Yesterday, President Donald Trump brought out his greatest weapon yet – Treasury Secretary Scott Bessent.

Speaking after the market close, Bessent noted that the U.S. economy could see an inflationary blip from the spike in oil prices, but that growth would resume at 3% or better.

That was the shot. The chaser? This morning’s GDP data for Q4 2025, which was cut to 0.7% – a 50% haircut from the initial 1.4% read.

One can’t help but be reminded of January 2008, when Federal Reserve Chairman Ben Bernanke stated that he didn’t see the possibility of a recession on the horizon.

This is the same Bessent who suggested that the U.S. might short oil futures to keep prices down just a week ago.

Sure, that works in financial markets. The heavy hand of government can do a lot of things. But the invisible hand of economics will eventually smack the government around.

Yes, the Fed can print as much currency as it wants. The Treasury can short oil futures if it thinks that will do something.

But money is ultimately a medium of exchange, not an end in itself. You can’t print a barrel of oil. Or food. Or housing.

Ultimately, there’s only so much that the Fed and Treasury can do about real-world assets. And it may be able to influence prices in the short term, but its impact won’t ever last long.

The Chicago Mercantile Exchange (CME) noted that this type of intervention would – and I’m using their exact words here – be a “biblical disaster.”

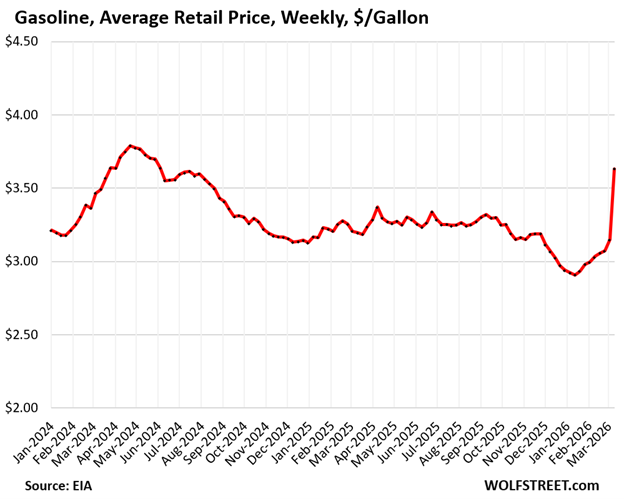

This week’s jawboning about oil and releasing reserves has proven short-lived, with oil back near $100 at Thursday’s close.

Goldman Sachs estimates that the Strait of Hormuz will be closed for at least 21 days, which will likely keep oil prices elevated, and the stock market stuck in neutral.

Until that changes, that’s a lot of oil sitting around in the Middle East not making it to its final destination.

And the longer that takes, the longer prices remain high and the more ever-sticky inflation weighs on Main Street.

For all the attention I’ve brought to today’s challenges in private credit, it pales in comparison to what $100-plus oil for a sustained period of time can do for the economy.

Traders are already scaling back their views of how often the Fed will cut rates this year – to one quarter-point cut in December. That’s despite Trump pushing Federal Reserve Chairman Jerome Powell for an emergency rate cut now – the kind of move that would put real panic into markets.

Don’t Call It the S-Word

That brings us to Truflation. That’s the website that aggregates price data across thousands of goods and services in real time.

Earlier this year, Truflation suggested that U.S. inflation was a scant 0.6%, well below the 2.5% range reported by government statistics.

However, with recent events, Truflation has shot up to nearly 1.1%, double its lows from last month:

And with oil prices rising, everything tied to oil – shipping of all goods and services, anything that uses fertilizer or plastic – is likely to see increased inflationary pressure.

Combined with a slowing labor market, we have conditions in place for 1970’s-style high inflation and a slow economy.

In the 1970s, it was called stagflation. We have no doubt someone such as Bessent will find a better term to use today.

And it also kicked off during a period when turmoil in the Middle East sent oil prices soaring.

Gorged on Dip

Yesterday’s market action signals a possible new phase in today’s markets. Stocks opened lower, then continued lower – and even closed near their lows of the day.

The audacity!

Retail investors appear to have forgotten to buy the dip. Or maybe they’re just running low on funds.

Data from Robinhood show that total wealth on its platform declined about 4.5% in February, compared to a 0.9% loss in the S&P 500 Index.

Part of that may be from the company’s users, whose younger demographic is more interested in a full tech-stock YOLO portfolio.

Or it may simply be that after buying every 1% down day that comes along, retail investors have tapped out.

If you’re patient, you can buy stocks around the 200-day moving average about once every 12 to 18 months. That’s a big, tasty dip worth buying. We had one last April.

But the good news is, we may get our next one soon.

With the stock market flatlining over the past three months, the 20- and 50-day moving averages are now curling lower. And the 200-day moving average is around 6,500 on the S&P 500. That’s where the smart money will start to rotate back in.

💰Big Tech Is 100% In On AI

While markets have been lagging, it hasn’t been because of earnings. They’ve been spectacular for the fourth-quarter of 2025. But it’ll be a new earnings season before you know it.

The biggest challenge? Keeping the party going in stocks. Today’s AI buildout has most Big Tech companies spending more than 100% of their cash flow on AI projects.

That doesn’t leave much money left for things like dividends or share buybacks, which used to provide investors with some price cushion.

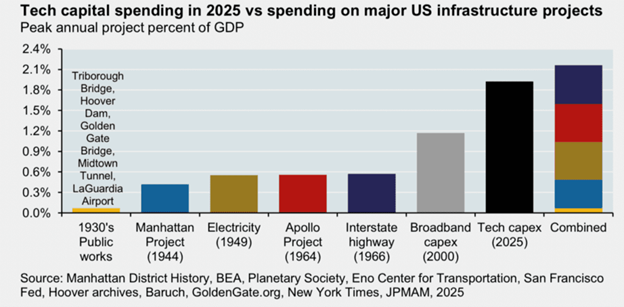

Even worse, today’s level of AI spending, as a percentage of GDP, is larger than the broadband buildout in the year 2000.

We did eventually get broadband. But the capex spending on broadband in 2000 may have also been the straw that broke the ‘90s dot-com boom.

In short, energy markets are reenacting the oil shocks of the 1970s. AI spending is bigger than the dot-com boom – in real and nominal terms – and investors may be running out of capital to buy the dip.

I swear I’m an optimistic guy. But I’m also going to be stingy about stocks until we hit the 200-day moving average. And even then, with everything going on in the world, that’s no guarantee of an immediate rebound to new all-time highs.

That will most likely come after the election – meaning we still have six months of grind ahead.

~ Andrew

P.S. Today, Addison is at The Gathering, a group of investors in an international real estate project led by Grey Swan friend and associate Ronan McMahon and his team at Real Estate Trend Alert.

The five-star Santa Maria hotel and resort, where Addison is networking to find the best deals for Grey Swan members.

Addison is getting a more in-depth look at some of the latest deals in Panama and beyond.

He’ll be recording a special Grey Swan Live! on scene in Panama City. We’ll let our paid-up fraternity members know once Addison reports in and the video is up on site. Learn more here…