This Friday, SpaceX goes public.

At a reported valuation approaching $1.75 trillion and a capital raise of nearly $75 billion, it will be the largest IPO in history. Wall Street is preparing accordingly. Financial television is treating the event like a moon landing. Fund managers are polishing their talking points.

Retail investors are searching for ways to participate in what many already regard as the defining public offering of the decade. If you’re not already “in” in some meaningful way, we have suggestions:

- Don’t get caught with your pants down ogling the mania

- Look at the lesser-known “Shadow IPO” plays that are less expensive, less volatile and will benefit from the fervor all the same.

You may recall earlier, on December 4, 2025’s episode of Grey Swan Live!, we had a good laugh with guest Dan Denning as we speculated a mega-IPO would ring the bell at the top of the skyrocketing (pun intended) stock market. We anticipated that the IPOs would likely be Anthropic or OpenAI. Some combo of the two and/or SpaceX.

SpaceX is going to be there first.

SpaceX sits at the intersection of nearly every story investors care about today: artificial intelligence, national security, advanced manufacturing, satellite communications and the growing competition between great powers.

Yet while investors focus on rockets, the bond market has begun sending a message that deserves at least as much attention.

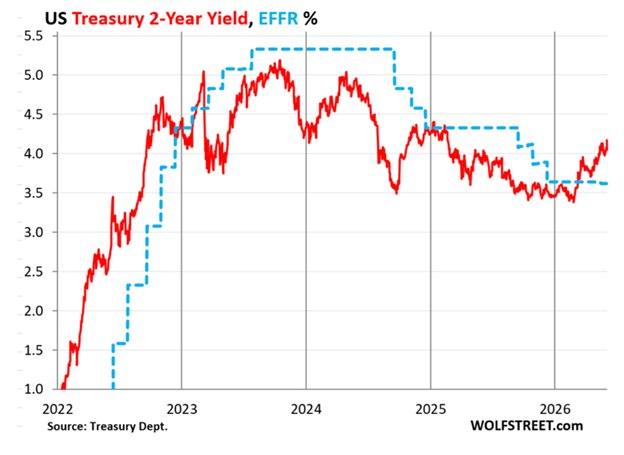

On Friday, the 2-year Treasury yield closed at 4.17%, its highest level since February 2025. Only a few months ago, traders expected additional rate cuts.

Short-term yields are moving in the exact opposite direction of Trump’s political will, just in time for Kevin Warsh’s first FOMC meeting as the Fed’s chair. Will he use the opportunity to excoriate the Phillips Curve? One can only hope. Maybe he’ll support auditing the Fed, too. Ha! (Source: Wolf Street)

Short-term yields are moving in the exact opposite direction of Trump’s political will, just in time for Kevin Warsh’s first FOMC meeting as the Fed’s chair. Will he use the opportunity to excoriate the Phillips Curve? One can only hope. Maybe he’ll support auditing the Fed, too. Ha! (Source: Wolf Street)

Since late February, yields have climbed nearly 80 basis points as markets reassessed the path of monetary policy following a series of surprisingly strong employment reports. Instead of an economy drifting toward recession, investors found themselves confronting one that continues to create jobs despite years of elevated interest rates.

The response revealed something curious about modern markets.

Strong economic news no longer guarantees enthusiasm. For investors conditioned by years of central bank intervention, a healthy labor market can create anxiety because stronger growth reduces the urgency for lower interest rates.

Good news threatens easy money.

🎰 The “Fed Put” And The Theory Behind It

The modern investing environment owes much to a lesson first taught in the aftermath of the 1987 stock market crash.

When markets seized up, Federal Reserve Chairman Alan Greenspan responded aggressively. Investors learned that severe market declines often attracted monetary support.

The pattern repeated often enough over subsequent decades that it became embedded in investor psychology. Greenspan responded to crises. Bernanke responded to crises. Yellen responded to crises. Powell responded to crises.

Each intervention strengthened the assumption that financial markets operated with a safety net underneath them.

The intellectual foundation supporting many of those decisions rested upon a framework known as the Phillips Curve.

For decades, central bankers believed inflation and unemployment shared a predictable relationship. When unemployment fell, employers competed for workers. Wages rose. Rising wages eventually fed through to higher prices. Policymakers came to believe they could manage inflation by monitoring labor markets and adjusting demand accordingly.

The theory appeared to work well enough during portions of the postwar period. Then the 1970s arrived and made a mess of the model.

Oil prices surged. Inflation surged. Unemployment surged, too.

The economy experienced both high inflation and weak employment simultaneously, a combination that was not supposed to happen under the original framework. Economists Milton Friedman and Edmund Phelps had warned that workers and businesses would eventually adapt to inflation. Once inflation became expected, the relationship between unemployment and prices became far less predictable.

The Federal Reserve never completely abandoned the Phillips Curve after stagflation. Instead, economists modified it, expanded it and incorporated increasingly sophisticated assumptions about expectations and behavior.

Kevin Warsh increasingly sounds unconvinced.

One of the market’s biggest assumptions this year was that Warsh would usher in a more dovish era at the Federal Reserve. But strong jobs growth and resilient economic data are pushing expectations in the opposite direction. Rather than racing to cut rates, a Warsh Fed may find itself keeping policy tighter for longer than investors anticipated. (Source: Bloomberg)

His criticism reaches beyond interest rates and into the intellectual machinery driving Federal Reserve decision-making. Warsh frequently points toward government borrowing, fiscal deficits and central-bank balance sheets when discussing inflation. Under that framework, rising prices emerge less from workers gaining bargaining power and more from policymakers creating too much money while financing spending levels that the economy struggles to absorb.

That shift in emphasis changes how policymakers interpret the same set of facts.

A strong employment report no longer serves primarily as an inflation warning. It becomes evident that productive economic activity remains healthy while attention turns toward the fiscal and monetary decisions occurring elsewhere in the system.

Deficits, debt issuance and balance-sheet expansion occupy a much larger role in the analysis than they did under the traditional Phillips Curve framework.

Investors discussing Warsh often focus on whether he is hawkish or dovish.

The more consequential question involves the assumptions he brings to the job. A Federal Reserve that abandons decades of Phillips Curve thinking would not simply change interest-rate policy. It would change how policymakers understand inflation itself.

⚔️ Trump’s War Put

Financial markets have spent much of the past year displaying remarkable confidence in favorable outcomes.

That retail confidence extends well beyond monetary policy.

Since the conflict with Iran intensified, investors have repeatedly embraced signs that negotiations remain active and that diplomatic progress continues. Equity markets have generally treated each indication of potential settlement as confirmation that stability remains close at hand.

Commodity traders, shipping firms and insurance underwriters operate under different constraints.

The Strait of Hormuz handles roughly one-fifth of global petroleum flows. Tankers crossing those waters do not move because investors feel optimistic. They move when operators, insurers and cargo owners conclude the risks justify the journey. Insurance premiums respond to probabilities, not headlines. Shipping routes respond to conditions on the water, not hopes about future agreements.

Yet despite the uncertainty surrounding one of the world’s most important energy corridors, the S&P 500 Index continues to behave as though geopolitical instability is a temporary interruption rather than a defining feature of the current landscape.

That confidence increasingly resembles a second form of market insurance. Investors spent decades relying on central banks to stabilize financial markets. Many now seem equally convinced that political leaders can eventually stabilize geopolitical events.

🥇 Gold Gets Left Behind

The behavior of gold offers another glimpse into prevailing market psychology.

A conflict involving Iran, disruptions in the Strait of Hormuz and growing questions about the future monetary order would ordinarily create a favorable environment for precious metals. Instead, investors have spent much of the year selling them.

Gold remains well below its January highs. Silver has weakened. Mining shares have fallen even further as capital chases artificial intelligence, technology shares and speculative growth opportunities.

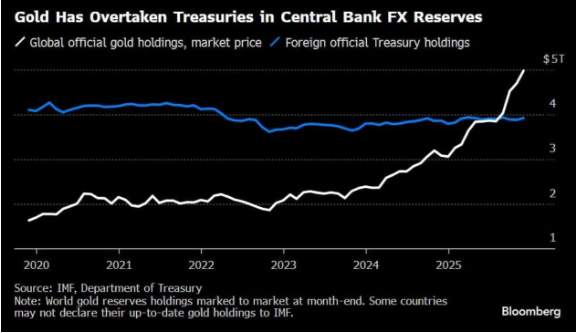

Central banks have chosen a different path.

For years, central banks were steady sellers of gold. Now, they’re among the market’s biggest buyers. From emerging economies to major global powers, policymakers are quietly building gold reserves as they seek greater independence from the U.S.-centric financial system. (Source: Bloomberg)

Recent reserve data show gold surpassing U.S. Treasurys as the largest reserve asset held by central banks, accounting for roughly 27% of reserves compared with approximately 22% for Treasury securities. The last time gold occupied such a prominent position in global reserve management, the Bretton Woods system still defined the monetary landscape.

The divergence is striking. Institutions responsible for preserving national balance sheets continue to accumulate bullion, while private investors pour money into risk assets associated with technological transformation.

History rarely rewards either side forever.

🏗️ The AI Buildout Continues

Meanwhile, the physical construction – the energy and resource layer of the AI five-layer cake – supporting the AI economy continues at an astonishing pace.

Data center construction now exceeds office construction in the United States. Roughly $50 billion is flowing into data centers compared with approximately $43 billion directed toward office projects.

What began as a “software story” increasingly resembles one of the largest infrastructure projects of the modern era. Even if the suggestion drew widespread “boos” among college graduates during various commencement speeches over the last month.

At some point, adults realize that every new data center requires electricity. Meeting that demand requires additional generation capacity, expanded transmission networks and enormous quantities of electrical equipment.

Semiconductor fabrication facilities consume billions of dollars before producing a single chip. Utilities, engineers, natural-gas producers, equipment manufacturers and technology companies increasingly find themselves participating in the same industrial ecosystem.

The physical footprint of artificial intelligence expands far beyond Silicon Valley.

Peter Thiel is building a fortified residence in Uruguay. Mark Zuckerberg reportedly oversees portions of Meta’s restructuring efforts from a $300 million yacht while directing tens of billions of dollars toward AI development.

Across the world, governments compete for computing capacity, electrical infrastructure and technological leadership because they increasingly understand that advanced computing sits near the center of future economic power.

The future has arrived, carrying permits, construction equipment and utility bills.

🕯️ June 8, 1968

Fifty-eight years ago today, Scotland Yard arrested James Earl Ray at Heathrow Airport for the assassination of Martin Luther King Jr.

Most Americans remember King as a civil rights leader.

Fewer remember how much of his final year focused on economic questions.

By 1968, King devoted increasing attention to poverty, opportunity and the distribution of prosperity throughout American society. He spent less time discussing formal legal equality and more time asking who benefited from economic growth, who remained excluded from it and how wealth circulated through the country.

Those questions remain remarkably durable.

Every generation develops new technologies, new industries and new financial instruments. Yet the underlying debates remain familiar because economic systems always distribute rewards unevenly. Some groups capture extraordinary gains. Others absorb costs they did not create.

The Great Race increasingly raises those questions again as trillions of dollars flow toward artificial intelligence, industrial infrastructure and geopolitical competition.

Who benefits?

Who pays?

History rarely stops asking.

~ Addison

P.S. Wall Street will spend this week talking about SpaceX. And so will we… likely, anyway.

While the bond market may prove more consequential… and a mego-IPO might actually prove to be the pin that pops the bubble… well, that remains to be seen, doesn’t it?

A shift in how the Federal Reserve understands inflation would reverberate through every asset class, every borrowing decision and every balance sheet in the country long after the IPO headlines fade.

On Thursday’s Grey Swan Live!, we’re going to dig deep into the SpaceX IPO, its significance to the broader market and identify the lesser-known opportunities we’re confident will be missed by the majority of the stock investing public.