Last night, President Donald Trump announced a ceasefire agreement with Iran. It’s the 38th time, mind you, he’s said a deal is coming. But still. With Kevin Warsh about to chair his first FOMC meeting tomorrow, the timing couldn’t be more auspicious. Let’s take a look.

By the time most Americans poured their first cup of coffee this morning, shipping companies, tanker operators, insurance underwriters and energy traders had already begun repricing risk. A missile fired near the Strait of Hormuz travels only a few miles. The financial consequences often travel much farther.

Roughly one-fifth of the world’s petroleum consumption passes through that narrow waterway. Every refinery manager in Asia knows it. Every sovereign wealth fund in the Gulf knows it. Every central banker worried about inflation knows it.

When crude oil moves freely through Hormuz, planners can make assumptions about energy costs six months from now. When missiles start flying, those assumptions begin to look like fiction.

The timing is difficult to ignore.

On November 18, 2025, Trump shook hands with Saudi Arabia’s Crown Prince Mohammed bin Salman on the White House veranda. During a press conference following the men’s announcement, agreements involving defense cooperation, artificial-intelligence infrastructure, semiconductor technology, critical minerals and investment commitments approaching $1 trillion were announced. The mainstream press naturally focused on the trillion-dollar headline. Investors paid closer attention to the project list.

Saudi officials arrived to discuss data centers. They arrived talking about electrical generation. They arrived talking about advanced manufacturing, semiconductor fabrication and artificial intelligence. The kingdom that spent decades financing its future with crude oil revenues was discussing the need for enough electricity to power a digital economy.

🛢️From Origin of the Petrodollar…

William Simon would have recognized part of the conversation.

In 1974, Treasury Secretary Simon traveled to Saudi Arabia with a proposal to stabilize the dollar, following Richard Nixon’s closure of the gold window three years earlier. The kingdom would continue selling oil in dollars. Saudi revenues would move through American financial markets. The United States would provide security guarantees.

The arrangement emerged during a decade when inflation was surging, energy markets were unstable and confidence in the monetary system had been shaken. Saudi Arabia gained security. Washington gained something equally valuable: a steady stream of dollar-denominated oil revenues moving through American financial markets.

Half a century later, Mohammed bin Salman arrived, discussing investments measured in hundreds of billions rather than millions. The meetings still involved security. They still involved capital. They still involved the dollar. But the conversation had expanded from oil fields and pipelines to semiconductor fabs, transmission lines, data centers and artificial-intelligence infrastructure.

The executives planning those projects are not making quarterly decisions. They are making decade-long commitments. They are negotiating power contracts, supply agreements and construction schedules that stretch beyond election cycles and news cycles alike.

That is why last night’s ceasefire matters. Not because politicians announced it. But because trillions in capital have been sidelined, waiting for it.

💵 Through The Triffin Dilemma…

The U.S. dollar, as the reserve currency of the Western financial system, has been a defining feature of the post-War Pax Americana.

In 1960, Belgian economist Robert Triffin appeared before Congress to warn about the very system Simon would later help reinforce. In what the IMF would famously dub “Triffin’s Dilemma,” the dollar reserve system has an Achilles heel.

The world needed dollars.

European governments needed them. Asian governments needed them. Commercial banks needed them. Commodity traders needed them. Every expansion of global trade required additional liquidity. If the dollar remained the world’s reserve currency, the United States would have to keep supplying those dollars.

The dollars would leave the country through trade, investment and military spending. Foreign governments would accumulate them. Foreign institutions would accumulate them. Eventually, all of those dollars would need somewhere to go.

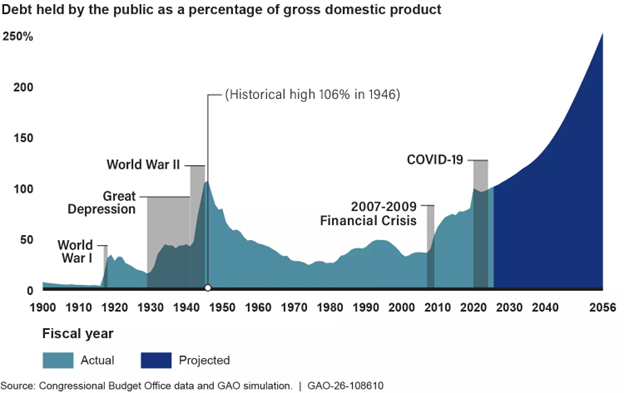

When Triffin testified, federal debt stood below $300 billion. Today, it approaches $40 trillion. Rapidly.

Federal debt continues to push higher, adding pressure to an already stretched fiscal outlook. With spending running ahead of revenues, more of the budget is being absorbed by interest costs, leaving less flexibility for everything else. The longer the imbalance persists, the harder it becomes to correct without sharper tradeoffs down the line. (Source: U.S. Government Accountability Office)

For decades, reserve managers, exporters and sovereign funds solved the same problem the same way. They purchased Treasury securities. Japanese exporters accumulated dollars and purchased Treasury securities. European financial institutions accumulated dollars and purchased Treasury securities. Oil exporters accumulated dollars and purchased Treasury securities.

The Treasury market became the place where global dollar balances settled.

Along the way, those purchases financed interstate highways, aircraft carriers, tax cuts, stimulus programs, financial rescues and a long list of promises made by politicians who have long since left office.

The debt accumulated slowly at first. Then quickly.

In Trump’s second term, it’s all at once. No small thanks to the Iran conflict and what is shaping up to be the United States’ 2nd-largest deficit in history, by total dollars spent and by percentage of gross domestic product (GDP).

🥇 To A New Slate of Global Gold Buyers

When Russian tanks crossed into Ukraine in February 2022, the United States and its allies froze a substantial portion of Russia’s foreign reserves.

Officials in Washington viewed the move as a sanctions tool. Non-Western allied reserve managers elsewhere saw something different. They saw a reserve asset become unavailable. And a banking system vulnerable to political objectives.

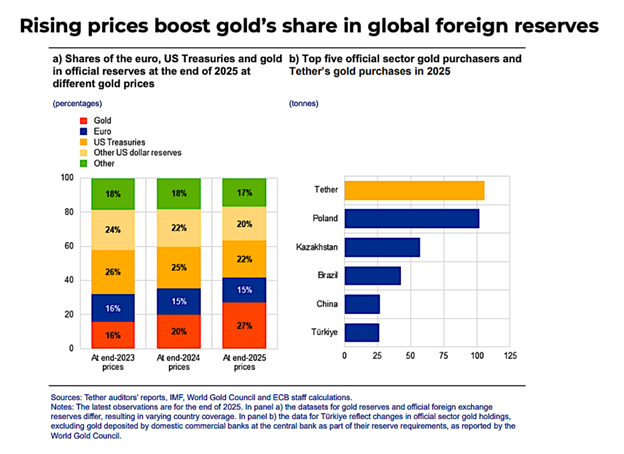

Within a few years, China increased its gold holdings. Poland increased gold holdings. India increased its gold holdings. Kazakhstan increased its gold holdings. Central-bank vaults began filling at a pace not seen in decades.

By early 2026, official gold reserves reached roughly $4 trillion, slightly exceeding official holdings of U.S. Treasury securities. The purchases continued even after gold crossed $5,000 an ounce.

Central banks are steadily adding to gold reserves, signaling a continued shift toward hard assets amid currency volatility and geopolitical risk. The sustained buying trend underscores gold’s role as a strategic hedge rather than a short-term trade. (Source: European Central Bank)

Mark Hulbert highlighted another oddity last week. Gold has fallen sharply during the Iran conflict despite decades of conventional wisdom suggesting geopolitical turmoil should support bullion prices.

Using data compiled by economists Dario Caldara and Matteo Iacoviello, Hulbert found no stable relationship between geopolitical stress and gold prices over rolling five-year periods dating back to 1968.

“Gold instead marches to its own drummer,” he wrote.

Campbell Harvey of Duke University and former commodity-fund manager Claude Erb arrived at a similar conclusion in their study Golden Dilemma. Over periods measured in generations, gold appears remarkably effective at preserving purchasing power. Over periods measured in market cycles, it behaves with considerably less regard for investor expectations.

The reserve managers buying bullion seem comfortable with that distinction.

⚙️ And Scott Bessent’s New Dollar and Treasury Buyers…

While central banks were adding gold, Treasury Secretary Scott Bessent spent much of the past year talking about Treasury demand.

Not from foreign governments. Not from pension funds. Not from traditional banks. From “Dollar 2.0” stablecoins and a global marketplace that can expand 24/7 instantly and far more efficiently than ever before.

A saver in Buenos Aires purchases a dollar-backed stablecoin. The issuer acquires Treasury bills. A saver in Lagos purchases a dollar-backed stablecoin. The issuer acquires Treasury bills. A software developer in Singapore writes code. A reserve account in the United States accumulates additional Treasury securities.

The mechanics would have sounded bizarre to the officials who negotiated the original petrodollar arrangements. The Treasury does not particularly care where the demand originates. The securities just need a market, also not susceptible to political ambition.

🏦 Tomorrow Belongs To Kevin Warsh

Tomorrow, Kevin Warsh walks into his first Federal Open Market Committee meeting as chairman.

He arrives after a weekend in which traders (including our own) have perused and debated his old speeches, Treasury officials have prepared another round of borrowing, central banks have continued adding gold to their reserves, and stablecoin issuers have quietly accumulated more Treasury bills.

When Paul Volcker took over the Federal Reserve in 1979, inflation was running wild and interest rates were climbing toward levels that would be unthinkable today.

When Ben Bernanke took over in 2006, mortgage lenders were handing out loans with extraordinary enthusiasm while Wall Street transformed those loans into securities carrying investment-grade ratings.

Kevin Warsh has consistently argued for a Fed that is more disciplined on inflation, more transparent in communication, and less reliant on crisis-era tools. His vision for the chair role centers on restoring credibility through tighter policy restraint when needed and a clearer exit from emergency interventions, even if that means tolerating slower growth in the short term. (Source: Getty Images)

Warsh inherits a different challenge. When Robert Triffin testified before Congress when federal debt stood below $300 billion. Tomorrow, Kevin Warsh chairs his first FOMC meeting with federal debt approaching $40 trillion.

While the numbers have grown substantially, the questions have not changed. We’re holding out for Warsh to enter his new post with a bang. More details on the possibilities tomorrow. Stay tuned…

📜 Eight Hundred Eleven Years Ago Today

As we wend our way toward the July 4th 250-year anniversary celebration for these United States, it’s worth keeping one eye on when and where this peculiar idea that a well-educated people could successfully govern themselves.

On June 15, 1215, King John met a group of rebellious barons at Runnymede and placed his seal on a document that became known as Magna Carta.

The king had spent years financing military campaigns that produced disappointing results and mounting expenses. The treasury was depleted. Relations with powerful landowners had deteriorated. The men financing the kingdom arrived carrying grievances, demands and enough military support to force a negotiation.

Many of Magna Carta’s provisions dealt with taxation, debts, property rights, merchants and legal process. The document eventually became associated with liberty, constitutional government and the rule of law. The men gathered at Runnymede were dealing with a more immediate concern: money.

King John appealed to Pope Innocent III within months, asking him to invalidate the agreement.

The Pope obliged. Civil war resumed. The king died the following year.

Yet, the document survived.

Eight centuries later, governments still borrow, creditors still negotiate and investors still spend considerable time trying to determine whether the people making promises today will be able to keep them tomorrow. But so far, so good, yeah? At least for this particular experiment in time and place…

~ Addison

P.S. The IPO is over, but the capital spending cycle is just getting started.

Adam O’Dell follows the money moving into AI infrastructure, electrical generation, transmission buildouts, hard assets, mining, energy bottlenecks and the next phase of The Great Race as investors look beyond the most anticipated public offering in history.

And if you missed last week’s Grey Swan Live!, be sure to catch the replay with Adam: What Comes After SpaceX?

The IPO may dominate headlines, but the larger story involves where capital flows next. Adam explores the AI buildout, energy bottlenecks, hard assets, infrastructure spending and the next phase of The Great Race as investors search for opportunities beyond the most anticipated public offering in history.