by recent behavior, Congress treats budget restraint the way a Labrador retriever treats a squirrel: everyone talks about it until something more interesting runs by.

As long as annual deficits remain measured in trillions rather than billions, the supply of Treasury debt continues to expand. Gold has historically performed best when confidence in fiscal discipline begins to erode. A projected $2 trillion deficit suggests there is still plenty of erosion left.

💵 Money Supply Is Still Growing

The third factor is less dramatic than the deficit but arguably more important.

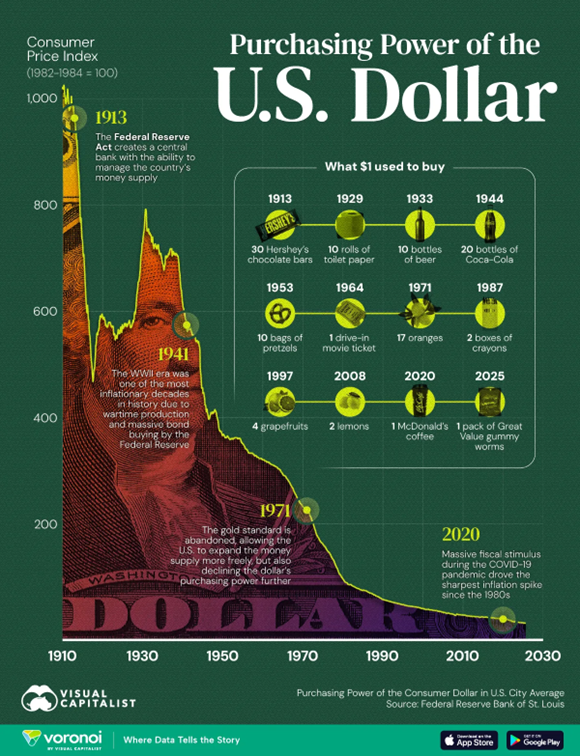

The U.S. M2 money supply currently stands near $22.8 trillion and is expanding at an annual rate of approximately 4.7%.

That pace is lower than the long-term average growth rate of roughly 6.8%, but it remains positive. More dollars exist today than existed a year ago. More will likely exist a year from now.

The extraordinary surge in money supply during the pandemic years understandably captured public attention. M2 expanded by more than 26% year-over-year during 2021, a monetary event that landed on the economy with all the subtlety of a piano falling from a fifth-story window.

The inflation that followed surprised many economists. It surprised fewer people who had spent even a passing amount of time reading monetary history.

The U.S. dollar remains the world’s dominant currency, but decades of inflation mean each dollar buys significantly less than it once did, steadily eroding purchasing power and making alternative assets like gold increasingly attractive stores of value. (Source: Visual Capitalist)

What is often overlooked is that money supply growth did not disappear after inflation cooled. It simply returned to a more familiar pace.

An economy built on credit and expanding output generally requires an expanding money supply. That is not controversial. The system is designed that way. Like a shark that must keep swimming, the modern financial system requires a continual flow of new credit and new liquidity to maintain forward motion.

The important point for gold investors is that the process continues.

Because gold trades globally in dollars, the long-term value of gold remains tied to the long-term supply of dollars. The relationship is not precise from month to month. Markets are too emotional, too political and too distracted for that. But over longer periods, the arithmetic tends to reassert itself.

Gold miners can discover new deposits. They cannot manufacture twenty-six percent more gold in a single year because policymakers decide the economy requires additional stimulus.

That distinction matters.

🚀 Looking Beyond the Current Market

The market’s attention today is focused elsewhere.

The glam stock SpaceX’s public debut has captured investors’ imaginations. Artificial intelligence companies continue to command eye-watering valuations. Semiconductor stocks have experienced a historic run that would make even veteran technology investors reach for the smelling salts.

As a result, capital has flowed aggressively toward growth stories and away from precious metals, miners and natural-resource companies.

It’s not our first rodeo, though, is it?

Late in a cycle, markets tend to crowd into whatever worked yesterday. They chase momentum the way tourists chase the last empty lounge chair by the hotel pool. For a while, it works beautifully. Then everyone discovers they have been standing in the same line.

Meanwhile, gold sits quietly in the corner, ignored and unfashionable, much like the boring uncle who spends the family reunion warning about debt and leverage. Eventually, someone checks his track record and realizes he was the only sober person in the room.

The forces supporting gold today are not speculative narratives. They are measurable trends. Central banks continue to add reserves. The federal government continues to borrow on a historic scale. The money supply continues to expand from already elevated levels.

Because gold remains priced in dollars on the global market, all three remain relevant.

And all three continue moving in the same direction.

That’s why we remain bullish on gold—not because of what happened last month, but because the forces underneath the market continue to work like tectonic plates. You don’t notice them moving on a Tuesday afternoon. Then one day, you look up and realize the landscape has changed.

~ Addison

P.S. The companies making headlines today may not be the biggest winners tomorrow. The entities controlling the underlying infrastructure could be.

Last week’s restrictions on foreign access to Anthropic’s most advanced AI systems may prove to be more than a national security decision — they could be an early sign that governments are beginning to treat artificial intelligence as strategic infrastructure.

Tune in this Thursday at 2 p.m. ET on Grey Swan Live! as Ian King joins us to explore what that means for AI, crypto, financial markets and the next phase of technological competition.

Markets have spent months whipsawing on every headline out of the Middle East, but this week’s U.S-Iran ceasefire announcement could mark a genuine turning point.

If tensions continue to ease, lower energy prices, declining volatility and improving investor sentiment could provide a powerful tailwind for stocks in the second half of 2026.

So, on Grey Swan Trading Fraternity tomorrow at 3 p.m., we’ll break down the sectors, trends, and opportunities that stand to benefit most if peace proves more durable than the market expects.