President Donald Trump extended the pause on Iranian energy strikes by 10days after Thursday’s close, pushing the deadline to April 6.

Earlier in the week, a similar delay knocked crude down nearly 10% in a single session.

Not so much this time. Yesterday, the decline lasted a few hours before buyers stepped back in, pushing oil prices higher overnight in Asian trading.

🧭 The Pressure Index, A Novel Look at the Markets

Every one of President Trump’s initiatives are high-stakes, must-win gamble. Tariffs. Attack on Federal Reserve Chairman Jerome Powell. Venezuela. Iran. China, coming up in May, now. The President needs all these gambits to work in order for the administration to maintain political control of the House and Senate in the fall.

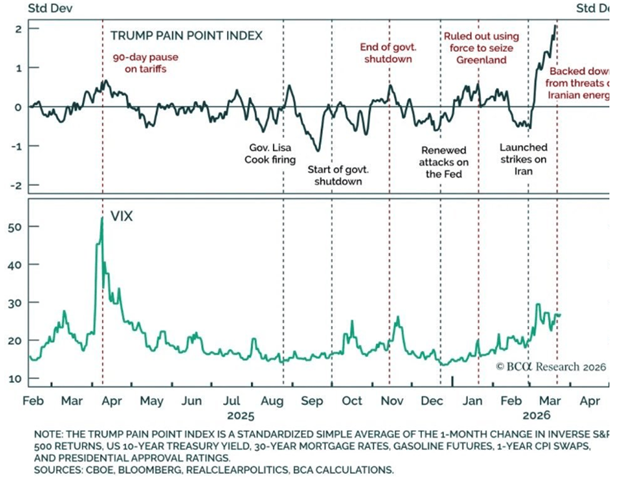

As we marveled at yesterday, Deutsche Bank traders tracked the Trump negotiating pattern long enough to quantify it for the bank’s strategists.

Following the missile and drone strikes in Iran, the Trump political pain index has moved to roughly two standard deviations above its long-term mean for the first time.

The index combines inverse S&P 500 Index returns, 10-year Treasury yields, 30-year mortgage rates, gasoline futures, one-year CPI swaps and presidential approval ratings into a single measure of economic and political strain.

Each prior spike aligned with a policy shift.

Tariffs paused in April 2025 after markets sold off. A government shutdown ended in September under similar pressure.

The Greenland acquisition proposal faded in December.

Earlier this week, threats against Iranian energy infrastructure were pulled back amid market volatility.

The pattern has been consistent enough to trade. Tonight, the President is scheduled to give the keynote address at the 4th Edition of the Future of Finance Miami 2026 summit hosted by the Saudi sovereign wealth fund. The conference aims to address how global economic shifts, AI, and energy transition affect investments.

Trump, we expect, is going to use the stage to tout his grand bargain – a ‘super deal’ – with Saudi Prince Mohammed bin Salman.

🛢️ Oil Holds Steady For Now

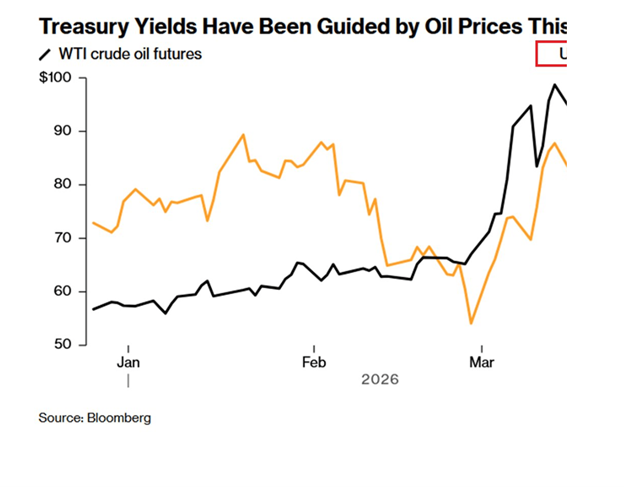

Crude has been trading at $93 amid continued Strait of Hormuz constraints.

In more sanguine times, oil prices and Treasury yields are less correlated. Right now, Trump’s high-stakes game of geopolitical poker, each statement he makes on Truth Social gets a reaction from both energy and debt markets. We’re confident he’s getting a kick out to that fact. (Source: Bloomberg)

In more sanguine times, oil prices and Treasury yields are less correlated. Right now, Trump’s high-stakes game of geopolitical poker, each statement he makes on Truth Social gets a reaction from both energy and debt markets. We’re confident he’s getting a kick out to that fact. (Source: Bloomberg)

The U.S. 10-year Treasury yield rose to 4.47%, the highest level since June, and has climbed roughly 50 basis points since the war began.

The move has taken yields back toward the 4.50% to 4.70% range that forced policy adjustments in April 2025.

At the same time, the Treasury issued $183 billion in new debt this week. Seven-year notes cleared at 4.255%, above the pre-auction level, marking the weakest three-auction sequence since May 2024.

Bond buyers – the advance guard of the vigilantes – required higher compensation to absorb supply.

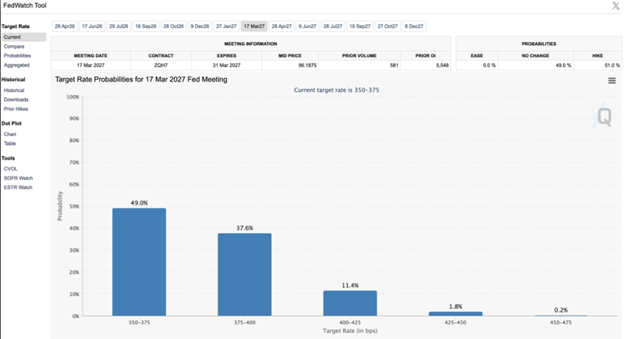

Futures markets that priced rate cuts a month ago are now pricing a potential rate hike as early as May 15, 2026, ostensibly Jerome Powell’s last FOMC meeting as the Fed chair. (Source: Barcharts)

Futures markets that priced rate cuts a month ago are now pricing a potential rate hike as early as May 15, 2026, ostensibly Jerome Powell’s last FOMC meeting as the Fed chair. (Source: Barcharts)

Inflation swaps reached 5.2%, the highest level since March 2023 during the SVB and First Republic bank runs.

Each move has tightened financial conditions across the system. Mortgage rates have pushed back toward 7%. Credit costs have risen for consumers and businesses. Government financing costs have increased alongside issuance.

In April 2025, the 10-year yield approached 4.50%, and the tariff policy reversed

If nothing else, the drama playing out on our trading screens is entertaining. For ideas on how to trade this environment, see the Grey Swan Trading Fraternity.

🏦 Powell, Warsh, and Timing

So what happened to Trump’s pressure on Jerome Powell to manhandle the Fed into lowering rates?

Under Section 10 of the Federal Reserve Act, Jerome Powell remains in place until a successor is confirmed. He has indicated he will continue in that role if necessary.

The policy divide has sharpened as the political pain index rises.

Powell’s framework responds to data on the books. By its very nature of waiting for data, the model is always reactive, “always late” as Trump would put it.

In the current scenario, the oil shock will feed into inflation readings. Inflation readings will influence Fed governor rate decisions. They will favor no cuts for the next meeting in April and perhaps vote to hike them at the following meeting. The central banks of major G7 trading partners are all reading from the same playbook and have announced they’re reading to hike rates, too.

Trump’s nominee for Fed chair, Kevin Warsh, has argued for a forward-looking approach, in which policy adjusts before observed disruptions in labor, capital formation and energy markets. Especially those that will benefit from AI productivity gains.

Warsh’s position advocates that the Fed anticipate structural changes rather than react to trailing indicators, particularly as war, energy shocks and AI-driven labor shifts occur simultaneously. Lower rates, in his view, will help capital get into the hands of the right people to support the economy growing at the pace new technology allows.

Treasury Secretary Scott Bessent agrees. An independent Fed that is not tasked with managing the economy or bailing out Wall Street banks will actually help him in his #1 role: financing the $39 trillion in U.S. debt.

For the same reason, Bessent is a champion of Dollar 2.0 digital assets in the ongoing policy disagreement over the Clarity Act under review by the Senate Banking Committee.

There’s a slight chance Trump will address the interest-rate conundrum and/or digital assets in his speech before the 2,000 global leaders assembled in Miami tonight.

⚙️ Labor Adjusts Before Policy

Goldman Sachs economist Joseph Briggs reported that roughly 300 million jobs globally are exposed to automation. In the United States, tasks representing about 25% of total work hours can be handled by AI systems.

AI Disruption has extended into consulting, call centers and design work, where AI systems now complete tasks previously handled by teams.

As you might expect, labor demand has shifted toward physical infrastructure. Construction, electrical work, plumbing, engineering and grid expansion roles are increasing as data centers and power systems scale.

Goldman estimates roughly 500,000 additional workers will be required to meet electricity demand tied to AI infrastructure by 2030.

💻 Credit Markets Are Pre-Sorting Outcomes

Credit spreads for software issuers widened by more than 250 basis points this year, raising borrowing costs unevenly across the sector. As Andrew Packer has been detailing quite thoroughly for Grey Swan, the private credit redemption crisis is in danger of seizing the whole market.

But we aren’t there yet.

Companies embedded in regulated workflows or controlling proprietary data have retained access to capital and continue to issue debt at manageable spreads.

So far, financial stocks have followed the same path.

The sector is down more than 10% year to date, roughly twice the decline of the broader index. Lenders exposed to consumer credit have repriced to reflect rising unemployment risk and tightening conditions.

At the same time, positioning has moved toward the lower end of its five-year range, with investor allocations to financials falling into the 15th percentile.

There’s a lot of technical jargon in the Goldman letter to its traders. But it’s fair to say, they’re bracing for the private credit “cockroach” to reveal further damage, more funds dropping to zero; the algorithms in their black box accounting methods are losing positive input.

🪙 Gold Absorbs the Flow

On the physical side of the ledger, we have also digested a long-ish report from our favorite Austrian economist outlet, The Daily Economy.

We summarize:

Gold has outperformed major U.S. equity indices since 2000 and has continued to attract capital across cycles.

Following the Basel III classification of gold as a Tier-One liquid asset, fully in effect in 2025, central banks have increased purchases as sovereign debt levels expand and reserve strategies shift away from concentrated currency exposure.

Geopolitical conflict has increased demand for assets outside political systems, particularly in regions exposed to energy and currency volatility.

Industrial demand has grown alongside financial demand, with gold used in electronics, computing infrastructure and advanced manufacturing.

Digital asset systems have begun using gold as collateral alongside Treasurys, linking commodity markets with emerging financial rails.

Supply growth has remained limited while demand has increased across multiple channels. Prices have adjusted accordingly.

Gold rallied to $4500 and change this morning.

🌸 Along the Potomac

On March 27, 1912, Helen Taft and Viscountess Chinda planted two Yoshino cherry trees along the Potomac.

The cherry trees along the Tidal Basin, East Potomac Park and the White House grounds are offre one of a few reasons you might actually want to visit D.C. in the spring. (Source: The History Channel)

The cherry trees along the Tidal Basin, East Potomac Park and the White House grounds are offre one of a few reasons you might actually want to visit D.C. in the spring. (Source: The History Channel)

An earlier shipment of cherry trees had arrived diseased and was destroyed. A second shipment of 3,020 trees was sourced from the Arakawa River near Tokyo and transported successfully.

After World War II, cuttings from those trees were sent back to Japan to restore stock destroyed during the bombing of Tokyo.

The same trees still line the water. They are beginning to blossom today, indicating that spring is really on the way.

Peace, amity and tranquility are better than war.

~ Addison

P.S. If you missed this week’s Grey Swan Live! with Ronan McMahon, it’s worth carving out time to watch the replay.

We recorded from Panama, where Ronan walked us through how global real estate markets evolve — and why some regions quietly attract capital, talent, and growth for decades at a time.

The key takeaway? Most investors limit themselves to what’s familiar. But the best opportunities often aren’t.

Watch now to see:

- Why places like Panama continue to benefit from global trade, migration, and business expansion.

- How early access to deals can create pricing advantages that don’t exist in public markets.

- The difference between buying property … and positioning for long-term capital appreciation.

- And how some investors are blending income, lifestyle, and upside into one strategy.

P.P.S. After you watch, you can take advantage of a special gift for Grey Swan members to join Ronan’s Real Estate Trend Alert for free … and for life! Click here to get started.