The Federal Reserve held rates unchanged for a third straight meeting yesterday. The decision came in at 8-4, the most divided vote at the Fed in 34 years, and it marked Jerome Powell’s final meeting as chair before his term ends May 15.

Powell added another twist to the Trump-Powell drama.

The chairman announced he will remain on the Board of Governors after stepping down as chair, something no Fed chair has done since 1948.

Perhaps wisely, Powell tied that decision to recent legal pressure on the institution, including the recently shuttered Justice Department probe into cost overruns at the Fed HQ building and allegations that they lied to Congress about them.

Powell assured the press that he will keep a low profile and support the incoming chair. Kevin Warsh waits on a full Senate vote after clearing the Banking Committee.

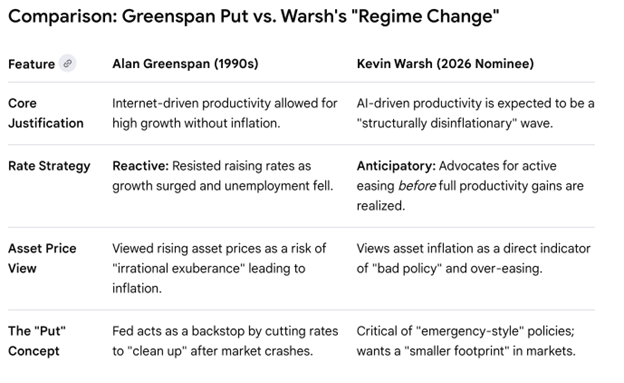

🧠 Warsh Channels Greenspan Circa 1996 to 1997

In the mid to late 1990s, then Fed chair Alan Greenspan kept rates lower than most economists and board governors expected because, he argued, technology goosed productivity and was inherently deflationary.

Unemployment fell. Growth accelerated. Inflation stayed contained long enough for the expansion to run. The so-called “Greenspan Put” earned its name because of his famous observation that you cannot identify a bubble when you’re in it… You can only lower rates after it bursts and “clean up the mess.”

Kevin Warsh appears to be following the Alan Greenspan playbook: leaning toward lower interest rates than many economists and Fed governors think is prudent — a stance that could once again redefine the market’s relationship with the Federal Reserve. (Source: Gemini)

Warsh says that if he’s confirmed and can persuade the board, he would aim for a similar outcome. But he adds a twist of his own.

Warsh advocates being more aggressive than Greenspan was… not waiting for the productivity to show up in the data.

His argument is that artificial intelligence has the potential to be far more disruptive — lowering costs, rising output — than the internet was three decades ago.

To head off an economic crisis, he advocates lowering rates before that shift becomes apparent in research reports rather than waiting until it’s visible.

One more layer of Warsh’s argument: By re-energizing the 1951 accord between Treasury and the Fed used to deal with historic debt accrued during World War II, Warsh says a ‘modern accord’ is needed to finance the out-of-control spending and debt accumulation the government has engaged in since the pandemic lockdowns in 2020.

That strategy might be even more radical than lowering rates into the energy shock caused by the Iran excursion. Under this plan, the Federal Reserve would step back from an activist role in regulating markets and sell Treasurys and mortgage-backed securities from its balance sheet.

The Warsh era at the Fed would mark a stark departure from the large-scale asset purchases that defined the last decade. If he gets his way, that is.

In a nutshell: Lower rates now or sooner. Less direct market intervention. Markets addicted to the Fed bailouts will have to clear supply on their own.

So would the Treasury… financing the $39 trillion in U.S. debt with 2-year Treasurys at lower rates on the short end of the curve and higher yields on 10-, 20- and 30-year bonds on the long.

🛢️ Oil Keeps Climbing while Washington Builds A Workaround

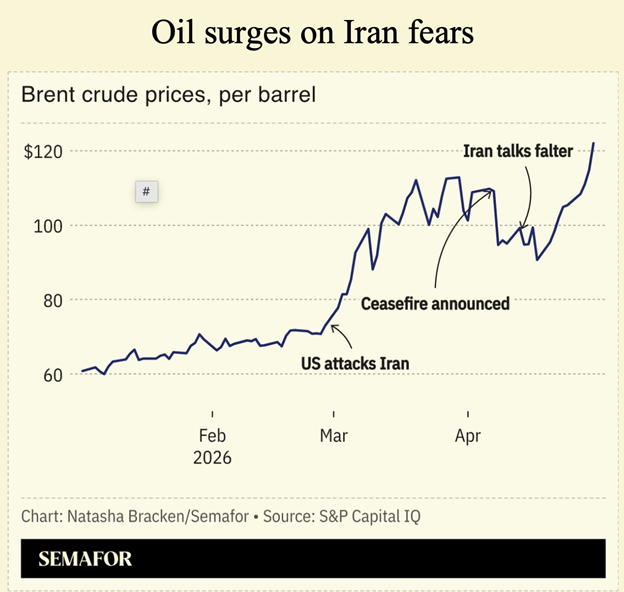

All the drama at the Fed comes with the U.S. naval blockade of Iranian ports in the Persian Gulf, driving oil prices back up to uncomfortable levels.

Oil prices are surging as uncertainty around the Iran conflict rattles global markets, with traders increasingly pricing in the risk of prolonged supply disruptions and a wider energy shock. (Source: S&P Capital IQ)

Oil prices are surging as uncertainty around the Iran conflict rattles global markets, with traders increasingly pricing in the risk of prolonged supply disruptions and a wider energy shock. (Source: S&P Capital IQ)

Brent crude pushed above $126 this week as the Iran conflict continues to disrupt flows through the Strait of Hormuz. The U.S. blockade on Iranian ports remains in place. Iranian officials have said they will respond if those restrictions continue.

Gasoline prices in the U.S. have already followed, reaching levels last seen after the early phase of the Ukraine war. Fuel moves through everything — trucking, aviation, shipping — and those costs show up before anything reaches a store shelf.

Washington is trying to build a workaround. Secretary of State Marco Rubio approved a plan to assemble a coalition to maintain shipping through the Strait. U.S. embassies have been told to line up participants, excluding China and Russia.

Those agreements take time. Cargoes are already pricing risk.

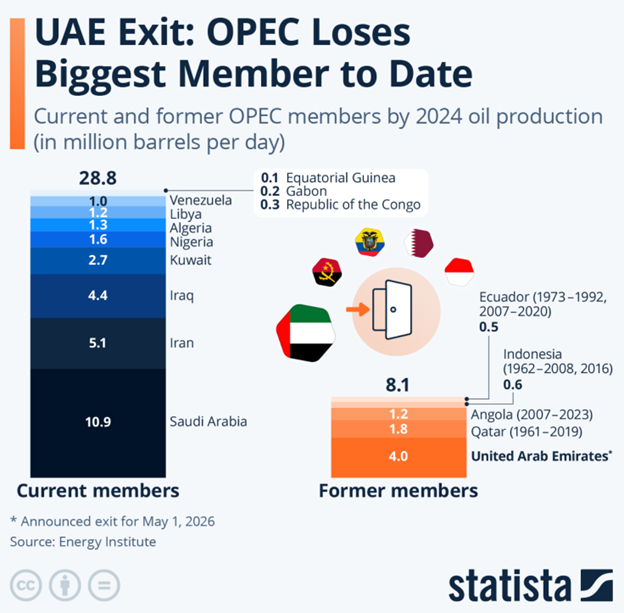

🌍 The UAE Quits OPEC

To make things interesting, the United Arab Emirates confirmed it will leave OPEC on May 1. Which is, um, tomorrow.

The UAE is one of the largest producers in Opec and has spare capacity it hasn’t been able to use under quota limits. Outside the cartel, it can set its own production levels. (Source: Statista.com)

The UAE’s announcement follows earlier exits by Qatar and Angola, but the UAE carries more weight. The Emirates have low extraction costs, large reserves and an economy that doesn’t rely solely on oil. That gives it room to increase output even if prices fall.

“The UAE is a long and complicated story,” our man on the scene admits, “buried in tribal history, and most importantly today, how the war has affected a core identity issue for Gulf Arabs.” We haven’t been able to connect further, and he warns it’s a highly sensitive issue.

For oil markets, the UAE’s departure introduces another moving part. A major producer gains some pricing flexibility just as prices are rising and supply routes are under reconstruction.

📉 Warsh Will Steps Into Higher Inflation and Higher Oil Costs

For now, we bid adieu to Powell (sort of) and await the broader Senate confirmation of Kevin Warsh as his successor.

One distinction Warsh will face: Greenspan held rates steady in the mid 1990s, with inflation near 2% and energy markets behaving themselves. Warsh would be working with inflation closer to 3.3% and Brent crude trading above $120.

Cutting rates in that setup lowers borrowing costs for the AI buildout and everyday American households while fuel, freight and electricity keep pushing prices higher.

At the same time, the Treasury must roll over its debt and deal with interest payments that have already crossed $1 trillion annually. Lower rates on the short end would reduce that cost at the margin.

That gap — between how much debt is issued and how cheaply it can be financed — has to be absorbed somewhere.

That’s where Treasury Secretary Scott Bessent’s plan for Dollar 2.0 – stablecoins and digital assets – starts doing its heavy lifting.

Stablecoins backed by Treasury bills, tokenized money market funds and on-chain cash pools all need short-term government paper as collateral. When those platforms grow, they become steady buyers of T-bills.

A crypto exchange holding reserves in Treasurys or a payments platform parking customer balances in tokenized bills is still buying the same debt the Treasury is issuing.

Dollar 2.0 demand sits mostly at the short end of the yield curve. It helps the Treasury fund itself without pushing long-term rates too high, too fast.

And it gives Treasury a broader base of buyers beyond banks, foreign central banks or the Fed’s balance sheet.

For Warsh, that matters. If the market can absorb new issuance through digital channels, the Fed can reduce its footprint and still move rates lower without stepping back in as the primary buyer.

As we said, there are a lot of moving parts. Both Warsh and Bessent’s plans are audacious to the fuddy-duddies who have become complacent at both the Fed and the Treasury.

Time to shake ‘em awake…

🪙 Gold royalties collect while operators carry the cost

We just released new research on one of our favorite niche asset classes. If you’re a paid-up member of the Grey Swan Investment Fraternity, you will have received several special reports in your email inbox yesterday.

Gold royalty companies — Franco-Nevada, Wheaton Precious Metals, Royal Gold, Triple Flag — provide capital upfront to mining companies in exchange for a percentage of production or the right to purchase metal at fixed prices.

Mining operators pay for fuel, labor and equipment. When diesel prices rise, operating costs increase. When supply chains delay equipment, projects stretch out. Those costs stay with the operator.

The royalty agreement stays the same. If a mine produces 100,000 ounces, the royalty holder receives its contracted share. If production rises, revenue rises. If costs double, the payment tied to output does not change.

That model is based on the price of gold rather than its production cost. If rates move lower or inflation stays firm, gold prices tend to respond. The royalty firms collect on that price without bearing the cost pressures beneath it.

To sum things up today, before we head off to Grey Swan Live! with Jeff Opdyke, the Fed is split. Powell will sit. Warsh moves toward confirmation.

Oil is trading above $126, at least until Iran “cries uncle,” the President told reporters in the Oval Office yesterday. A major producer quits the OPEC pricing cartel.

With any luck, the Senate Banking Committee will now turn its attention to passing the Clarity Act and get Dollar 2.0 back on track to last October’s jubilant rally trajectory.

Cheers,

~ Addison

P.S. Wall Street still believes the Fed will stay higher for longer. But if Warsh takes the chair sooner than expected, the entire rate outlook could flip almost overnight. That kind of policy shock is exactly the type of setup we can capitalize on before the crowd catches on. Learn more here…

And today, Grey Swan Live! returns with a new guest: Jeff Opdyke.

Jeff is a former Wall Street Journal writer who has moved not just to heavily invest overseas, but also to live overseas. Today, he’s trading and writing Global Intelligence Letter from his bolt hole in Portugal.

We’ll talk with Jeff about how he made his move overseas, why he’s focused on international investing, a weaker US dollar and some of the top foreign markets for investors today.