There was a time when buying your first house ranked somewhere between getting married and buying your first new car on the list of American rites of passage.

You found a modest place, painted the spare bedroom on weekends, argued with the neighbors about whose tomatoes deserved the blue ribbon and slowly accumulated equity while pretending the mortgage would someday disappear.

Today, the first step onto the property ladder increasingly resembles standing outside an exclusive nightclub. The velvet rope isn’t there to create excitement. It’s there because hardly anyone can afford to get in.

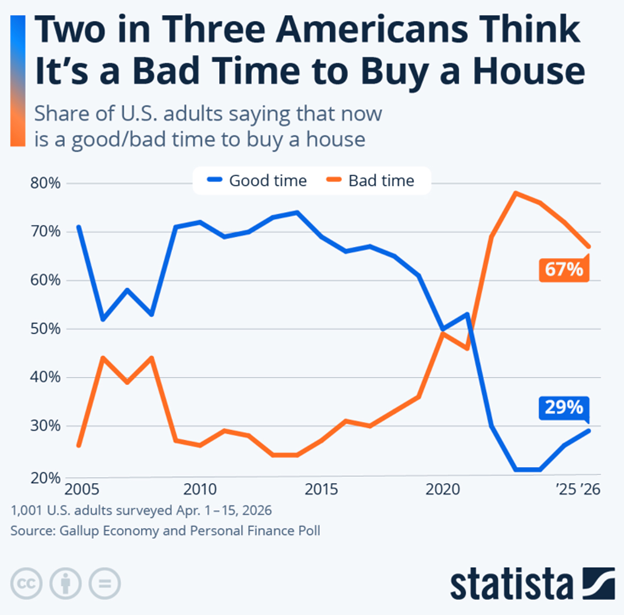

Gallup’s latest housing survey tells the story with unusual clarity. Nearly two-thirds of Americans now say it’s a bad time to buy a home — the most pessimistic reading since Gallup began asking the question in 1978.

Remarkably, Americans are more discouraged today than they were during the wreckage of the 2008 housing collapse.

For millions of Americans, buying a home has never felt further out of reach. A combination of high home prices, elevated borrowing costs and limited inventory has created a perfect storm for affordability. Even as the broader economy shows signs of strength, the housing market continues to squeeze first-time buyers and existing homeowners alike. (Source: Statista)

For millions of Americans, buying a home has never felt further out of reach. A combination of high home prices, elevated borrowing costs and limited inventory has created a perfect storm for affordability. Even as the broader economy shows signs of strength, the housing market continues to squeeze first-time buyers and existing homeowners alike. (Source: Statista)

That should stop us for a moment.

The financial crisis was defined by collapsing home prices, failing banks and foreclosure signs sprouting across suburban lawns like dandelions after a spring rain.

Today’s problem is almost the mirror image. Houses remain expensive. Mortgage rates remain stubbornly elevated. Down payments have become moving targets as inflation quietly erodes the savings families spent years accumulating.

Artificial intelligence has added another wrinkle.

Every conference room in America seems to contain at least one executive wondering how many jobs software will eventually replace. Every office contains at least one employee wondering whether that conversation includes his desk.

A 30-year mortgage requires confidence in tomorrow. Confidence has become harder to finance than the house itself.

History suggests housing never remains permanently disconnected from household income. Every cycle eventually corrects itself. Prices fall, incomes rise or some combination of the two restores equilibrium.

Unfortunately, the timing has never appeared on Zillow.

💵 Scott Bessent’s Strong Dollar

Housing as a proxy for the “affordability” issue leading up to November’s midterm elections is going to pose a challenge for Scott Bessent and Kevin Warsh, the Treasury Secretary and Federal Reserve chairman, respectively.

The fourth of the five legs, Mr. Bessent presented at the Economic Club of New York on Tuesday night, is a “strong dollar.” The outline of the Trump administration’s economic policy is meant to assuage voters that the “got this” in time to keep the democratic socialists from gaining the upper hand in the House of Representatives in Washington and really mucking things up for the country.

Unfortunately, a “strong dollar” is one of Washington’s oldest mantras. Every Treasury secretary says some version of it.

Robert Rubin said it.

Henry Paulson said it.

Tim Geithner said it.

Janet Yellen said it.

Scott Bessent says it.

The phrase sounds reassuring because nobody campaigns for a weak currency.

Yet most Americans have spent their adult lives watching the dollar purchase less food, less gasoline, less education, less health care and dramatically less housing. Gold has climbed from below $300 an ounce at the turn of the century to more than $4,200 today.

Federal debt has expanded from roughly $5.7 trillion in 2000 to more than $40 trillion today. Purchasing power has quietly slipped away while Washington has continued to assure the public that America favors a strong dollar.

The apparent contradiction disappears once we recognize that the dollar now performs two very different jobs.

Families experience the dollar as spending power. Global capital experiences the dollar as infrastructure.

For most of the 20th century, exchange rates performed something like shock absorbers. Countries that became less competitive eventually watched their currencies weaken. Exports became cheaper. Factories became busier. Trade imbalances slowly corrected themselves.

That mechanism has weakened because America exports something different than it once did.

Foreign investors are no longer exchanging dollars primarily to buy American machinery, wheat or automobiles.

They’re buying SpaceX (SPCX) and Micron Technology (MU); they’re buying venture-capital and private-equity funds; they’re buying Treasury securities. They’re Dollar 2.0 stablecoins and the financial architecture surrounding innovation itself.

The dollars spent on imported automobiles and televisions have an odd habit of returning to the United States wearing different clothes. They leave inside shipping containers. They come back wearing tailored suits and carrying brokerage statements.

Scott Bessent understands that distinction.

When he speaks about preserving confidence in a strong dollar, he is less concerned with exchange rates than with preserving the institutional plumbing that supports the dollar. Treasury securities remain the collateral underpinning global banking. International trade continues settling overwhelmingly in dollars. Global credit markets continue to measure risk in dollars.

Confidence in that architecture remains one of America’s greatest strategic advantages.

🏭 Financial Dominance or Financial Repression?

President Trump appears to be pursuing a different objective.

His administration wants lower borrowing costs, expanded manufacturing, larger capital expenditures and a revival of industrial production that has gradually migrated overseas during the past four decades.

That ambition sits awkwardly beside America’s financial dominance.

For years, the United States has financed consumption by exporting financial assets. Foreign capital eagerly purchased Treasury securities, corporate bonds, private-equity partnerships, venture capital funds and technology stocks. Wall Street prospered. Financial assets appreciated. Manufacturing steadily occupied a smaller share of the economy.

Readers of Empire of Debt will recognize the pattern. Empires rarely decline because they suddenly run out of money.

They decline because finance gradually replaces production. Speculation becomes more profitable than manufacturing. Capital discovers that it earns higher returns by trading paper than by building factories.

That transition rarely feels dangerous as asset prices continue to rise.

It becomes much more obvious once governments discover that financial markets and the real economy no longer move together.

The Federal Reserve’s latest figures illustrate how far that transition has progressed.

Total public debt now exceeds 122% of gross domestic product (GDP), while debt held by the public approaches 99% of GDP. Those figures would have seemed extraordinary when we first began writing Financial Reckoning Day and almost unimaginable when the first edition of Empire of Debt was published two decades ago.

After 40 years of ‘structural disinflation’, we’ve entered into a new regime of ‘structural inflation’, meaning, among other things, financing the national debt is getting increasingly more expensive. (Source: Luke Gromen on X)

After 40 years of ‘structural disinflation’, we’ve entered into a new regime of ‘structural inflation’, meaning, among other things, financing the national debt is getting increasingly more expensive. (Source: Luke Gromen on X)

Trump and his constituent secretaries are actively trying to reverse some of those incentives.

Factories instead of financial engineering. Capital investment instead of balance-sheet expansion. Industrial production instead of perpetual asset inflation.

Whether that transition succeeds depends upon forces much larger than tariffs or campaign slogans.

Wall Street became extraordinarily successful because finance proved more profitable than production.

Changing that equation may prove considerably more difficult than announcing it. The distinction worth watching over the next several years is not between a strong dollar and a weak dollar.

It’s not between lower short-term interest rates or higher long-term ones. It’s not between the local currency you use to buy gas and food in versus the global currency used to settle trade deals and

It is between two important terms we’re going to dig into on Grey Swan Live today with Dan Amoss, Jim Rickards’ investment strategist: financial dominance and financial repression.

Neither is a good option. Both require aggressive policies that must show progress in voters’ home balance sheets before November 3. The fickle swing voters in the middle don’t have a lot of patience for economic theory.

Let’s begin by observing the difference between the two:

Financial dominance attracts global capital because investors trust American institutions, American markets and American innovation. Capital arrives voluntarily because opportunity appears abundant.

Financial repression is something else entirely.

Governments encourage — or compel — domestic savings institutions, banks, pension funds and insurers to absorb ever-larger quantities of public debt while interest rates remain below the rate of inflation.

Savers quietly subsidize borrowers. Purchasing power erodes slowly enough that few people notice the transfer until years later.

These two systems can coexist for a surprisingly long time. Eventually, however, policymakers discover they must choose which one they intend to preserve.

That choice — not tomorrow’s inflation report or next week’s employment numbers — may become the defining investment question of the decade.

As we argued years ago in Empire of Debt and later in The Demise of the Dollar, monetary systems rarely fail all at once. They evolve. Incentives shift. Institutions adapt.

Investors who recognize those shifts before the headlines do usually fare much better than those waiting for television commentators to explain what has already happened.

After we discuss the lesser evil of financial dominance or repression, we’ll report back to you… likely in tomorrow’s Swan Dive.

The Inbox Is Heating Up

“All you guys in Baltimore,” reader Keith M. writes in one email we cherry-picked for today, “obviously all drink at the same bar!”

Its “all”about money and while i must admit i sought and payed several of you providors to help guide me into a profifable future, i did still expect there to be a level of judgement and wisdon to balance that economic knowledge with thoughts of the planets health and future.

While i agree there were areas where the last administration made bad calls especially in the areas of blockchain, digital currency and locking up too much of your mineral reserves, they also did good in playing their part in helping theworld decarbonize the planet.

Okay, we’ll bite.

First, contributors to Grey Swan live all over the country – Baltimore, Florida, Oregon, New York, Virginia, Tennessee – and the globe – the U.S., Great Britain, Ireland, France, Australia, Argentina, Uruguay. Would that we could all drink at the same bar!

Second, you’re asking us to associate two very different things — our financial recommendations and political observations. Climate change, fossil fuels and carbon emissions are among the most widely misunderstood and abused topics to cross our desk.

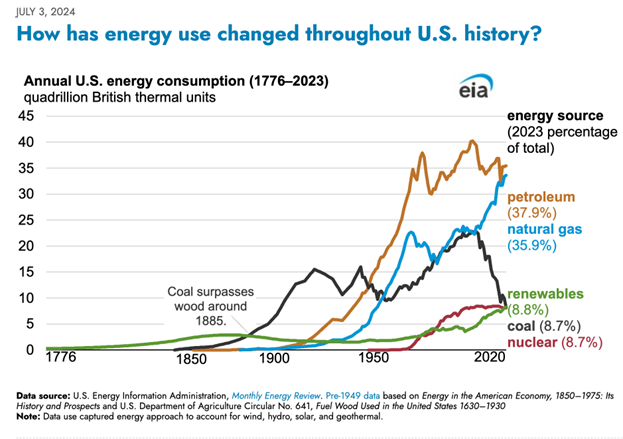

We won’t go into here, but we’ve spent countless hours studying climate science, including an intensive trip to the Greenland Ice Shelf with scientists organized by our friend John Englander of the Rising Seas Institute. We don’t claim to be experts in the science, but will leave you with this chart:

Every major technological revolution has required more energy, not less. And the AI boom is no exception. Behind every chatbot, autonomous machine and data center sits an enormous amount of electricity consumption. As digital infrastructure expands, energy demand is becoming one of the defining investment themes of our time. (Source: EIA)

Petroleum and natural gas remain the dominant sources of energy in the U.S. and have throughout the climate change hysteria we’ve all been forced to endure. The cost of energy is central to the debate over “affordability” itself… so we’re likely not done talking about it today.

~ Addison

P.S. Housing has always been one of the clearest proxies for the financial health of the American middle class. When families can comfortably buy homes, confidence tends to spread through the economy.

When they can’t, the consequences eventually reach far beyond real estate. Keep one eye on home affordability and the other on the United States’ balance sheet. They are telling versions of the same story.

While investors maintain their focus on AI and momentum stocks, Kevin Warsh’s first Fed meeting signaled that he’s prepared to move away from the Fed’s long-standing practice of telegraphing future policy moves.

So, this week on Grey Swan Trading Fraternity, we discussed why that matters — and what it could mean for market volatility and investment opportunities in the months ahead.