Yesterday, we answered the question “why gold?” and why now. (See: The 4th Great Gold Bull Market). Today, we’re going to tackle the question “why energy?”

Yesterday on Truth Social, President Donald Trump floated the idea that the U.S. should suspend its $1.5 trillion support of NATO. The foreign policy establishment was aghast. How dare he go there?

As it turns out, Trump is serious about dismantling the bureaucratic structure of NATO and removing the U.S. responsibility to pay for it.

What’s more, Trump wants to establish a modern Monroe Doctrine in Venezuela, Panama, Greenland and the Arctic.

He also aims to dismantle Iran’s military capability to bully its neighbors and harass Israel.

It turns out Trump is also serious about sovereign U.S. borders and deportation.

Trump is serious about disrupting the banking system and using technology to upgrade payment systems and secure the U.S. dollar as the world’s reserve currency.

Turns out, Trump is serious about realigning U.S. strategic military and economic ambitions with Saudi Arabian capital in exchange for Prince Mohammed bin Salman’s seat at the table for the future of the global AI economy.

Politicians talk. We’re immune to what they say because we know since their lips are moving, they must be… well, you know. Markets have learned to discount any potential follow-through or just ignore them altogether.

For Trump, to the shock and awe of the world, the follow-through is happening in real time.

Along with dismantled assumptions about geopolitics and money, it would be wise to accept that old assumptions about investing — 60% stocks, 40% bonds — are likely to change just as dramatically.

In 2025, Morgan Stanley’s macro desk recommended a shift toward 60% equities, 20% bonds and 20% gold.

Louis-Vincent Gave pushes that further: 60% equities, 20% gold, 20% energy.

Yesterday, we laid out the case for gold. (See: The 4th Great Gold Bull Market)

Today, we’re going to ask “why energy?”

🔥 Assumptions Built The Old System. Events Broke Them

For most of the past two decades, policymakers treated energy as background noise.

Capital flowed into software, AI hyper-scalers, financial services and space. Meanwhile, energy’s weight in the S&P 500 Index drifted toward 3%.

That positioning rested on three working assumptions. Louis-Vincent Gave:

First, that US Treasuries could be converted into physical supply when needed.

Second, the US Navy would always secure global shipping lanes.

Third, that the United States would continue to act as the stabilizing force behind global trade.

Those assumptions have all taken direct hits.

When Russian reserves were frozen after its invasion of Ukraine, central banks were aghast… and adjusted their reserve mix. They didn’t necessarily sell U.S. Treasurys, but they added alternatives, gold most notably, after Basel III established the metal as a tier-one asset, equally liquid as the US dollar itself.

Houthi attacks in the Red Sea and this month’s closure of the Strait of Hormuz showed how quickly shipping routes can be disrupted. The current conflict and response have forced decades-old post-World War II allies to reconsider how much financial support they can expect from the U.S. in a crisis.

Trump suggested in his speech to the nation last night that the U.S. doesn’t need to keep the Strait of Hormuz open. Once the military’s objective of decimating Iran’s missile and nuclear capabilities is achieved, Trump implied, the U.S.’s job is done.

The rest of the West – those who depend on free passage – should seize the Strait and “cherish it.”

In response, Iran established a de facto toll system in the Strait of Hormuz, charging roughly $1 per barrel — or up to $2 million per vessel — for safe passage. Payments are required to clear in yuan or stablecoins, with IRGC approval and naval escort required for transit.

🌏 Reserves, Storage And What Countries Actually Held

The United States entered the current disruption after a series of large drawdowns from the Strategic Petroleum Reserve.

Beginning in 2022, the Biden administration released 180 million barrels over six months – the largest drawdown in the reserve’s history. Ostensibly, the motive was in line with green energy policy and as a countermeasure to inflation… that was caused entirely by the lockdown of the economy and government spending.

The reserve fell from over 600 million barrels to roughly 347 million barrels by mid-2023. Replenishment efforts lifted that level back toward 415 million barrels by early 2026, still well below prior peaks.

By comparison, South Korea and Japan entered the Iran disruption with roughly 10days of natural gas supply. China entered with about 50 days of combined reserves.

Those numbers reflect earlier policy decisions. When oil was trading at roughly $40 a barrel, China did the exact opposite of the Biden-era policy, increasing storage and diversifying supply following sanctions episodes and U.S.led trade restrictions.

Allied economies continued to operate under the expectation that supply could be sourced quickly through global markets.

🏛️ Energy Policy, Supply Investment

At a White House media event with Japanese Prime Minister Sanae Takaichi, Trump was asked whether the United States coordinated with allies before striking Iran. Trump, now famously, asked, “Why would I? You didn’t warn us about Pearl Harbor.”

Despite the reserve drawdown, under a renewed energy policy, the United States produces roughly 13 million barrels of oil per day and remains a net exporter of petroleum products.

At the outset of hostilities, the oil markets adjusted immediately. The spread between WTI and Brent widened as Gulf shipping routes carried higher insurance costs and security risk, while U.S. inland supply remained unaffected.

China has restricted exports of diesel, jet fuel and fertilizer. European officials have discussed windfall taxes on energy producers. Those actions feed directly into capital allocation decisions.

Shrinking exports from east of Suez — namely the Middle East and Asia — are redrawing global transport fuel trade routes. (Source: Vortexa)

Shrinking exports from east of Suez — namely the Middle East and Asia — are redrawing global transport fuel trade routes. (Source: Vortexa)

An oil company evaluating a new project now has to price three outcomes at once: oil falling sharply if the Strait of Hormuz reopens, margins compressing under export controls and profits taxed if prices remain elevated.

Constraints extend downstream. Refineries at Ras Tanura, Mina Al Ahmadi, Haifa and Ashdod have been damaged in recent strikes. Global refining capacity was already tight due to permitting delays and years of underinvestment. Crack spreads remain elevated as a result.

Electricity supply is adjusting as well. South Korea and Japan entered the disruption with roughly 10days of natural gas. China entered with closer to 50. Utilities in import-dependent countries are increasing coal usage to stabilize power generation. Coal producers and rail operators have outperformed broader energy indices over the past year.

Technology investment is moving with power availability. Data center projects originally planned for Qatar, Saudi Arabia and the UAE are being reconsidered after recent disruptions. New projects in the United States and Canada are increasingly paired with dedicated power generation to ensure supply.

Across markets, the divergence is visible. Brazil, Colombia and Indonesia are seeing higher export revenues from energy and coal. Japan and Europe are absorbing higher import costs that are feeding into inflation and bond yields.

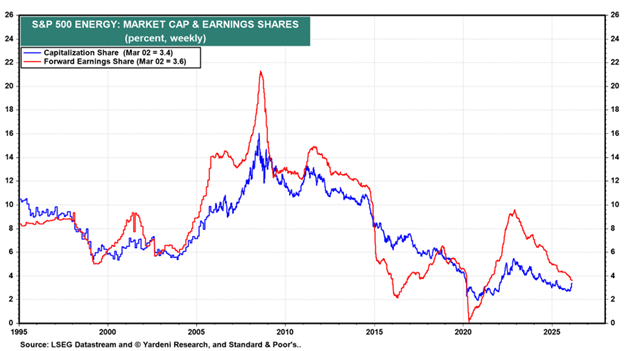

📊 From 3% Weighting To Central Role In Markets

The energy sector currently represents roughly 3% to 4% of the S&P 500 by market capitalization. Yet it contributes more than 10% of total index earnings and has delivered total returns above 30% over the past year.

Energy’s weight in the S&P 500 has dramatically shifted over time. (Source: X)

Energy’s weight in the S&P 500 has dramatically shifted over time. (Source: X)

As of this week, the Energy Select Sector SPDR Fund (XLE) reached a rare technical condition: every constituent company is trading above its 200-day exponential moving average. That kind of breadth signals broad institutional participation rather than a narrow rally in a few names.

The shift reflects a change in what markets are pricing. Technology companies are increasing capital expenditure on data centers, but those facilities require stable power. Utilities, pipelines, generation and fuel supply are now part of the same investment chain.

The bottleneck is moving away from chips and into electricity.

🌐 Where The Adjustments Are Showing Up

Energy-exporting economies are seeing immediate benefits. Brazil, Colombia and Indonesia are capturing higher revenues from oil, gas and coal exports.

Import-dependent economies are absorbing higher costs that feed directly into inflation, currency pressure and bond yields. Japan and Europe are exposed through energy imports.

Central banks are adjusting reserve allocation. Governments are reconsidering industrial policy. Companies are reassessing where to locate production and infrastructure.

The adjustments are happening simultaneously across multiple layers of the system.

📉 What Happened To The Old Portfolio?

Since U.S. strikes on Iranian targets escalated the conflict on February 28, equal-weighted balanced funds have delivered returns of -8.8% in Europe, -7.1% in Japan, -5.3% in the U.S. and -3.6% in China.

In the past fiveyears, we’ve weathered the COVID-19 pandemic, economic lockdowns, supply-chain destruction, a revolution in digital assets, the Ukraine invasion, the Biden green-policy fantasy and the violent demolition of Gaza.

Turns out, with the “excursion” in Iran, Trump is serious about his ambition for global trade-military-tech alignment.

Individual investors, Grey Swan members, would be wise to recognize the shifting priorities and allocations in their own portfolios “sooner rather than later,” as my friend David Walker likes to say.

~ Addison

P.S. Grey Swan Live! returned today at 2 p.m. ET.

While financial markets have seen big price swings over the past few weeks, AI development rolls on. And the crypto markets move, glacially, towards increased clarity. Ian has his eye on the pulse of the markets.

Ian’s view of the Clarity Act and Defi revolution, covering everything from tokenization to all our “Dollar 2.0” ideas to modernize the U.S. dollar and financial system – are key topics for discussion.